Stock #2 | Jun ’24 | HFBL

Rediscovering A Legacy of Trust and Service: Home Federal Bancorp, Inc. of Louisiana

By Zach Gedal | June 1, 2024 30-minute read

Discussion of Home Federal Bancorp, Inc. of Louisiana

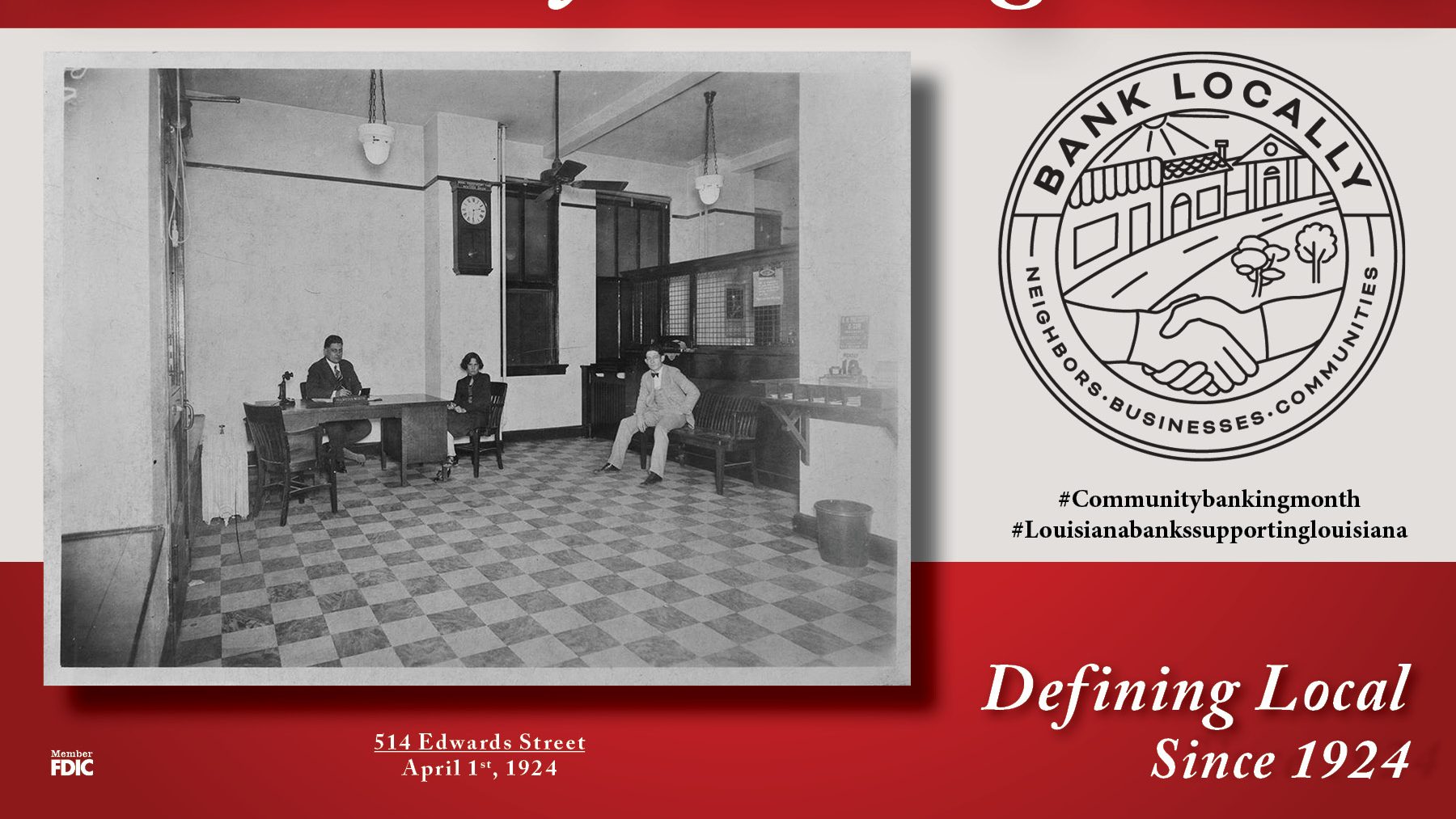

Home Federal Bank, headquartered in Shreveport, Louisiana since its inception in 1924, epitomizes a robust tradition of financial dependability and an unwavering commitment to community involvement. As Home Federal Bancorp, Inc. of Louisiana, and trading under the NASDAQ symbol HFBL, the institution has been integral in propelling local economic advancement and enhancing community welfare. Its emphasis on comprehensive savings strategies and diversified financial services significantly bolsters homeownership and individual financial security across the region, making it a stalwart of financial health.

