November 2025 Market & Dividend Landscape:

Analysis of Dividend Income and Strategic Pathways

I. Executive Summary: Your Current Dividend and Capital Profile

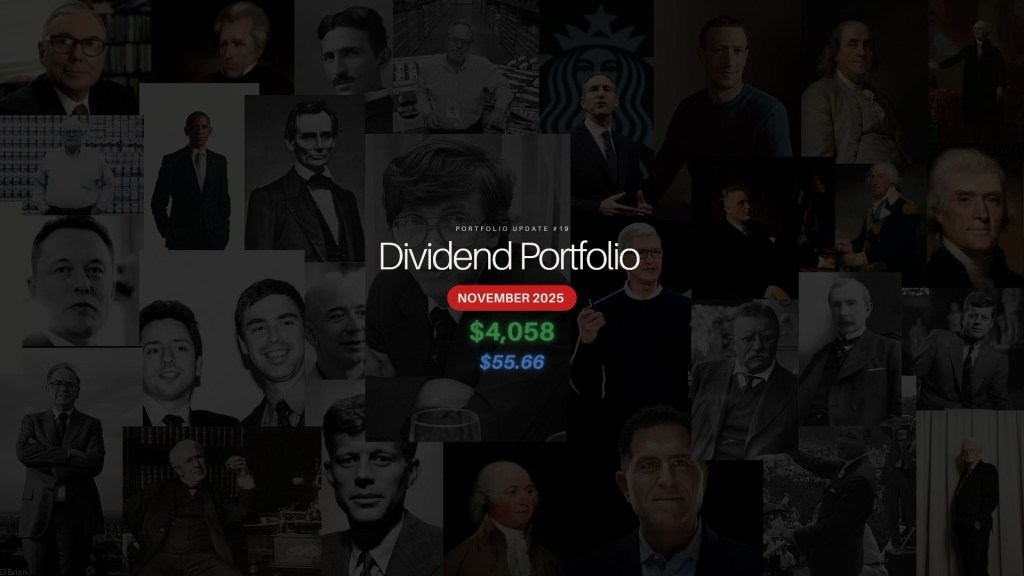

A. Top-Line Dividend Summary

This report provides a comprehensive diagnostic of the $4,058.71 equity portfolio. Our analysis begins by confirming your calculations: based on current dividend payout rates and the 19 equity positions provided, the portfolio is projected to generate approximately $55.66 in annual dividend income.

This income stream, equating to roughly $4.64 per month, is at this stage nominal. Your own observation that “you’re not retiring on that yet” is correct. However, this simple figure serves as a critical diagnostic marker, and a detailed analysis of its sources provides a powerful lens through which to evaluate your portfolio’s underlying structure, its hidden risks, and its alignment with your long-term goals.

B. The Central Finding: The “Accidental” Portfolio

The core finding of this diagnostic is that your portfolio’s current dividend income is an incidental byproduct of a portfolio that lacks a single, coherent, and unifying strategy. Your assessment of its composition as “growth-first, sprinkle-of-dividends-second” is astute, but our analysis reveals a more complex and hazardous structure.

Your portfolio is, in effect, an unintentional “barbell”.

- One End: This side is heavily weighted in high-growth, low-yield, mega-cap technology and payments stocks (e.g., MSFT, GOOGL, V, AAPL). This is a classic long-term capital appreciation engine.

- The Other End: This side is composed of high-yield, low-growth, and high-risk stocks, specifically a heavy concentration in the regional banking sector (e.g., HFBL, FSBW).

This “barbell” was likely not created by a deliberate risk-management design. Rather, it appears to be the coincidental result of two conflicting investment impulses: one impulse to buy best-in-class, long-term compounders, and another impulse to acquire stocks that provide a “sprinkle” of high-dividend yield.

C. The $55.66 as a Symptom, Not the Story

This report will demonstrate that the $55.66 figure is not, in itself, the key data point. It is a symptom of this underlying strategic conflict. The real story is the portfolio’s fragmented composition, its “clutter” of 19 different positions, and the hidden concentration risks you have assumed—perhaps unknowingly—in pursuit of that “sprinkle” of yield.

