I. October 2025 Market & Dividend Landscape: Easing Rates Meet AI Momentum

October 2025 Dividend Portfolio Update (DP.18)

I. October 2025 Market & Dividend Landscape: Easing Rates Meet AI Momentum

Market Summary: The fourth quarter kicked off with equity markets near record highs. The S&P 500 advanced briskly through Q3 (up 8.1% for the quarter and +14.8% year-to-date) , and the Nasdaq likewise surged on the back of tech strength. By early October, both indices were taking a breather just shy of their late-September peaks. A slight uptick in volatility emerged mid-month as investors digested new economic data and some profit-taking, but overall sentiment remains far more positive than a year ago. Notably, the Federal Reserve has shifted to an easing stance: after delivering a 0.25% rate cut in September (the first of the cycle) to the 4.00–4.25% range , futures markets anticipate at least one more quarter-point cut by year-end . This dovish turn is bolstering hopes for a “soft landing,” even as the Fed balances lingering 2.9% inflation with growth concerns.

AI Sector Developments: The AI revolution remains a central driving force. Tech companies continue to report outsized gains from AI-driven products and services, though October saw a momentary pause in the AI stock rally as valuations caught their breath. Still, the fundamental trend is intact – enterprise and consumer adoption of AI is accelerating across industries. Dell Technologies (DELL), for example, recently raised its long-term growth targets and reiterated an annual ≥10% dividend growth commitment through 2030 , underscoring its confidence in AI-fueled demand for infrastructure. Similarly, Intuit (INTU) – which we added to our portfolio this month – showcased the strength of the AI-enhanced fintech sector. Intuit’s FY2025 report and investor day revealed ~$18.8B revenue with free cash flow of $6.1B, of which $4B was returned to shareholders via dividends and buybacks . Intuit even announced a 15% dividend hike (to $1.20/quarter) as it projects double-digit growth into FY2026 . These examples highlight how high-quality tech names are translating AI tailwinds into tangible shareholder returns.

Investor Sentiment: Despite robust market gains, investor sentiment turned more cautious as October progressed. The CNN Fear & Greed Index slipped from neutral (~50) a month ago to about 30 (“Fear”) by mid-October , reflecting concerns over rising long-term bond yields and geopolitical headlines. In general, we view this dip in sentiment as a healthy reset. Some froth came off the hottest tech stocks, and defensive sectors caught a bid as investors rotated toward safety. Importantly, dividend-paying stocks have held up well – their reliable income provides comfort amid any short-term jitters. Overall, the backdrop remains accommodative for dividend growth investors: a more supportive Fed, strong corporate earnings (especially in tech/AI), and still-rising dividends are combining to offer both growth and income. Our strategy in this environment continues to stress balance – enjoying the upside from innovation-driven growth while relying on dividend stalwarts for stability, all while staying alert to macro risks (inflation surprises, Fed missteps, etc.). The tone is one of guarded optimism as we head into year-end.