The bank’s rich historical narrative is peppered with influential leadership figures like George M. Hearne and Amos L. Wedgeworth, whose visionary guidance has spurred its growth and widened its reach. Transitioning to a holding company structure in 2010, Home Federal Bancorp has not only expanded its service spectrum but also solidified its position as a pillar of community trust. For dividend investors, Home Federal Bank represents a venerable institution whose consistent performance and community-centric business model promise reliability and potential for sustained income, embodying the true essence of a ‘Dividend Darling’

The Foundation of Financial Stability

Founding and Early Years (1924-1934)

In 1924, amidst the economic vibrancy of the Roaring Twenties, Home Federal Bank was established in Shreveport, Louisiana, under the leadership of George M. Hearne. This era, marked by rapid industrial growth and a booming stock market, provided an opportune moment for new financial institutions to support burgeoning economic activities and the growing aspirations of middle-class America. As the founding president, Hearne steered the bank through its nascent decade, laying down the principles of community engagement and financial resilience. These early years not only set the foundation for the bank’s future growth but also embedded it within the fabric of Shreveport’s expanding economy, helping locals navigate the financial complexities of the time. This period was pivotal as it demonstrated the bank’s capability to support and stabilize the community, even as the nation edged towards the economic downturn of the Great Depression.

Leadership and Legacy (1934-2010)

From 1934 to 2010, Home Federal Bank witnessed significant transitions under the guidance of influential leaders like Amos L. Wedgeworth, whose leadership was pivotal in steering the bank through the fluctuations of the mid-20th century. Wedgeworth took the helm in 1936 and his tenure is noted for its enduring stability and growth, nurturing the bank’s resilience through the economic upheavals that included the latter part of the Great Depression and the post-World War II boom. Under his stewardship, Home Federal Bank expanded its services and solidified its commitment to the community, enhancing its portfolio of offerings and extending its geographic reach.

Throughout the 20th century, the bank embraced modernization, adopting technological advancements to enhance customer service and operational efficiency. This era saw the introduction of automated teller machines (ATMs), online banking services, and other technological innovations that transformed traditional banking practices. These efforts not only catered to the evolving needs of their customers but also positioned Home Federal Bank as a forward-thinking institution ready to meet future challenges. The legacy of these leaders, particularly Wedgeworth, left an indelible mark on the bank’s culture and operational philosophy, guiding it towards a path of sustained growth and community integration well into the 21st century.

Transition to Home Federal Bancorp (2010)

In 2010, Home Federal Bank made a strategic transformation into Home Federal Bancorp, a decision that marked a significant milestone in its long history. This transition to a holding company structure was driven by a variety of factors, primarily aimed at enhancing the bank’s ability to diversify its services and improve its financial stability. By becoming a holding company, Home Federal Bancorp gained the flexibility to create or acquire subsidiary companies that could offer a wider range of financial services beyond traditional banking, such as insurance and investment services. This broadened scope allowed the bank to tap into new revenue streams and better manage risks associated with economic fluctuations.

The impact of this transformation on business operations was substantial. It facilitated more robust capital management strategies and provided a more efficient organizational structure for managing the expanded range of services. Additionally, it improved the company’s ability to raise capital and invest in growth opportunities without the constraints that typically accompany a traditional bank structure. Overall, the shift to a holding company model enabled Home Federal Bancorp to strengthen its competitive position in the marketplace, enhancing its capability to serve the evolving needs of its customers and community more effectively.

Growth and Expansion

Branch and Service Expansion

Home Federal Bank’s journey of growth and expansion, particularly in terms of its branch network and service offerings, has been a testament to its adaptability and commitment to reaching a broader customer base. Over the decades, starting notably in the mid-20th century, the bank systematically broadened its footprint, initially deepening its presence within Louisiana before extending beyond state lines.