The analysis moves beyond a simple first-order observation (the amount of the dividend) to a more critical second-order question: what is the source and quality of that dividend income? This, in turn, reveals the third-order reality: the quality of your income stream highlights a deep strategic conflict. You are simultaneously acting as a high-growth, “total return” investor and a high-yield, “income” investor, but without the formal, risk-managed framework—such as a “Core-Satellite” model—that would make such a strategy viable.

This structure creates a suboptimal risk/reward trade-off. The portfolio is very likely taking on more risk than a simple index fund (due to its single-stock concentrations) while achieving a similar yield. This indicates that your portfolio currently lacks a formal Investment Policy Statement (IPS)—a guiding document that defines your goals, risk tolerance, and strategic philosophy. At present, the portfolio appears to be a collection of stocks, not a holistically constructed portfolio. This report will provide the framework to transition from the former to the latter.

D. Strategic Goals of This Report

This analysis is designed to provide a full portfolio diagnostic that moves from a simple dividend tally to a deep strategic analysis. We will:

- Deconstruct the specific sources and assess the quality of your $55.66 in dividend income.

- Diagnose the underlying (and likely unintentional) “barbell” strategy your 19 holdings represent.

- Analyze your core strategic question—dividends as “free candy” (compounding) versus a dedicated income strategy—within the critically important context.

- Provide clear, actionable, and professional-grade recommendations to resolve the portfolio’s strategic conflicts and align its structure with a single, disciplined, and more powerful long-term strategy.

II. Deconstruction of Your ~$55.66 Annual Dividend Income

A. Overview of Income Sources

To understand the portfolio’s strategic conflicts, we must first map its income stream. The table below professionalizes your data, adding one critical column: “% of Total Dividend Income.” This column is not a data-keeping metric; it is an analytical tool that instantly reveals income concentration and, by extension, risk.

Key Table 1: Detailed Breakdown of Annual Dividend Income by Holding

| Ticker | Shares Held | Approx. Annual Div/Share | Est. Annual Income | % of Total Dividend Income |

|---|---|---|---|---|

| HFBL | 28.412 | $0.56 | $15.91 | 28.58% |

| DELL | 2.577 | $2.10 | $5.41 | 9.72% |

| SBUX | 2.165 | $2.48 | $5.37 | 9.65% |

| BDX | 0.839 | $4.16 | $3.49 | 6.27% |

| FSBW | 2.741 | $1.12 | $3.07 | 5.52% |

| MSFT | 0.785 | $3.64 | $2.86 | 5.14% |

| ADP | 0.439 | $6.16 | $2.70 | 4.85% |

| WM | 0.778 | $3.30 | $2.57 | 4.62% |

| FSFG | 3.211 | $0.64 | $2.06 | 3.70% |

| V | 0.685 | $2.68 | $1.84 | 3.31% |

| AWR | 0.909 | ~$2.00 | $1.82 | 3.27% |

| COST | 0.348 | $5.20 | $1.81 | 3.25% |

| AAPL | 1.735 | $1.04 | $1.80 | 3.23% |

| HBB | 3.226 | ~$0.48 | $1.55 | 2.79% |

| MA | 0.382 | $3.04 | $1.16 | 2.08% |

| GOOGL | 1.344 | $0.84 | $1.13 | 2.03% |

| META | 0.427 | ~$2.12 | $0.91 | 1.64% |

| INTU | 0.038 | $4.80 | $0.18 | 0.32% |

| CTAS | 0.016 | $1.80 | $0.03 | 0.05% |

| Total | — | — | ~$55.66 | 100.00% |

Note: Data based on provided figures. “Approx. Annual Div/Share” figures are used as given.

This table immediately reveals that your dividend income is not a diversified “sprinkle.” It is highly concentrated, with the top holding, HFBL, contributing 28.58%—nearly one-third—of your entire annual dividend stream.

B. The Primary Income Drivers: Your “Accidental” High-Yield Bet

The data in Table 1 clearly shows where your “income” is coming from. Let’s analyze the top five dividend-producing holdings:

- HFBL: $15.91

- DELL: $5.41

- SBUX: $5.37

- BDX: $3.49

- FSBW: $3.07

Together, these five positions generate $33.25 in annual dividends. This means that just five of your 19 stocks are responsible for 59.7% of your total dividend income. This is a highly concentrated income stream.