II. Portfolio Performance & Allocation – October Update

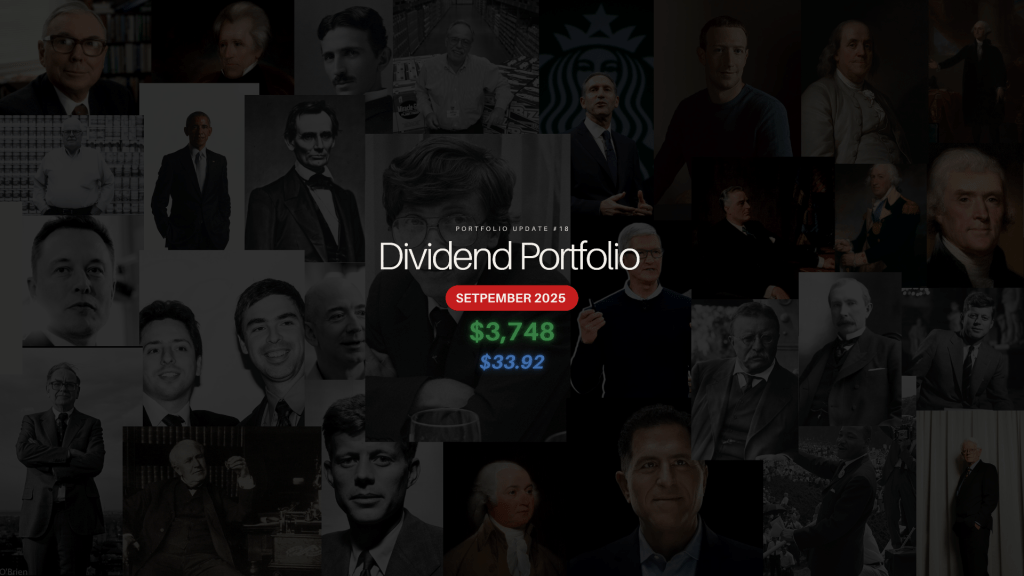

Portfolio Value: As of this update, my Roth IRA dividend portfolio totals $5,260.23, a significant increase from last month. This jump owes largely to new contributions (more on that below) and solid market appreciation across many holdings. Equity holdings now amount to $3,778.48, with the remaining $1,481.76 (28%) in cash as dry powder. I’m keeping a healthy cash reserve on hand to capitalize on any volatility or buying opportunities the market offers – a prudent move given October’s uptick in fear. The stock portion of the portfolio has an unrealized gain of $320.17 (+9.3%), meaning our investments are up about 9% on cost so far. This reflects both price appreciation and the careful selection of companies that have held their value in choppier waters. Notably, tech positions drove much of the portfolio’s upside in recent weeks, offsetting flat-to-slightly-down moves in some defensive names.

Notable Movers: The standout contributor on the upside was Dell Technologies (DELL). Riding on stellar earnings and bullish AI guidance, DELL’s stock has climbed strongly – it’s now one of our top gainers with a double-digit percentage increase since purchase. Our mega-cap tech holdings (Microsoft, Apple, Alphabet, Meta) also continued their strong 2025 run, though they paused in early October along with the broader Nasdaq. On the other end, a few traditionally defensive stocks lagged: for instance, American States Water (AWR) saw its price dip a bit this month (higher bond yields often pressure utility stocks), and Becton Dickinson (BDX) traded sideways as healthcare remains out of favor. These price softness in defensives are not concerning to us; they’re largely a function of sector rotation, and meanwhile those companies keep delivering steady earnings and dividends. Our community bank holdings – Home Federal Bancorp of Louisiana and FS Bancorp – were relatively stable, providing little drama (just how we like from income workhorses). In sum, the portfolio’s diversification did its job: tech and fintech gains boosted our total value while dividend payers in other sectors provided stability when momentum trades cooled.

Current Holdings (18 stocks): The portfolio remains split across 18 dividend-paying positions. Below is a breakdown by sector, including each holding and current share count:

• Technology (~50% of equity): Intuit (INTU) – 1 share, Microsoft (MSFT) – 1, Apple (AAPL) – 1, Alphabet (GOOGL) – 2, Meta (META) – 1, Dell Technologies (DELL) – 3.

• Financials (~30% of equity): Visa (V) – 1, Mastercard (MA) – 0.5 (half share), Home Fed. Bancorp of LA (HFBL) – 18, FS Bancorp (FSBW) – 4, First Savings Financial Group (FSFG) – 1.

• Defensive (~10% of equity): American States Water (AWR) – 1, Costco (COST) – 0.2 (fractional share), Becton Dickinson (BDX) – 0.2.

• Other (~10% of equity): Starbucks (SBUX) – 1, Automatic Data Processing (ADP) – 0.6, Waste Management (WM) – 0.45, Hamilton Beach Brands (HBB) – 0.1.

(Share counts reflect small fractional holdings in a few cases – a strategy of nibbling into positions even with limited funds. For example, we started with a fractional share of HBB to track the stock and will scale up over time.)

This diversified mix spans high-growth tech, stable financials, and defensive plays. Tech remains the largest allocation (~half the stock portfolio), a deliberate tilt given the secular growth and dividend initiation we’re seeing in names like Intuit, Alphabet, and Meta. Financials are ~30%, including our community bank trio and the payment giants Visa/Mastercard – these provide reliable income and some cyclical upside. The defensive slice (~10%) covers utilities, healthcare, and consumer staples, which add ballast (AWR’s regulated water business, BDX’s healthcare products, Costco’s staple retail model). The remaining “other” ~10% includes unique dividend growers like SBUX, ADP, and WM that don’t neatly fit traditional sectors but offer strong cash generation and dividend histories. We’re comfortable with this allocation for now; it achieves a balance between growth and safety. Going forward, I may deploy some of the cash into underweight areas (perhaps adding to defensives if valuations improve) to keep the portfolio well-rounded.

