Feb 2026

Thermo Fisher Scientific Inc.

Executive Summary

Thermo Fisher Scientific Inc. (NYSE: TMO) is the world’s leading provider of life science tools, technologies, and services, with a mission “to enable our customers to make the world healthier, cleaner and safer” . Formed via a landmark merger in 2006, Thermo Fisher has evolved into a global life sciences powerhouse with $42.9 billion in annual revenue (2024) , operations in dozens of countries, and a product portfolio that touches virtually every aspect of scientific research and healthcare. This deep dive evaluates Thermo Fisher as a long-term dividend compounder – a prospective “Dividend Centurion” – by examining its origin story, business model, competitive moat, financial performance, dividend strategy, risks, valuation, capital allocation, and peers. We then explore future scenarios for Thermo Fisher over the next 10–25 years to assess whether it can sustain durable dividend growth and join the ranks of elite dividend growth companies.

Key Takeaways: Thermo Fisher’s journey from a collection of niche lab supply businesses to the undisputed leader in life science tools and services underscores a rare combination of strategic vision and execution. The company enjoys a wide economic moat driven by unmatched scale, a one-stop-shop portfolio of products and services, high switching costs for customers, and a large base of recurring revenues . Financially, Thermo Fisher has delivered consistent growth (boosted by opportunistic acquisitions and pandemic-related demand in recent years), healthy profitability (gross margins ~45% and operating margins 25% ), robust free cash flow ($6.6 billion in 2024 ), and double-digit returns on invested capital (ROIC) historically . Although its dividend yield is modest (currently about 0.3% ), the company has rapidly grown its payout (15% CAGR over the past 5 years ) while maintaining a low payout ratio (<10% of earnings ). This reflects a deliberate capital allocation strategy that prioritizes reinvestment and acquisitions for growth, resilient dividend increases, and opportunistic share buybacks – a strategy that has rewarded shareholders with outsized total returns.

Looking ahead, Thermo Fisher’s entrenched position in the life sciences ecosystem, broad exposure to secular growth drivers (biopharma R&D, healthcare, advanced diagnostics, etc.), and proven ability to adapt (e.g. rapidly scaling COVID-19 testing supplies in 2020–21 ) suggest it is well-positioned to compound value for decades. In the following sections, we will dive deeper into how Thermo Fisher built its empire, how its business works, what competitive advantages protect its profits, how its financial and dividend track records stack up, what risks it faces, how it’s valued, how management deploys capital, how it compares to key peers like Danaher and Agilent, and what Thermo Fisher might look like as a dividend-paying powerhouse in 2040 and beyond.

The Evolution of Scientific Capital: A Definitive History of Thermo Fisher Scientific (NYSE: TMO)

Prologue: The Convergence of Matter and Energy

The history of Thermo Fisher Scientific is not merely a chronicle of corporate mergers and stock tickers; it is a proxy for the evolution of the American scientific industrial complex over the last century. From the soot-stained steel mills of Pittsburgh in 1902 to the genomic frontiers of the 21st century, the entity now known as Thermo Fisher Scientific has served as the silent infrastructure of discovery. It represents the successful fusion of two distinct, and at times contradictory, corporate philosophies: the “Fisher” lineage—a pragmatic, catalog-driven merchandising empire built on the tangible needs of the industrial chemist—and the “Thermo” lineage—an MIT-born, intellectual property-driven incubator founded on the abstract principles of thermodynamics.

The merger of these two entities in 2006 created a colossus that defied the typical “conglomerate discount,” building instead a “flywheel of serving science” that capitalizes on every stage of the research lifecycle. To understand the $170 billion titan that exists today, one must first deconstruct the parallel histories of its progenitors, exploring how a stockroom in Pittsburgh and a garage in Belmont, Massachusetts, evolved to control the supply chain of global science.