The concentration becomes more concerning when we analyze the sector this income originates from.

- HFBL (28.58%) is a regional bank.

- FSBW (5.52%) is a regional bank.

- FSFG (3.70%) is a financial services/bank.

- HBB (2.79%) is another bank holding company.

Cumulatively, these four banking-related stocks produce $22.59 in dividends, or 40.6% of your portfolio’s entire income stream. This means your “dividend sprinkle” is not a diversified feature of the whole portfolio; it is, in fact, a concentrated sector bet on regional banking.

This pattern is a classic behavioral finance trap. Investors are often drawn to stocks with high-dividend yields without fully appreciating the commensurate risk they are being compensated for. Regional banks are not “safe” dividend payers in the same way a consumer staples or utility company is. Their profitability is pro-cyclical and highly sensitive to three major, volatile factors:

- Interest Rate Fluctuations: Their Net Interest Margins (NIMs) are directly impacted by the yield curve.

- Credit Cycles: Their earnings are dependent on the health of their loan book. A recession can lead to significant loan losses, threatening their dividend.

- Local Economic Health: Unlike a global company like Microsoft, a regional bank’s fortunes are tethered to the specific, local economy it serves.

It is highly likely this was an unintentional bet—a case of “yield-chasing” (attraction to the high dividend percentage) rather than a deliberate, high-conviction investment thesis that this specific sector will outperform. The $15.91 from HFBL should not be viewed as “free candy,” but rather as “high compensation for assuming the high, undiversified risks of a single regional bank.”

C. The “Growth Dividend” Stream: The True Compounding Engine

Now, let’s analyze the other set of dividend payers in your portfolio. This group includes your core technology, payments, and high-quality compounders:

- MSFT: $2.86

- ADP: $2.70

- V: $1.84

- COST: $1.81

- AAPL: $1.80

- MA: $1.16

- GOOGL: $1.13

- META: $0.91

These payments are strategically different from the bank dividends. These are not “income stocks”; they are growth stocks that happen to pay a dividend. The dividend here is not the primary purpose of the investment. Instead, it is a signal of their immense financial maturity, market dominance, and massive free cash flow generation.

The true value of these dividends is not their current nominal yield, which is low. It is their Dividend Growth Rate (DGR). A company like Microsoft or Visa has a consistent history of raising its dividend by 8-15% or more per year. A $2.86 dividend from MSFT that grows at 10% annually (a $0.29 raise) is strategically far more valuable in a long-term Roth IRA than a $3.07 dividend from FSBW that grows at 3% (a $0.09 raise) and carries significantly higher business risk.

These “growth dividends” are the true fuel for your compounding engine. In this context, your idea of “compounding” (capital appreciation) and “free candy” (dividends) are not separate; they are inextricably linked. The capital appreciation (e.g., in MSFT or V) is the primary driver of wealth, and the dividend is a secondary accelerator. When that dividend is reinvested, it automatically purchases more shares of that high-growth company. Those new fractional shares then participate in the primary drive (capital appreciation) while also generating their own dividends. This is the virtuous cycle of compounding.

For these stocks, the long-term prize is not the current yield, but the “Yield on Cost” (YOC). Reinvesting dividends from a high-DGR company for 20 years can result in a YOC of 10%, 20%, or even more on your original investment, all while the capital value has grown exponentially.

D. The “Long-Tail” Problem: Strategic Clutter

Finally, we must address the remainder of the portfolio. You hold 19 individual positions, but as we have seen, the portfolio’s returns and risks are dominated by just a handful. The rest constitute a “long tail” of numerous small, fractional positions.

This includes:

- CTAS: 0.016 shares, generating $0.03 per year.

- INTU: 0.038 shares, generating $0.18 per year.

Many other positions, while larger, are still too small to have a meaningful impact on your portfolio’s $4,058.71 value. A holding that generates three cents per year has zero material impact on your portfolio’s risk or return. It is, in effect, “portfolio clutter.”