Equity vs. Cash: The 72%/28% split between stocks and cash is a bit more conservative than last update. This is intentional – given October’s rise in volatility, I trimmed the pace of new stock purchases and let cash accumulate. That said, I’m eager to put cash to work in high-conviction ideas if the market pulls back further. Having nearly $1.5k on the sidelines gives me flexibility. It’s worth noting that this cash drag does weigh on our current total returns (as seen in the ~0.95% overall portfolio yield below), but I view it as an “opportunity fund” ready to fuel future gains.

III. Dividend Income: $50 and Climbing 🥳

Forward Annual Income: I’m thrilled to report that our projected annual dividend income now stands at $50.03! Crossing the $50 mark is an exciting milestone for this small but growing portfolio – especially considering it was about $33.92 just a month ago . In practical terms, the portfolio should generate roughly $4.17 per month in passive income going forward (on average, though actual monthly receipts will vary). While $4 a month won’t pay any bills yet, the trend is our friend: the income is up ~47% month-over-month, reflecting the powerful combo of new contributions and dividend increases. We’ve essentially accelerated our dividend machine by almost a year’s worth of growth in just these past several weeks.

Yields on Cost and Value: The influx of fresh capital and dividend hikes has nudged our yield on cost (YOC) to ~1.4%, meaning the portfolio yields about 1.4% on the money we’ve invested so far. This YOC is higher than it was in September (around 1.1% ), thanks to recent dividend bumps and opportunistic buys at reasonable prices. The current yield on market value (i.e. yield on the $3,778 equity portion) is about 1.3%, a bit lower than YOC because many of our stocks have appreciated – a good problem to have! When including the large cash reserve, the yield on total portfolio value comes out to only 0.95%, reflecting the drag of idle cash. I expect this figure to rise once we deploy more cash into dividend-payers. Our focus isn’t on chasing high yield, however; it’s on steady dividend growth. In fact, many of our tech positions yield under 1% currently – but their dividend growth rates are stellar, which will boost our YOC over time.

Dividend Increases – Key Developments: October brought a flurry of dividend raises from our holdings, underscoring why we love this strategy of growing income:

• Starbucks (SBUX) – Declared its 15th consecutive annual increase, bumping the quarterly payout from $0.61 to $0.62 per share . It’s a modest +1.6% raise (SBUX is prioritizing reinvestment in growth), but still a nice token from this consumer giant. The new dividend will hit at the end of November.

• Microsoft (MSFT) – Approved a hefty 9.7% increase in its quarterly dividend, from $0.83 to $0.91 per share . This boosts MSFT’s forward yield to ~1.0%. The higher dividend kicks in with the December payment, and it marks Microsoft’s 21st year of consecutive raises – a testament to its cash generation.

• Costco (COST) – Back in spring, Costco quietly delivered a 13% dividend hike, raising its quarterly payout to $1.30 . We benefited from that increase in our forward income this quarter (Costco last paid us in August). While Costco typically announces dividend moves once a year (and none this fall), it remains one of our fastest-growing income sources thanks to that April raise.

• Dell Technologies (DELL) – No new increase this month (Dell’s big 15% hike came earlier in the year), but importantly the company reiterated its policy of ≥10% annual dividend growth through FY2030 . This explicit commitment gives us confidence that Dell will keep rewarding shareholders as its AI-driven earnings grow. We’re counting on those double-digit raises from Dell to turbocharge our income.

• American States Water (AWR) – Announced an 8.3% raise to its quarterly dividend (now $0.504/share) this summer , which we are now reflecting fully in our forward income. AWR has one of the longest dividend growth streaks in existence (69 years!), and it continues to deliver solid high-single-digit bumps like clockwork.

• Automatic Data Processing (ADP) – ADP typically announces its increases in November, so we’re on watch. Its last hike (late 2024) was a robust ~10% jump to $1.54 quarterly, and ADP has increased its dividend for 50 consecutive years (an esteemed Dividend King). While we haven’t seen a new raise yet in 2025, ADP’s consistent double-digit dividend CAGR is a cornerstone of our portfolio’s growth engine.