The expansion strategy was characterized by a thoughtful blend of opening new branches and acquiring smaller banks, a move that allowed Home Federal Bank to penetrate new markets while consolidating its offerings in existing ones. Each new branch was strategically located to capture a mix of residential, commercial, and industrial clientele, thereby diversifying its customer base and spreading its risk portfolio.

Simultaneously, Home Federal Bank expanded its service offerings to include more comprehensive financial products tailored to meet the diverse needs of its growing clientele. This included the introduction of business banking services, personal and commercial loans, and later, wealth management and insurance services through its subsidiaries. Such expansions were not only a response to the growing demands of the market but also aligned with the bank’s goal to provide holistic financial solutions under one umbrella.

This expansion was supported by investments in technology and staff training, ensuring that the quality of service at new branches matched the high standards set by the bank’s original locations. By the early 2000s, Home Federal Bank had established a robust network of branches that not only covered a significant part of Louisiana but also had presence in key strategic locations in neighboring states, cementing its role as a regional leader in financial services.

Overall, the careful and strategic expansion of branches and services helped Home Federal Bank build a resilient and versatile financial institution, capable of serving a wide array of financial needs and contributing significantly to regional economic development.

Technological Advancements

Home Federal Bank’s adoption of online and mobile banking technologies marked a crucial pivot in its approach to customer service and banking convenience. As the digital landscape evolved, the bank recognized the necessity of integrating these technologies to stay competitive and meet the growing expectations of its customers.

The introduction of online banking allowed customers to perform a variety of financial transactions remotely, such as checking account balances, transferring money, paying bills, and managing loans. This level of accessibility was not just a convenience but a transformation in how customers interacted with their finances, providing them the ability to manage their accounts around the clock without the need to visit a branch.

Following the advent of online banking, Home Federal Bank further expanded its technological repertoire by embracing mobile banking. This move was in response to the increasing use of smartphones and the demand for on-the-go banking solutions. The mobile banking app included features similar to those of the online banking platform but optimized for mobile devices, offering functionalities like mobile check deposits, real-time notifications, and location services to find nearby ATMs or branches.

These technological advancements significantly enhanced customer satisfaction by providing seamless, efficient, and secure access to banking services. They also allowed Home Federal Bank to reduce operational costs and allocate resources more effectively. For instance, with more routine transactions being handled online or via mobile, bank staff could focus on higher-value services and personalized customer engagement.

Moreover, the adoption of these digital solutions helped Home Care Federal Bank attract a younger demographic, who tend to prefer digital interactions for managing their finances. It also played a crucial role in maintaining customer loyalty by aligning the bank’s services with the convenience and efficiency expected in the modern digital era. Overall, the strategic implementation of online and mobile banking technologies not only strengthened Home Federal Bank’s market position but also reinforced its commitment to enhancing customer service and operational efficiency.

Community Impact and Recognition

Community Involvement

Over the years, Home Federal Bancorp, Inc. of Louisiana has demonstrated a profound commitment to its community through a variety of significant initiatives and programs. The bank has been a staunch supporter of educational advancement, offering scholarships and financial support to local schools to foster educational opportunities, especially in underserved communities. Additionally, it has engaged in community development projects aimed at revitalizing neighborhoods and stimulating local economies, including financing affordable housing and supporting small businesses with flexible lending options and financial literacy programs.

Home Federal has also prioritized health and wellness by sponsoring health fairs and partnering with local healthcare providers to offer free or affordable health screenings, promoting preventive care and healthy living. Moreover, the bank has taken steps to support environmental sustainability, highlighting its role in building a stronger and more resilient community. Through these efforts, Home Federal Bancorp, Inc. of Louisiana underscores its enduring legacy of trust and service as it celebrates a century of commitment to its community.

Awards and Honors

Throughout its history, Home Federal Bancorp, Inc. of Louisiana has garnered several prestigious awards and honors that reflect its commitment to excellence and community service. The bank was prominently listed in Money Magazine as one of the most trustworthy financial institutions, which underscores its integrity and dedication to customers’ financial well-being. Additionally, Home Federal has been the recipient of the Community Partnership Award, a testament to its active involvement and positive impact within the local community. This award highlights the bank’s efforts in initiating programs that support local businesses, enhance health and education, and foster community development. These recognitions not only celebrate the bank’s achievements but also reinforce its role as a pillar of support and a trusted partner in the community. As it marks its 100-year anniversary, these accolades serve as milestones that commemorate its ongoing legacy of trust and superior service.