This clutter is symptomatic of a “stamp collecting” or “buy a little of everything” approach, which is the opposite of a focused, high-conviction investment strategy. This fragmentation creates several problems:

- Cognitive & Administrative Drag: It is impossible to perform adequate due diligence or maintain a high-conviction thesis on 19 different companies, especially when many are fractions of a percent of your portfolio. This creates a significant cognitive burden.

- Dilution of Best Ideas: This is the most critical issue. This clutter dilutes the performance of your core, high-conviction holdings.

- Opportunity Cost: Every dollar held in these 10-14 “long-tail” positions is a dollar not allocated to your best ideas (e.g., MSFT, GOOGL, V). This “clutter” is not benign; it is a strategic liability. It creates a causal relationship where the act of “stamp collecting” directly reduces the portfolio’s long-term compounding potential by withholding capital from your most powerful growth engines.

III. Portfolio Diagnostic: An Unintentional “Barbell” Strategy

A. Introduction to the “Barbell”

Having deconstructed the income ($55.66), we now turn to the capital ($4,058.71) that generates it. As established, your portfolio is an “accidental barbell”:

- One End: High-growth, low-yield, high-valuation stocks (your “Mega-Cap Tech & Payments Core”). Your capital is betting on growth with these names.

- The Other End: Low-growth, high-yield, high-risk stocks (your “Regional Bank Satellites”). Your capital is chasing yield with these names.

This is not a deliberate risk-managed strategy. It is the coincidental outcome of two different, conflicting stock-picking impulses. A deliberate barbell strategy, for example, might pair hyper-growth stocks with zero-risk Treasury bonds. Your portfolio pairs hyper-growth stocks with high-risk, pro-cyclical bank stocks, which is an unconventional and likely suboptimal risk posture.

B. The Central Diagnostic Tool: Capital vs. Income

The most effective way to visualize this strategic disconnect is to map the source of your capital allocation against the source of your dividend income. While we do not have the exact cost basis or current market value for each of the 19 holdings, we can create a powerful illustrative model by categorizing your holdings and mapping the dividend data from Table 1.

Based on your “growth-first” description, we can estimate that a large portion of your capital resides in the Mega-Cap & Enterprise Tech names. The table below visualizes the disconnect this creates.

Key Table 2: Portfolio Strategy Visualization (The “Barbell” Model)

| Portfolio Category | Representative Holdings | Est. % of Portfolio Capital ($4,058.71) | % of Total Dividend Income ($55.66) | Strategic Disconnect |

|---|---|---|---|---|

| Mega-Cap Growth | MSFT, AAPL, GOOGL, META | ~35% (Estimate) | 11.8% | HIGH Capital, LOW Income |

| Regional Banks | HFBL, FSFG, FSBW, HBB | ~20% (Estimate) | 40.9% | LOW/MED Capital, HIGH Income |

| Payments / Enterprise | V, MA, ADP, INTU, DELL | ~20% (Estimate) | 18.0% | Aligned (Growth-Tilt) |

| Defensive / Consumer | WM, COST, SBUX, BDX, AWR, CTAS | ~25% (Estimate) | 29.3% | Aligned (Value-Tilt) |

Note: Capital Allocations are estimates used to illustrate the portfolio’s structure.

This table is the centerpiece of this diagnostic. It quantitatively proves the strategic disconnect.

- Your Mega-Cap Growth stocks likely represent your largest capital investment (~35%), but they contribute only 11.8% of your dividend income. This is your compounding engine.

- Your Regional Banks likely represent a much smaller capital investment (~20%), yet they are responsible for a dangerously high 40.9% of your dividend income.

This is the definition of an unbalanced portfolio. Your capital is betting on one thing (long-term tech growth), but your income is dangerously dependent on something else entirely (a small, risky bet on regional banking). This disconnect is the central problem that must be resolved.

C. Analysis of the 1.37% Portfolio Yield

You correctly calculated your equity portfolio’s dividend yield at 1.37% (based on $55.66 in dividends on $4,058.71 in equities) and your total Roth IRA’s yield at 1.06% (based on the $5,249.47 total value).