• Home Federal Bancorp (HFBL) – Our micro-cap bank quietly notched its 12th straight annual dividend increase, holding the quarterly rate at $0.135 after a raise earlier this year . It may not move the needle much in dollar terms, but seeing any growth from our smaller banks in a tough environment is encouraging.

In aggregate, these dividend hikes added several dollars to our forward annual income. Just to quantify a few: Microsoft’s raise gives us an extra ~$0.32 per share annually, AWR’s about +$0.04 per share quarterly, and Starbucks’ +$0.01 quarterly adds up to +$0.04 a year per share. It’s the combination of many such increases (big and small) that drives our snowball. As of now, the portfolio’s weighted dividend growth rate is hovering in the high single-digits percent – an excellent figure that far outpaces inflation and should lead to exponentially higher income if sustained.

New Contributions & Buys: The big news on this front was the initiation of Intuit (INTU) as a new position. I contributed fresh capital to the Roth IRA and purchased Intuit in mid-October, just in time to receive its increased dividend. This move added $4.80 to our forward income (INTU’s new annual payout) in one go. Intuit is a lower-current-yield (~0.7%) name, but I’m attracted to its 15% dividend growth and huge free cash flow (as noted, they’re returning billions to shareholders) . It fits perfectly into our “compounders” bucket. Aside from INTU, I also modestly increased our stake in ADP (another low-yield, high-growth dividend stalwart) and a few fractional additions here and there using leftover cash. I refrained from major buys in the latter half of October given the market’s elevated levels – hence our higher cash allocation – but I stand ready to pounce if volatility presents bargains.

Upcoming Dividends (Cash Infusion Ahead): We have a couple of notable payouts pending in the next weeks which will boost our cash balance further: Dell goes ex-dividend around October 20th for its $0.525 quarterly payout, which will be paid on Oct 31. With our shares, that will translate into a nice chunk of change coming Halloween day. Also, Mastercard (MA) just went ex-dividend on Oct 9 (for $0.76 per share) and will pay on Nov 7 . Even with our half-position, we’ll see that cash land soon. These incoming dividends – along with October receipts from some of our smaller holdings – will be promptly reinvested. My strategy is to compound the income by reinvesting: in some cases via automated DRIP (Dividend Reinvestment Plans) on positions I find attractively valued, and in other cases by pooling the cash to manually buy whichever stock offers the best opportunity. For instance, we have DRIP active on a few lower-valued names like AAPL, V, and COST to accumulate fractional shares automatically . Meanwhile, I’ll likely take the Dell and MA dividend cash and add to either an underweight holding or even a new position if one catches my eye. The goal is to make every dollar work and accelerate that forward income trajectory.

All told, our portfolio’s dividend income is in great shape: a $50+ annual run-rate, a ~1.3% current yield that should rise as we deploy cash, and a collection of businesses that are regularly hiking their payouts. The “dividend snowball” is still small, but it’s undeniably picking up speed.

IV. Month-Over-Month Progress and Evolving Strategy

Income Growth (DP.17 vs DP.18): The leap from $33.92 to $50.03 in forward income represents a +47% increase in one month, which is extraordinary. Several factors drove this surge: (1) the new capital I injected (primarily into INTU and ADP) immediately raised our income base, (2) the dividend hikes from MSFT, SBUX, AWR, etc., layered on additional dollars, and (3) small reinvestments and rounding up of fractional shares are now contributing a few extra cents. To put it in perspective, in September our portfolio was generating about $2.83 per month on average – now it’s about $4.17. That kind of month-over-month jump is uncommon (and not something to expect regularly), but it shows the combined power of market opportunity + proactive investing. It’s especially satisfying because it brings us that much closer to longer-term goals; for example, the next milestone might be $100/year in income, and we essentially covered half that distance in a single bound.

