Dividend Portfolio Review (Jan 2026): The “Growth Orchard” Strategy

Strategy: Quality Compounders & Dividend Growth

To fellow investors,

As we kick off 2026, it is time for a transparent look at the dividend portfolio. If you have been following along, you know this strategy isn’t built to chase the highest immediate yield. Instead, it is designed to own wonderful businesses that compound wealth tax-free in a Roth IRA.

At this stage, the portfolio is still small enough that every good decision matters, but the “snowball” is officially starting to roll. Here is the honest review of where we stand as of January 2026.

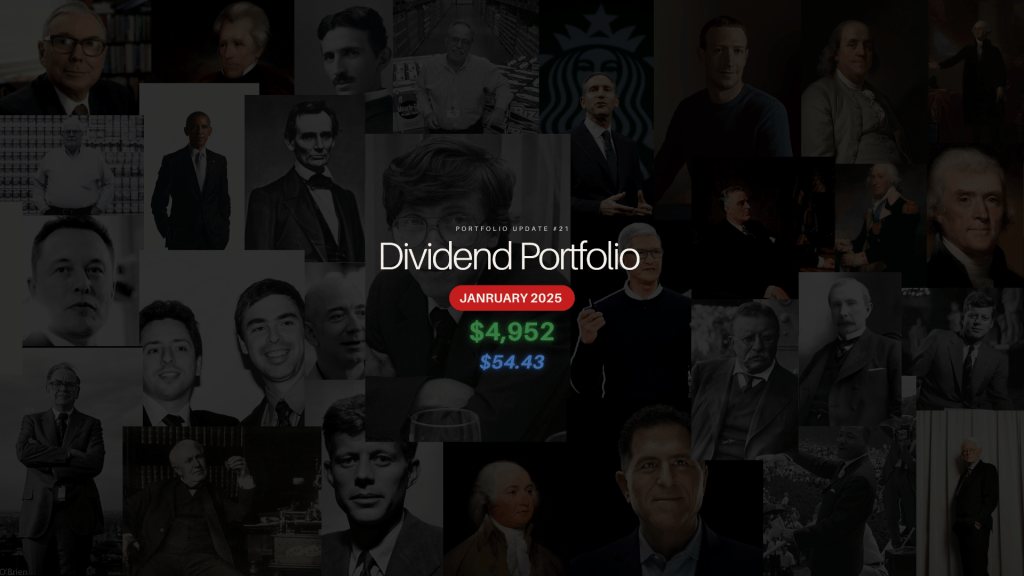

1. The Scoreboard

We closed out 2025 with the portfolio sitting at roughly $4,952. As of this update, thanks to recent contributions and a market rally, we have crossed a significant milestone.

- Total Value: $4,952

- Holdings: 21 Companies

- Forward Annual Dividends: ~$54.43

- Portfolio Yield: ~1.1% (on invested capital)

- Recent Performance: ~+9.6% gain since recent lows

The Takeaway: The portfolio is in its “toddler era”—growing fast, but not yet paying the rent. The ~10% gain on invested capital confirms that the “quality first” approach is working, even if the dividend income is still modest.

2. Composition: A “Barbell” Strategy

The portfolio is currently structured like a barbell, balancing two distinct engines to manage risk and return.

The Growth Engines (Offense)

A huge portion of our value sits in the titans of the modern economy: Microsoft, Apple, Alphabet (Google), Meta, Visa, and Mastercard. These companies pay tiny dividends (or none at all), but they provide the muscle. As noted in recent market data, the “Magnificent Seven” drive a massive share of the S&P 500’s returns.1 By owning them, we capture the capital appreciation that lifts the portfolio’s total value.

The Income Defenders (Defense)

Counterbalancing the tech giants are our “boring” dividend payers. This includes:

- Industrials/Services: ADP, Waste Management, Cintas.

- Healthcare: UnitedHealth (UNH), Becton Dickinson.

- Consumer/Niche: Starbucks, Costco, and regional banks (HFBL, FSBW).

This mix aligns with Fidelity’s research, which suggests that mixing growth-oriented tech with reliable dividend payers helps hedge against volatility. The boring stocks provide the ballast when the tech stocks stumble.

3. The Income Truth: Quality vs. Concentration

Let’s be honest about the numbers. A 1.1% yield generating $54/year is low compared to a high-yield savings account. This is intentional—we are prioritizing dividend growth over immediate yield.

However, a deep dive into the data reveals a specific risk: Income Concentration.

Currently, our dividend stream is heavily reliant on just a few names:

- Home Federal Bancorp (HFBL): ~$13.27/yr (~24% of total income)

- Starbucks: ~$5.23/yr

- Dell: ~$4.84/yr

- Becton Dickinson: ~$3.51/yr

While I love HFBL (it has been a great performer), having one small bank provide a quarter of the portfolio’s income is a vulnerability. The goal for 2026 is not necessarily to sell HFBL, but to aggressively grow the income from the other blue-chips (like ADP, UNH, and Visa) to balance the scales.

4. Performance: Winners & Opportunities

The overall portfolio is up, but the divergence between individual holdings is stark. This is exactly why we diversify.

- The Big Winners: Alphabet has been a monster, up roughly 71% from my cost basis. HFBL (+33%) and Hamilton Beach (+29%) are also doing heavy lifting.

- The Laggards: ADP (-7%), Costco (-5%), and Meta (-4%) are currently trailing.

Psychologically, it is tempting to view the red positions as “mistakes.” But in a dividend growth strategy, these are opportunities. ADP is a “Dividend King” with 51+ years of raises.2 If the price drops while the business remains strong, our reinvested dividends buy more shares at a discount, accelerating future growth.

Conclusion

The strategy remains simple: Buy wonderful businesses, reinvest the dividends, and wait.

In this tax-sheltered Roth IRA, every dividend is reinvested tax-free. We are “feeding the orchard.” The trees are still young, and the fruit (income) is small right now, but the roots are deep and the growth is real.

Next Steps for Jan/Feb:

- Stay patient.

Disclaimer: This post documents my personal investing journey. I am not a financial advisor. Always do your own due diligence.