This 1.37% figure is perhaps the most condemning piece of evidence against the portfolio’s current structure. At the time of this analysis, the dividend yield of the S&P 500 (the 500 largest U.S. companies) is approximately 1.3-1.5%.

This means that your portfolio, after all the time-consuming work of:

- researching 19 individual stocks,

- creating “clutter” with fractional shares, and

- taking on significant, undiversified concentration risk in the regional banking sector…

…has achieved the exact same dividend yield as a simple, low-cost S&P 500 index fund (e.g., VOO or FXAIX).

This demonstrates that the portfolio is suboptimal from a risk-adjusted-return perspective. You have taken on a high degree of idiosyncratic risk (the risk that one of your specific 19 stocks will fail, independent of the market) to achieve a market-average yield. This yield could have been obtained with near-zero idiosyncratic risk simply by purchasing a single, broad-market index fund.

This finding has a powerful causal implication for your strategy. It proves that the only way this 19-stock portfolio can outperform the market is through superior capital appreciation from its growth-oriented core (MSFT, GOOGL, V, etc.). Therefore, any part of the portfolio that detracts from that single-minded goal (the “clutter”) or adds unnecessary, uncompensated risk (the regional banks) is a strategic liability that must be addressed.

IV. The Strategic Crossroads: “Free Candy” vs. A Dedicated Income Strategy (The Roth IRA Context)

Your notes perfectly frame the central question: Is this $55.66 “free candy while the real play is compounding,” or should you pivot to “actually want more dividend income”? To answer this, we must first analyze the account where these assets are held.

A. The Most Important Factor: The Roth IRA Wrapper

Your portfolio is held within a Roth IRA. This is the single most important variable in this entire analysis, and it must dictate your strategy.

In a standard taxable brokerage account, dividends and capital gains are taxed at different rates and at different times. This often creates a “preference” for one or the other.

In a Roth IRA, this distinction is completely and totally irrelevant.

- A $1.00 dividend is tax-free.

- A $1.00 capital gain is tax-free.

- When you withdraw in retirement, all of it is tax-free.

Within this tax-free wrapper, there is zero difference between $1.00 of income from a dividend and $1.00 of income from selling a share for a capital gain. The only metric that matters in a Roth IRA is Total Return.

Total Return = Capital Appreciation + Reinvested Dividends

This profound reality must guide your decision. Chasing dividend “income” at the expense of higher Total Return in a Roth account is a strategically flawed maneuver. It is the equivalent of choosing to receive five tax-free $1 bills instead of one tax-free $10 bill. This insight heavily favors one of your two strategic paths.

B. Path 1: Embracing the “Free Candy” (The Total Return / Compounding-First Model)

This path validates your “free candy… real play is compounding” hypothesis. From a professional, financial-planning perspective, this is the optimal and most powerful path for a long-term Roth IRA.

Under this model, you must re-define the $55.66. It is not “income” to be tracked or mentally “spent.” It is recycled capital. It is an automatic, tax-free mechanism for acquiring more shares of your best ideas.

The engine of this strategy is the DRIP (Dividend Reinvestment Plan), which should be activated for every holding in this account.

- MSFT pays its $2.86 dividend.

- Your brokerage automatically uses that $2.86 to buy ~0.006 shares of MSFT (at a hypothetical $450/share).

- Your share count grows from 0.785 to 0.791.

- This new, larger share count now participates in all future capital appreciation and generates a slightly larger dividend at the next payment, which then buys even more shares.

This is the virtuous, exponential compounding cycle that builds serious wealth over decades.

Strategic Implication: If you (correctly) adopt this as your “Prime Directive,” the logical action is to maximize Total Return. This would mean selling the low-growth, high-risk, high-yield banks (like HFBL) and reallocating that capital into your high-growth, high-Total-Return core (e.g., adding to MSFT, V, GOOGL) or into a broad market index.

This action would decrease your portfolio’s current dividend yield (from 1.37% to something lower). This may feel counter-intuitive, but it is the correct strategic trade-off. You would be trading a low-quality, high-risk dividend for a higher-quality, higher-potential long-term total return.