Portfolio Changes: In terms of holdings, the core list of stocks remains the same aside from the addition of Intuit. I did not sell any positions – a key aspect of my approach is low turnover. We’re in this for accumulating assets, not trading. The only adjustments were incremental: increasing some positions slightly and letting portfolio weights shift naturally with market movements. One noticeable change is that our Tech sector weight increased (from roughly 45% to ~50% of equities) while Financials’ weight dipped a bit (from ~35% to ~30%). This was intentional: most of the new contribution went into tech/fintech names, and tech stock appreciation outpaced that of banks over the month. I’m comfortable with tech around half the portfolio given the caliber of companies we hold (many are quasi-monopolies in their domains). The financials bucket is still substantial, providing yield and diversification, but I didn’t add new money there this month. Our Defensive/Other segment shrank slightly in percentage terms – not because we sold anything, but simply because tech grew larger. As mentioned, I may allocate some new cash into those lagging sectors in the coming months to keep a balance. For example, I have my eye on a couple of high-quality defensive names that could complement AWR and COST if their valuations become attractive.

Strategy Shifts: Strategy-wise, there’s been no radical change – I remain committed to the philosophy of blending growth and income. However, I would highlight a subtle shift: I’m leaning even more into dividend growth vs. high current yield. The purchase of INTU (yield <1%) and the continued buildup of low-yield names like MSFT and ADP reflect my priority for long-term growth of income over short-term yield. This doesn’t mean I’ll avoid all high-yield opportunities, but they have to meet quality criteria. In fact, our highest yielding positions (the micro-cap banks) taught us a lesson recently: one needs to monitor them closely for dividend safety. (On that note, I corrected a data error from last time – FS Bancorp’s quarterly dividend is $0.28, not $0.50 – a reminder to always double-check data!). We’ll continue to hold HFBL, FSBW, FSFG as they pay reliably, but I won’t overweight such names just to chase yield . Instead, the plan is to rebalance with intent, not emotion: ensure our mix aligns with the goal of maximizing income growth over current yield . Right now, I believe it does – our portfolio’s bias toward names like INTU, MSFT, META, GOOGL, DELL (balanced by stalwarts like AWR, COST, V) is well-suited for that goal . If my goals were to change (say I suddenly needed higher immediate income), I would consider shifting into telecoms, utilities, or REITs; but at this stage, I prefer to keep riding the compounders.

Another minor strategic point: With the market’s fear gauge up, I’m holding more cash as noted. This is a tactical decision; it doesn’t signal any bearish market call, but it does acknowledge that after such a strong year-to-date rally, having liquidity is valuable. Should we get a 5-10% market dip (which isn’t uncommon in Q4 historically), I’ll be ready to deploy that cash into quality names that go “on sale.” My watchlist includes adding to existing positions on weakness – for example, adding to Apple or Visa if they pull back to more attractive yield levels, or initiating a new defensive position to bolster that side of the portfolio. In essence, the strategy remains: stay invested, but stay flexible. We never want fear to paralyze us, but we also want to have options when opportunity knocks.

V. Outlook & Personal Reflections – Balancing Optimism with Discipline

Looking ahead, I remain optimistic yet vigilant. The remainder of 2025 will bring some important events for our portfolio: Big Tech earnings are on deck, which will likely move stocks like Microsoft, Apple, and Alphabet (and by extension our portfolio value). Early indications show continued strength in cloud, advertising, and consumer tech spending, which bodes well – but we’ll watch for any slowdown signals. The Federal Reserve’s next meetings and any additional rate cuts (or a surprise pause) will also be key; a smoother rate environment would be a tailwind for our financials and high-yield plays. On the flip side, I’m mindful of macro risks: an unexpected spike in inflation or an external shock could spur volatility. Our plan there is simply what we’ve been doing – focus on company fundamentals. Companies with solid balance sheets, real earnings, and loyal customers tend to ride out macro storms, and I’ve centered the portfolio around such names.

From an investor’s personal perspective, I have to say it’s incredibly gratifying to see this dividend journey progress. Hitting the $50 annual income mark in October was a feel-good moment – it may be small in absolute terms, but it represents the compound growth of my efforts and strategy. I recall that at the start of the year, the portfolio’s income was around half this amount. The fact that it’s doubled through consistent investing and dividend growth reinforces my conviction in this approach. Every dollar of dividend is a dollar that works for me, and as those dollars get reinvested, they’ll generate more dollars – the snowball is slowly rolling. There’s a genuine passion I have for this process of building a passive income stream, and it keeps me disciplined even when markets get noisy. For example, during the brief market wobbles in October, instead of worrying, I found myself eagerly checking for dividend announcements and ex-dates – because those are signals of tangible progress toward my goals, independent of daily price moves. Using tools like DivTracker to monitor upcoming paydays and updates has been immensely helpful in this regard . It keeps me focused on the endgame: a steadily rising income.