Chapter I: The Crucible of Industry — The Fisher Lineage (1902–1950)

The Pittsburgh Context and the Birth of the “Stockroom”

The genesis of the Fisher side of the ledger dates to the dawn of the 20th century in Pittsburgh, Pennsylvania, a city then serving as the crucible of American industrial power. In 1902, the steel industry was voracious, not just for iron ore and coal, but for the chemical verification of its products. As America transitioned from an agrarian society to an industrial superpower, quality control was moving from the artisan’s eye to the chemist’s bench. The burgeoning steel factories, coal mines, and manufacturing plants of western Pennsylvania required rigorous testing to ensure the structural integrity of the materials building the nation’s skyscrapers and railroads.1

However, the infrastructure to support this scientific booming was nonexistent. Chester Garfield Fisher, a twenty-year-old engineering graduate from the Western University of Pennsylvania (now the University of Pittsburgh), recognized a critical bottleneck in this industrial boom. The laboratories testing the steel and coal lacked a reliable, centralized commercial source for equipment and reagents. Laboratories were forced to source beakers from glassblowers, chemicals from apothecaries, and precision instruments from Europe, often with months of lead time.1

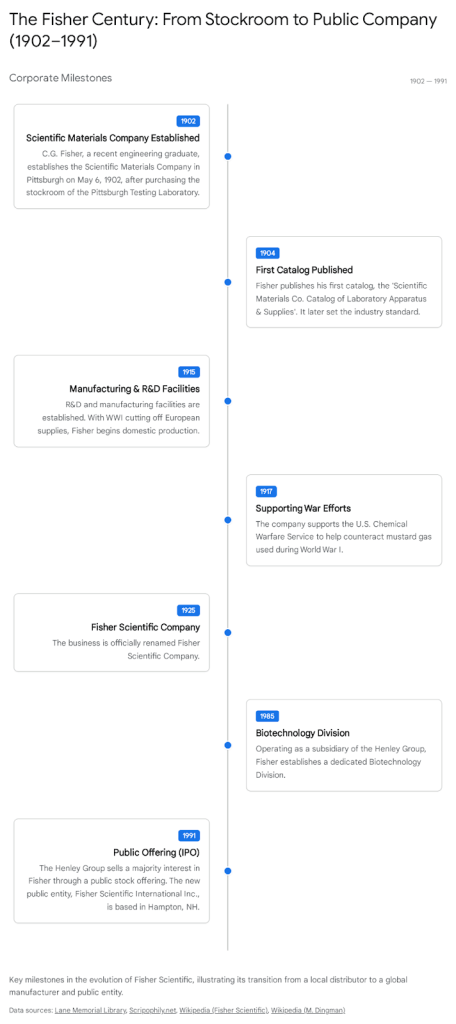

On May 6, 1902, C.G. Fisher purchased the stockroom of the Pittsburgh Testing Laboratory and established the “Scientific Materials Company”.1 This acquisition was the embryo of what would become Fisher Scientific. Fisher’s business model was not initially one of invention, but of aggregation and distribution—a “one-stop shop” mission that remains the core DNA of the Fisher channel today. By centralizing the supply chain, Fisher allowed industrial chemists to focus on analysis rather than procurement, effectively professionalizing the logistical side of American science.

The 1904 Catalog: The Bible of the Laboratory

In 1904, two years after founding the company, Fisher published the Scientific Materials Co. Catalog of Laboratory Apparatus & Supplies.1 This 400-page tome was more than a simple sales list; it was a radical act of standardization. In an era before standardized parts, where a “clamp” or a “stand” could vary wildly between manufacturers, Fisher’s catalog defined what a “standard” pipette, buret, or balance looked like for the American scientist.2

The catalog became the primary interface between the scientific world and the marketplace. Later renamed simply The Fisher Catalog, it set the industry standard and became a recognized scientific reference tool worldwide, eventually being published in eight different languages.4 The strategic brilliance of the catalog lay in its ability to lock customers into the Fisher ecosystem. By assigning unique catalog numbers to specific apparatus configurations, Fisher ensured that when a laboratory manager ordered a replacement part, they ordered it from Fisher. This effectively created a “platform” business model decades before the term was coined in Silicon Valley.