The Acquisition: A New Chapter

Details of the Acquisition by Great Western Bank (2015)

In 2015, Home Federal Bank was acquired by Great Western Bank in a move that marked a significant consolidation in the banking sector. This acquisition was driven by strategic growth ambitions of Great Western Bank, aiming to expand its presence and deepen its market penetration in the Southeastern United States. The decision to merge was influenced by the synergistic potential to combine Home Federal Bank’s strong local relationships and Great Western’s broader array of financial products.

Key figures in the transaction included the CEOs and CFOs of both banks, who were pivotal in negotiating terms and overseeing the seamless integration of operations. These leaders focused on aligning the corporate cultures and operational systems to ensure continuity for customers and employees alike.

The transition process was carefully managed to maintain service continuity. Extensive measures were taken to integrate banking systems, align product offerings, and provide thorough communication to both staff and customers about what the changes would mean for them. Training sessions were held to familiarize Home Federal Bank’s staff with Great Western Bank’s systems and corporate culture, ensuring a smooth transition that preserved the legacy of customer care excellence Home Federal was known for. This acquisition ultimately positioned Great Emerging Bank as a more formidable player in the banking industry, with enhanced capabilities and a larger geographical footprint.

Impact of the Acquisition

The acquisition of Home Federal Bank by Great Western Bank in 2015 had a profound impact on its services, community involvement, and overall legacy. Post-acquisition, Great Western Bank was able to leverage Home Federal Bank’s strong community ties and extensive network to expand its service offerings, introducing a broader range of financial products that included advanced investment and wealth management services previously unavailable to Home Federal’s clientele.

One significant change was the enhancement of digital banking services. Great Western introduced more sophisticated online and mobile banking platforms to Home Federal’s customer base, improving user experience and access to banking services. This technology upgrade was crucial in keeping pace with the digital transformation trends in the financial sector, providing customers with the convenience of modern banking amenities such as mobile deposits, real-time notifications, and personalized financial management tools.

Community involvement, a cornerstone of Home Federal Bank’s identity, continued under Great Western’s stewardship but with increased resources. Great Western upheld Home Federal’s legacy of community engagement by continuing to support local charities, nonprofits, and community projects. They expanded these efforts by leveraging larger-scale corporate social responsibility programs, which allowed for greater impact and outreach in the communities they served.

Moreover, the legacy of Home Federal Bank as a trusted community institution was preserved through the retention of many of its branches and employees, providing continuity for customers. Great Western recognized the value of Home Federal’s local brand equity and continued to operate under the Home Federal name in many locations, ensuring that the legacy of personalized service and local involvement remained intact.

Overall, while the acquisition brought significant changes, it also created opportunities for growth and enhancement of services, ensuring that the legacy of Home Federal Bank continued to evolve in line with modern banking demands and community needs.

Legacy and Continuing Influence

Enduring Impact on Local Banking

The enduring impact of Home Federal Bank on the local banking sector remains significant, even after its integration into Great Western Bank. The foundational principles and practices established by Home Federal have continued to influence the banking industry, particularly in terms of community engagement, customer service, and conservative financial management.

Home Federal Bank was known for its deep commitment to the communities it served, a trait that has perpetuated through its successor. This legacy is evident in the continued emphasis on local relationships and personalized banking services that cater to individual and local business needs. Such practices have set a standard in the sector, influencing other banks to prioritize community involvement and customer-centric services as key components of their business models.

Moreover, Home against Federal’s prudent management practices, particularly in risk management and financial stability, have become benchmarks for other institutions. Its conservative approach to lending and investment has been instrumental in illustrating the importance of maintaining sound financial practices, which has proven especially valuable during economic downturns.

The bank’s legacy is also reflected in the continued professional development of its employees and the leadership roles they undertake in the broader banking community. Many former executives and staff members have gone on to influence the industry by advocating for policies and practices that promote financial integrity and responsible banking.

Continuation under New Management

The essence of Home Federal Bank has been carefully preserved and integrated within the operations and culture of Great Southwestern Bank following the acquisition. This preservation is evident in several key areas that highlight the continuity of Home Federal’s core values and operational philosophy.