In closing, the portfolio is on a strong trajectory as we enter the final stretch of 2025. The mix of AI-powered growth stocks and dividend stalwarts is delivering both capital appreciation and income expansion – exactly as intended. My plan is to stay the course: continue reinvesting dividends, selectively deploy the cash reserve, and perhaps initiate one or two new positions (I’m researching a few candidates in the industrial and healthcare sectors that could complement our holdings). I’ll also continue to document this journey in these updates, sharing the wins, losses, and learnings. If this month taught me anything, it’s the importance of patience and balance. By blending high-growth dividend payers with reliable income generators, I didn’t have to choose one or the other – the portfolio is achieving growth and income together. As an investor, that’s incredibly satisfying and motivating. Here’s to finishing 2025 on a high note, with an eye on compounding our results further in the months and years to come. We’ll check back with DP.19 next month – and until then, I’ll keep grinding, saving, and investing, one dividend at a time.

Thanks for reading and happy investing!

Sources:

0) TL;DR (what actually matters)

- INTU just hiked the dividend 15% to $1.20/qtr (record Oct 9, 2025, payable Oct 17, 2025). Dividend growth track is intact; cash returns remain a priority.

- FY25 scorecard for INTU: revenue $18.8B; Investor Day reiterated double‑digit FY26 growth and shows FY25 free cash flow ≈ $6.1B with **$4B** returned to shareholders. Translation: dividend coverage is comfy.

- Data hygiene note: One item in the pasted DP.17 needs correcting—FSBW’s quarterly dividend was $0.28, not $0.50. Keep the tracker clean or it will lie to you.

1) INTU: Dividend quality, coverage, and sustainability (D.18 focus)

Status: Healthy dividend‑growth profile with low payout and high cash visibility.

- New run‑rate DPS: $4.80/year (from $1.20/qtr). Board approved Aug 21; pay Oct 17 to holders of record Oct 9.

- Coverage math: FY25 FCF ≈ $6.1B; company returned ~$4B to shareholders (dividends + buybacks). Dividend piece (~$1B in FY25) implies a modest FCF payout, leaving plenty for reinvestment and buybacks.

- Context: Management still guiding to double‑digit top‑line and margin expansion into FY26; the premium multiple keeps the yield small but the raises big—classic dividend‑growth stock, not a high‑yield play.

Bottom line: Keep INTU in the “compounding engine” bucket. Let the dividend growth and buybacks do the heavy lifting while resisting yield‑chasing.

2) Upcoming & recent paydays (as of Oct 11, 2025)

- INTU – $1.20 qtr; record Oct 9, pay Oct 17.

- MSFT – Paid $0.83 on Sep 11 (ex‑date Aug 21). Board raised to $0.91 for the Dec 11 payment (ex‑date Nov 20).

- META – $0.525; record Sep 22, pay Sep 29 (done).

- GOOGL/GOOG – $0.21; ex‑date Sep 8, paid Sep 15.

- V (Visa) – $0.59; ex‑date Aug 12, paid Sep 2. Next declaration pending.

- AAPL – $0.26; ex‑date Aug 11, paid Aug 14. Next typically hits mid‑Nov after late‑Oct declaration.

- COST – Quarterly raised to $1.30 in April; last paid Aug 15. Watch for the next board action.

- DELL – $0.525 qtr; reiterated policy to grow the dividend ≥10% annually through FY2030.

- HFBL – $0.135; paid Aug 18 (12th straight annual increase).

- FSBW – $0.28; 50th straight quarterly dividend (plus a special).

- AWR – $0.504 (raised 8.3%); paid Sep 3.