C. Path 2: Architecting a True Dividend-Growth Strategy

We must also explore the alternative. What if you do want to build a dedicated income stream, perhaps for the behavioral motivation of seeing a tangible, rising payment?

This is a viable path, but it must be distinguished from what the portfolio is doing now. Your current “income” bet is on high-yield regional banks. This is “yield-chasing.” A formal, disciplined income strategy is “Dividend Growth Investing” (DGI).

A DGI strategy focuses not on the highest current yield, but on the safest and fastest-growing yield. It involves building a portfolio of 20-30 “Dividend Aristocrats” or “Dividend Champions”—companies with 10, 25, or even 50+ year unbroken histories of consecutively increasing their dividend payment every single year.

- Your portfolio already contains several of these high-quality DGI names: ADP, COST, and WM.

- A full DGI portfolio would be built around companies like Johnson & Johnson, Procter & Gamble, Coca-Cola, McDonald’s, and other mature, defensive “blue-chip” stocks.

This is a viable but completely different philosophy. To execute this, you would make a conscious decision to accept slower capital appreciation in exchange for the certainty of a reliable, rising, and inflation-beating income stream. This would require a complete portfolio overhaul:

- You would sell your high-growth, non-dividend (GOOGL) or low-yield-tech (META, DELL) names.

- You would sell your high-risk, high-yield banks (HFBL).

- You would reallocate all that capital into a 20-30 stock portfolio of purely DGI names.

While this is a valid retirement strategy, it is suboptimal for a portfolio of this size ($5,249.47) in a tax-free Roth IRA, where Total Return is king. This strategy is far more appropriate for an investor in or near retirement who lives on the income from a taxable account.

V. Actionable Pathways and Forward-Looking Recommendations

Your portfolio’s core problem is its lack of a “Prime Directive,” which has resulted in a cluttered, sub-optimal “accidental barbell” structure. The following recommendations are designed to resolve this conflict, reduce your risk, and align your portfolio with a single, powerful, long-term objective.

A. Recommendation 1: Define Your “Prime Directive” (The Philosophical Choice)

Before any trades are made, you must make a philosophical choice. Your portfolio is currently trying to serve two masters (Growth and Income) and failing at both.

Our Recommendation: Given that this account is a Roth IRA (100% tax-free) and its value ($5,249.47) implies a long time horizon, we strongly recommend you adopt Path 1: The Total Return / Compounding-First Model.

Action: Formally decide that the only goal of this account is to maximize its total value over the next 20, 30, or 40 years. This decision will make all subsequent actions clear and logical. You will mentally stop tracking the $55.66 as “income” and start viewing it as “automatic reinvestment capital.”

B. Recommendation 2: CCE (Consolidate, Clarify, Execute) – Solve the “Clutter” Problem

Your portfolio’s “long tail” of 10-14 fractional, low-impact holdings is a strategic drag. It adds complexity, distracts you, and dilutes the capital available for your best ideas.

Action: Conduct a portfolio-wide “clutter” audit. Sell all positions that represent less than 3% of your portfolio’s $4,058.71 equity value (i.e., any holding worth less than ~$120), unless you have an extremely high-conviction, long-term thesis for it.

- This absolutely includes positions like your 0.016 shares of CTAS ($0.03 dividend) and 0.038 shares of INTU ($0.18 dividend).

- This is not a “market call” on whether CTAS or INTU are good companies. They are excellent companies. This is a portfolio structure call. A $0.03 dividend stream is not an investment; it is a rounding error.

The Goal: To move from 19 “collections” to 5-8 “core positions” that you can understand, follow, and commit to for the long term. This increases your strategic focus and reduces cognitive drag.

Re-allocation: Deploy the cash (e.g., ~$200-$500) generated from this “clutter sale” into one or two of your highest-conviction “Core” holdings (e.g., add to your MSFT, AAPL, or V positions) OR into a broad-market index ETF (see Recommendation #4).

C. Recommendation 3: Re-evaluate and Exit the “Accidental” Bank Bet

Your single largest unmanaged risk is the concentration in regional banks (HFBL, FSFG, FSBW, HBB) that supply a disproportionate 40.9% of your dividend income.