Customer Service and Community Focus: Home Federal Bank was renowned for its exceptional customer service and strong community ties. Great Western Bank has embraced these principles, continuing to offer personalized banking experiences that prioritize customer relationships. This commitment is reflected in the ongoing community banking activities, where decisions are still made locally, and banking officials are familiar faces in the communities they serve.

Employee Retention and Development: In an effort to maintain continuity, Great Western Bank retained a significant number of Home Federal’s staff during the transition. This strategic decision helped preserve the cultural and operational ethos of Home Federal, ensuring that the longstanding traditions of employee engagement and development continued. Furthermore, these employees bring a depth of knowledge and a sense of legacy that enrich the corporate culture at Great Western Bank, fostering a workplace environment that values history and continuity.

Philanthropic and Community Initiatives: Home Federal Bank’s legacy of community involvement lives on through Great Western Bank’s enhanced support for local initiatives. Great Western has not only continued but also expanded Home Federal’s programs and sponsorships, from local charity events to significant community development projects. This expansion demonstrates an ongoing commitment to the welfare and growth of the local communities that Home Federal once served.

Operational Practices: The operational practices of Home Federal, known for their conservatism and focus on long-term stability, have been integrated into the broader strategic framework of Great Western Bank. These practices now inform the bank’s approach to risk management, lending, and financial planning, helping to secure a stable and prosperous future for the bank and its stakeholders.

By weaving these aspects of Home Federal’s identity into its own, Great Western Bank has ensured that the spirit of Home Superior Federal Bank continues to influence its operations and corporate culture, proving that the acquisition was not just a merger of assets but also a blending of values and traditions.

Home Federal Bank Overview

Home Federal Bank (HFBL), established in 1924, crafted a business model that significantly emphasized community-oriented banking, merging traditional banking services with a deep commitment to local development. This model was centered on providing comprehensive financial services tailored to the needs of individuals, families, and businesses within the communities it served, thereby fostering economic growth and stability.

Community-Centric Services: HFBL’s services extended beyond typical banking offerings such as savings and checking accounts, to include mortgages, business loans, and investment services. What set HFBL apart was its approach to service delivery, which was highly personalized and adapted to the unique needs of its community members. This personalized service not only helped in building lasting relationships but also in achieving customer loyalty and trust, which are critical in the banking industry.

Economic Impact: HFBL played a pivotal role in stimulating local economies. By providing loans and credit to small businesses, the bank supported entrepreneurship and helped sustain local job markets. Additionally, its mortgage services enabled homeownership, which is a key driver of community stability and development.

Community Engagement: Beyond its economic contributions, HFHL was deeply involved in community affairs, sponsoring local events, and supporting charitable organizations. This engagement helped in building a solid reputation as a community pillar, not just a financial institution. The bank’s commitment to community welfare was evident in its responsiveness to local needs, often tailoring its programs and initiatives to support various community-driven projects.

Financial Education: Recognizing the importance of financial literacy in sustaining economic growth and personal financial health, HFBL actively engaged in educational initiatives aimed at providing community members with the knowledge and skills needed to manage their finances effectively. These initiatives included workshops, seminars, and school programs, which contributed to a more informed and financially savvy community base.

Overall, HFBL’s business model was a blend of traditional banking and proactive community involvement. Its significant impact on the communities it served went beyond financial transactions; it was about creating a supportive network that contributed to mutual growth and prosperity. This approach not only distinguished HFBL in the banking sector but also entrenched its legacy as a community-focused institution.

The Investment Case for HFBL

Home Federal Bank (HFBL) presents an attractive option for the “A Dollar A Day” investment strategy due to its compelling combination of steady dividend payouts, a strong community banking model, and a consistent financial performance.

Dividend Reliability: HFBL has a history of providing shareholders with stable and reliable dividends, making it an ideal candidate for investors focused on generating passive income. This is particularly appealing for the “A Dollar A Day” strategy, where the aim is to build a portfolio that not only grows in value but also delivers a steady income stream through dividends. HFBL’s track record of dividend payouts reflects its financial health and commitment to returning value to its shareholders.