3) Portfolio dividend table (latest declared run‑rates)

| Ticker | Quarterly DPS | Fwd DPS (annual) | Latest known ex‑date | Notes |

|---|---|---|---|---|

| INTU | $1.20 | $4.80 | Oct 9, 2025 | 15% hike; pay Oct 17. |

| MSFT | $0.91* | $3.64 | Nov 20, 2025* | *Board raised from $0.83; $0.91 starts with Dec payment. |

| META | $0.525 | $2.10 | Sep 22, 2025 | Paid Sep 29. |

| GOOGL | $0.21 | $0.84 | Sep 8, 2025 | Paid Sep 15. |

| V | $0.59 | $2.36 | Aug 12, 2025 | Paid Sep 2. |

| AAPL | $0.26 | $1.04 | Aug 11, 2025 | Paid Aug 14; next typically mid‑Nov. |

| COST | $1.30 | $5.20 | Jul 31, 2025 | Last paid Aug 15. |

| DELL | $0.525 | $2.10 | (varies) | Guidance to grow ≥10%/yr through FY2030. |

| HFBL | $0.135 | $0.54 | Aug 4, 2025 | 12th straight annual raise; paid Aug 18. |

| FSBW | $0.28 | $1.12 | Jul 22, 2025 | 50th straight quarterly dividend; special declared. |

| AWR | $0.504 | $2.016 | Aug 15, 2025 | +8.3% y/y; paid Sep 3. |

Use this as the baseline “D.18 sheet.” If your actual share counts differ, multiply Fwd DPS by your shares to get forward income. Keep this table current and you’ll never miss an ex‑date again.

4) Quality & risk notes (straight talk)

- Coverage > optics. INTU’s dividend is tiny on yield, but coverage is excellent thanks to that ~$6.1B FY25 FCF and consistent repurchases. That’s exactly what you want in a compounding core.

- Policy clarity helps. DELL explicitly committed to ≥10% annual dividend growth through FY2030—rare corporate honesty that helps planning.

- Bank micro‑caps (HFBL/FSBW). Dependable, but thinly traded. Track payout ratios and credit quality; don’t overweight illiquid names just because the checks show up on time. (Latest amounts cited above.)

- Utility ballast. AWR keeps quietly compounding with regulated cash flows and annual bumps; it’s your “dividend spine” while tech stays spicy.

5) Zero‑drama execution checklist (do these, then go live your life)

- Lock the calendar. Add the INTU Oct 17 pay date and MSFT Nov 20/Dec 11 dates to your tracker; roll 48‑hour alerts before each ex‑date.

- Clean the data. Fix FSBW to $0.28 in your sheet; annotate that July PR noted the 50th consecutive dividend (and special).

- DRIP where it’s cheap. If your broker offers no‑fee DRIP, consider enabling on low‑cost names (AAPL, V, COST) to auto‑reinvest fractional shares.

- Rebalance intent, not vibes. If your goal is income growth > current yield, your mix (INTU/MSFT/META/GOOGL/DELL + AWR/COST/V) is aligned. If you want higher present yield, add a measured utility/telecom/pipe sleeve instead of overweighting micro‑caps.

- Quarterly audit. After every board season: update DPS, check payout ratios, and re‑rank positions by “dividend safety x growth runway.”

6) What to monitor next

- INTU guidance drift (Mailchimp and TurboTax variability can ding near‑term optics; management still guiding to double‑digit FY26). If they reaffirm, you’re golden.

- DELL AI cycle vs. margins (long‑term targets lifted; dividend growth commitment reiterated—watch execution).

- Big Tech cadence (MSFT’s raise to $0.91, META/GOOGL regularity). If these stay boring, your compounding won’t be.

Receipts (key sources)

- Intuit Q4/FY25 press + 8‑K + dividend history.

- Intuit Investor Day slides (FCF ~$6.1B; ~$4B returned).

- Microsoft dividend (Jun $0.83; Sep raise to $0.91).

- Alphabet dividend (ex‑date Sep 8, $0.21).

- Meta dividend ($0.525; record Sep 22; pay Sep 29).

- Visa dividend ($0.59; ex‑date Aug 12).

- Apple dividend ($0.26; ex‑date Aug 11; pay Aug 14).

- Costco dividend ($1.30; increased Apr 2025).

- Dell dividend ($0.525; ≥10%/yr growth commitment).

- HFBL dividend ($0.135; paid Aug 18).

- FSBW dividend ($0.28; 50th straight; special).

- AWR dividend (+8.3% to $0.504; paid Sep 3).