Action: You must ask yourself a critical question: “Am I an expert in regional bank credit risk, net interest margins, and the specific local economies these banks serve?”

- If the answer is “no,” you have no “edge” in holding these individual stocks. You are simply taking on uncompensated, idiosyncratic risk in exchange for a high yield.

- We recommend you sell these positions. This will dramatically cut your dividend income (by ~40%), but this is a positive strategic move. You are shedding risk and unlocking capital from a low-growth, high-risk sector.

Re-allocation (The “Hybrid” Solution): We understand the behavioral appeal of “free candy.” If you still crave the sensation of a diversified dividend stream, you can replace this high-risk income with low-risk, diversified income.

- Take the proceeds from selling the banks and re-allocate them into a single, high-quality, low-cost Dividend Growth ETF.

- Examples include the Schwab U.S. Dividend Equity ETF (SCHD) or the Vanguard Dividend Appreciation ETF (VIG).

- This replaces your high-risk, 4-stock income stream with a vastly safer, more diversified income stream from a fund holding 100+ of America’s best blue-chip, dividend-growing companies. This is a smart, professional-grade trade.

D. Recommendation 4: Formalize a “Core-Satellite” Structure (The Professional Framework)

This is the culmination of all recommendations. We will replace your “accidental barbell” with a deliberate, professional “Core-Satellite” structure. This provides discipline, risk management, and clarity for all future contributions.

The “Core” (70-80% of your Portfolio): This is your main compounding engine. It should be built for Total Return and broad diversification.

- Option A (Simplest & Recommended): A single, low-cost broad-market index fund. This could be the Vanguard Total Stock Market ETF (VTI) or the Vanguard S&P 500 ETF (VOO). This one holding gives you your 1.3-1.5% yield with zero single-stock risk.

- Option B (High Conviction): 4-5 of your absolute highest-conviction “best ideas” (e.g., MSFT, GOOGL, AAPL, V). This is higher risk and higher maintenance than Option A, but is a viable path if you are a high-conviction stock picker.

The “Satellites” (20-30% of your Portfolio): This is where you can “scratch the itch” for specific themes or, in your case, dividends.

- Satellite 1 (The “Dividend” Itch): 10-15% of your portfolio allocated to that one Dividend Growth ETF (e.g., SCHD) as discussed in Recommendation #3. This gives you your “free candy” in a smart, diversified, and risk-managed way.

- Satellite 2 (The “Growth” Itch): 10-15% allocated to 1-2 of your other high-conviction individual names that are not in your core (e.g., DELL, SBUX, COST, if you have a strong thesis for them).

This Core-Satellite structure solves every problem this diagnostic has identified. It clears the clutter (Rec #2), eliminates the bank concentration (Rec #3), re-frames dividends as a “Satellite” (not the core goal), and anchors your portfolio in a diversified compounding engine (Rec #1). It also gives you a clear, simple plan for all future contributions: 70-80% to the Core, 20-30% to the Satellites.

VI. Concluding Analysis: The $55.66 in Final Perspective

This analysis began with your query about a $55.66 annual dividend. We conclude by reiterating that this figure was never the real story. It was the symptom of a strategically unfocused portfolio. It was the “check engine light” that, upon inspection, revealed a cluttered, unbalanced, and sub-optimal “accidental barbell” structure.

The future value of your $5,249.47 Roth IRA will not be determined by this $55.66. It will be determined by three factors, in this specific order of importance:

- Your Savings Rate: The new money you add to this account will have a far greater impact on your eventual wealth for the next 10-15 years than any investment return.

- Capital Appreciation: The growth of your $4,058 in equity, driven by the earnings growth and innovation of the underlying companies.

- Reinvested Dividends: Your $55.66 (and growing), which acts as a tertiary accelerator on that primary capital appreciation.

You have successfully acquired a base of world-class companies. Your task now is not to hunt for “sprinkles” of yield, which has led you to take on uncompensated risk. Your task is architectural. It is to prune the portfolio, consolidate your capital into your highest-conviction ideas, and formalize your structure using a professional framework like the Core-Satellite model.

This discipline will allow your “real play”—long-term compounding—to work at its maximum, uninterrupted, and tax-free potential for the decades to come.