Financial Stability: HFBL’s business model is grounded in community banking, a sector known for its resilience and stability. Community banks like HFBL typically maintain conservative lending practices and have a deep understanding of their local markets, which reduces risk and enhances stability. For investors adding a daily dollar to their investment portfolio, this stability is crucial as it mitigates risk while providing a dependable growth trajectory.

Growth Potential: Despite its traditional focus, HFBL has demonstrated adaptability and growth, expanding both its services and geographic footprint. This growth not only ensures that the bank remains competitive but also indicates potential for capital appreciation. Investors in the “A Dollar A Day” strategy can benefit from both the income generated through dividends and the potential increase in the stock’s value over time.

Community Impact: Investing in HFBL also means contributing to a business model that values community impact and development. For socially conscious investors, this aligns with the goal of ensuring that their investment has a positive impact on society. HFBL’s commitment to supporting local businesses and initiatives fosters economic growth and community development, which can be a compelling aspect for investors who value ethical and sustainable investment practices.

Home Federal Bank (HFBL) has a commendable dividend history that makes it an appealing choice for an investment strategy focused on steady income generation. Historically, HFBL has consistently paid dividends, reflecting its robust financial management and commitment to shareholder returns. The regularity and reliability of these dividends are particularly important for the “A Dollar A Day” strategy, as the accumulation of these dividends can significantly contribute to the portfolio’s income stream over time.

HFBL’s approach to dividends is conservative yet progressive, with incremental increases that align with the bank’s earnings growth. This strategy ensures that dividend payouts remain sustainable while providing investors with a predictable and growing income. This makes HFBL a prime candidate for a portfolio aimed at not only preserving capital but also generating income through dividends, which can be reinvested to compound growth.

HFBL’s financial health is solid, characterized by a strong balance sheet, prudent risk management, and consistent profitability. These factors are crucial in sustaining dividend payments and are indicative of a well-managed institution capable of navigating various economic conditions. Such financial stability reassures investors of the bank’s ability to maintain or increase dividend payouts in the future.

As for the dividend yield, HFBL offers a competitive rate when compared to industry standards. While its yield may not be the highest in the banking sector, it is attractive given the bank’s stability and lower risk profile. The yield is sufficiently appealing for long-term investors looking to benefit from both dividend income and potential capital appreciation.

HFBL’s Dividend Details

Dividend Policy: Home Federal Bank (HFBL) has maintained a disciplined and consistent dividend policy, focused on delivering regular shareholder returns while maintaining sufficient capital reserves for growth and stability. The policy prioritizes sustainable dividend payments that reflect the bank’s financial health and profit generation capabilities, supporting both stability and shareholder confidence.

Historical Dividend Payments and Growth: Over the past decade, HFBL has demonstrated a robust pattern of dividend growth. The dividends have seen a gradual increase from $0.06 per share in 2011 to $0.125 per share by 2024. This steady growth in dividend payments underscores HFBL’s ongoing profitability and effective financial management. The ability to consistently raise dividends is indicative of the bank’s operational success and commitment to returning value to its shareholders.

Dividend Yield Compared to Industry Standards: HFBL’s dividend yield, while generally conservative, is competitive within the financial sector, particularly among community banks. The yield has remained attractive relative to industry standards, offering a balanced return to investors looking for income in addition to potential capital appreciation. Although not the highest in the sector, HFBL’s yield is appreciated for its stability and reliability, making it a solid choice for income-focused investors.

Stability and Sustainability of Dividends: HFBL’s dividends are characterized by their stability and sustainability, factors that are critically important for long-term investors. The bank’s conservative approach to financial management, including maintaining strong capital and liquidity ratios, ensures that it can continue to pay dividends even in less favorable economic conditions. This resilience is bolstered by HFBL’s strategic focus on core banking operations and prudent risk assessment, further enhancing the reliability of its dividends.

Monthly Investment Strategy

Investing $1 Daily Accumulation Strategy:

Investing $1 daily into a portfolio translates into a simple yet effective strategy for gradually building an investment in Home Federal Bank (HFBL). By setting aside one dollar each day, an investor accumulates $30 over the course of a month (assuming a typical 30-day month). This accumulated sum is then used to purchase shares of HFBL on a monthly basis. The simplicity of this method allows investors, especially those new to investing or with limited resources, to participate in the stock market consistently.

To implement this strategy effectively, investors might choose to use a brokerage account that allows fractional share purchasing due to the price of HFBL shares possibly exceeding the monthly savings amount. This enables every dollar saved to be fully invested, maximizing the potential for growth and ensuring that even small amounts of money are continually working for the investor.

Projecting Growth of the Investment:

The growth of this investment strategy can be projected by considering two key components: compounding dividends and capital appreciation.

- Compounding Dividends:

- As HFBL pays dividends, these payments can be reinvested into purchasing more shares of HFBL, which in turn will generate their own dividends. Over time, this compounding effect can significantly increase the number of shares owned and the total value of the dividend income. For instance, if HFBL pays a dividend of $0.125 per share quarterly, reinvesting these dividends will gradually increase the holdings each quarter, enhancing the investment’s overall growth through compounding.

- Capital Appreciation:

- In addition to the dividends, the strategy also benefits from potential capital appreciation of HFBL shares. If the bank continues to perform well, demonstrating solid financial health and profitability, the market value of its shares is likely to increase. This appreciation would be reflected in the higher market price of the shares over time, adding to the investment’s total return.

When combined, these two factors—compounding dividends and capital appreciation—can lead to significant growth in the investment portfolio, even with a modest daily contribution of $1. To illustrate, starting with a minimal investment, the accumulated and reinvested dividends along with any increase in share price can grow the portfolio to a substantial sum over a period of years. This strategy is particularly appealing for long-term investors looking to build wealth gradually while minimizing daily financial impact.

This monthly investment strategy, using a consistent daily contribution towards purchasing HFBL shares, showcases how disciplined, long-term investing can lead to meaningful financial outcomes through the power of compounding and the steady growth of a well-chosen investment.

Benefits of Consistent Investing in HFBL

Investing consistently in a stable dividend-paying stock such as Home Federal Bank (HFBL) provides several key benefits:

- Stable Income Stream: Dividend-paying stocks like HFBL offer investors a predictable and regular income stream. This is particularly appealing for those who need consistent income, such as retirees, or for investors who are looking to build their wealth over time.

- Lower Risk: Companies that regularly pay dividends are often more mature and financially stable. This stability often translates into lower volatility in the stock price, making such investments less risky compared to non-dividend-paying stocks or high-growth companies whose future is more speculative.

- Reinvestment Opportunity: Dividends provide an opportunity for reinvestment. By automatically reinvesting dividends to purchase additional shares of HFBL, investors can benefit from the compounding effect, where not only do your original investments grow, but the reinvested dividends do as well, accelerating the growth of your investment over time.

- Tax Advantages: Dividend income often enjoys favorable tax treatment compared to other types of income, such as interest income. For instance, qualified dividends may be taxed at a lower rate than regular income, providing a tax-efficient way to generate income.

*2. How Consistent Investing in HFBL Leads to Significant Passive Income Over Time:

Investing consistently in a dividend-paying stock like HFBL can lead to significant passive income due to the compounding effect of dividends and the potential appreciation of the stock itself:

- Building Shares through Dividends: As dividends are paid out and reinvested, the number of shares an investor holds increases. Each new share acquired also begins generating dividends, and over time, this growth in share count can significantly increase the total dividend income received.

- Growth of Dividend Payments: Companies with a history of stable or increasing dividends tend to continue this trend. As HFBL grows and its financial health improves, it may increase dividend payments, further enhancing the income an investor receives. This growth in dividends can be a significant source of increasing passive income.

- Capital Appreciation: While the primary focus might be on dividend income, the potential appreciation of the stock cannot be overlooked. As HFBL continues to perform well, the underlying value of the shares may increase, leading to capital gains in addition to the dividends received.

- Long-Term Financial Security: The combination of regular dividend income and potential capital gains provides a strong foundation for long-term financial security. This strategy can help investors build a substantial nest egg over time, reducing financial stress and providing funds that can be tapped into during retirement or other phases of life.

- Inflation Protection: Dividend-paying stocks often provide a measure of protection against inflation. As the cost of living increases, companies may raise prices, potentially leading to higher profits and subsequently, higher dividend payments. This increase can help maintain the purchasing power of your investment income over time.

HFBL’s Role in a Diversified Portfolio

Fitting HFBL into a Larger Diversified Investment Portfolio:

Home Federal Bank (HFBL) can play a critical role in a diversified investment portfolio, providing both stability and steady income. Here’s how HFBL fits into a broader investment strategy:

- Risk Management: HFBL, as a stable dividend-paying stock, can help balance the risk in an investment portfolio that may also contain higher-volatility securities such as growth stocks, international equities, or commodities. The predictable nature of its dividend payments can act as a buffer during market downturns when riskier assets might underperform.

- Sector Allocation: Including HFBL in a portfolio adds exposure to the financial sector, specifically the community banking segment. This sector often reacts differently to economic changes compared to technology or consumer goods sectors, thereby providing additional diversification benefits.

- Income Generation: For portfolios designed to generate income, HFBL contributes positively with its consistent dividend payouts. This is particularly valuable for income-focused investors such as retirees or those seeking cash flow from their investments.

- Long-Term Growth Potential: While HFBL offers stability, it also presents long-term growth potential through its strategic expansions and community-focused business model. This balanced approach allows investors to benefit from both income and potential appreciation, enhancing total returns over time.

2. HFBL’s Role as a Stable Income Generator Amidst More Volatile Investments:

In a diversified portfolio, HFBL serves as a stabilizing force, especially important amidst more volatile investments:

- Consistency in Dividend Payments: HFBL has a history of regular, reliable dividend payments. This consistency is crucial during economic uncertainties when more cyclical or speculative investments might falter. Regular dividends can provide a steady cash flow, helping to smooth out the returns of a portfolio that includes more volatile stocks.

- Lower Volatility: Community banks like HFBL typically exhibit lower volatility compared to the broader market. This stability is due to their localized business models and conservative management practices, which focus on sustainable growth and risk management. Investing in HFBL can thus reduce the overall volatility of an investment portfolio, providing a safer return profile.

- Counterbalancing Effect: During periods of high market turbulence, sectors like technology or consumer discretionary can experience significant swings. HFBL’s stock can act as a counterbalance within a portfolio during such times, providing steadiness and mitigating large fluctuations in portfolio value.

- Defensive Nature: Financial stocks, particularly well-managed community banks like HFBL, are often considered defensive investments because they can maintain performance even in challenging economic climates. Their operations, centered around fundamental banking services, are essential and continue regardless of the economic cycle, adding an element of defensive positioning to an investment portfolio.

Conclusion

Investing in Home Federal Bank (HFBL) through the “A Dollar A Day” strategy offers a compelling approach to building wealth gradually but surely. This strategy underscores the value of consistency and patience in investing, particularly for those who may be starting with smaller amounts or seeking a low-risk entry into the stock market.

Recapping the Benefits of Including HFBL: HFBL presents an excellent case for inclusion in a “A Dollar A Day” strategy due to its steady dividend payouts, financial stability, and a strong community banking model. The consistency of HFBL’s dividends provides a predictable income stream, which is key for investors looking to build up their investment gradually. Additionally, HFBL’s focus on conservative growth and community engagement translates into lower volatility and sustainable long-term growth. These characteristics make HFBL an ideal choice for those who are new to investing or those who prefer a cautious approach to building their financial portfolio.

Encouragement for Long-Term Gains from Steady, Small-Scale Investments: Small, consistent investments can compound into significant sums over time, a principle that is at the heart of the “A Dollar A Day” strategy. By investing just one dollar daily into HFBL, investors can tap into the power of compounding dividends and capital appreciation. This method not only cultivates a habit of regular saving but also demonstrates how incremental investments can lead to substantial financial growth.

The journey of investing is often as important as the destination. Starting small with HFBL allows investors to participate in the financial markets with minimal risk while learning the ropes of investment management. Over time, this strategy can significantly enhance financial literacy and confidence, empowering investors to make more informed and ambitious investment decisions.

In conclusion, consider the long-term advantages of integrating HFBL into your investment strategy. Its reliable dividends and stable growth offer a foundation for building wealth that can withstand market fluctuations and yield substantial returns. Embrace the discipline of saving and investing a dollar a day—it’s a simple step that can lead to profound financial rewards. Whether you’re saving for retirement, building an emergency fund, or just trying to grow your wealth, the “A Dollar A Day” strategy with HFBL is a prudent and promising approach to achieving your financial goals.