Wartime Innovation and Supply Chain Sovereignty

The outbreak of World War I presented the young company with its first existential crisis and its greatest opportunity. Prior to the war, the global scientific community was heavily reliant on Europe—specifically Germany—as the primary source of high-quality optical glass, reagents, and precision instruments. As the war severed these supply lines, American laboratories faced a critical shortage of essential tools.4

Forced to innovate to survive, Fisher established its own Research & Development (R&D) and manufacturing facilities in 1915.1 The company’s role shifted from a pure distributor to a manufacturer-distributor hybrid. This vertical integration allowed Fisher to control the quality and availability of its products, a strategic advantage that would prove crucial in the decades to come.

In 1917, the company’s logistical capabilities were tested on a national stage. Fisher supported the U.S. Chemical Warfare Service in its efforts to counteract the mustard gas attacks used by the German army. Chester Fisher coordinated a massive logistical operation to round up “seven railroad carloads” of supplies to produce a complete field research laboratory for the American Expeditionary Force in France.1 This feat demonstrated that Fisher was not just a vendor, but a strategic partner capable of mobilizing resources for national security.

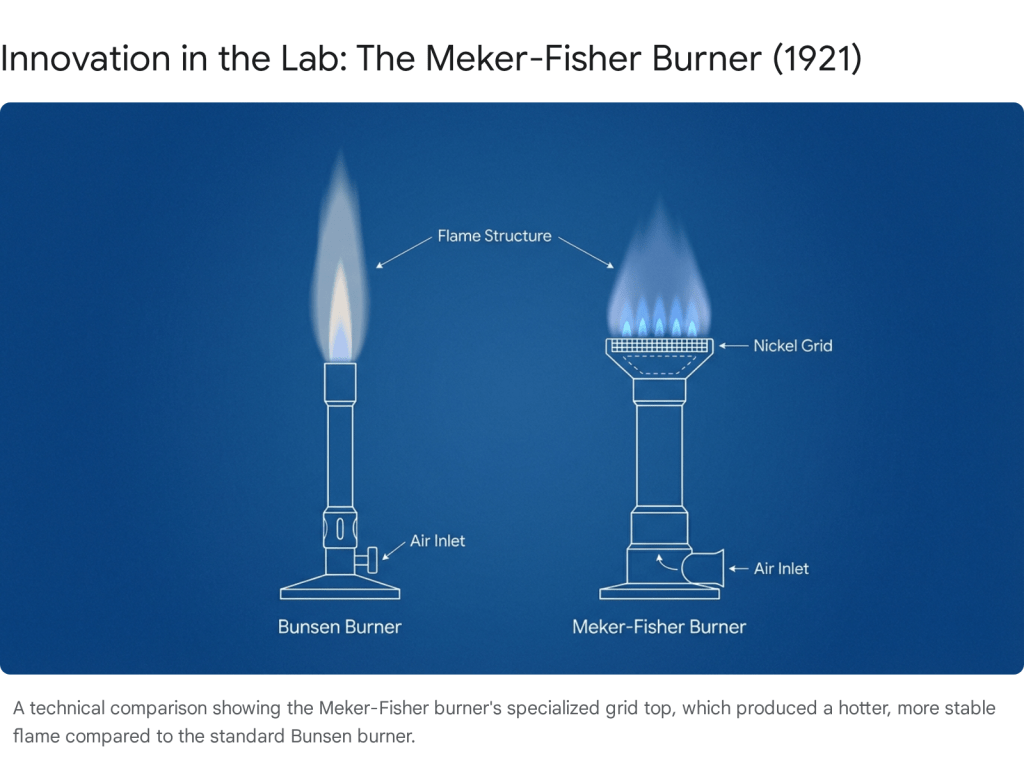

The Meker-Fisher Burner: Incremental Innovation

In 1921, the company introduced a product that exemplified its approach to innovation: the Meker-Fisher burner.1 Developed by Edwin Fisher, Chester’s brother, this device was a significant improvement over the standard Bunsen burner, which had been the laboratory standard since 1888. The traditional Bunsen burner often produced a flickering, uneven flame that was insufficient for the precise metallurgical analysis required by the steel industry.

Edwin Fisher’s design featured a deep nickel grid at the top of the burner tube and a larger air inlet. These modifications created a “short, intensely hot, homogeneous flame” that was far superior for high-temperature work.1 The Meker-Fisher burner was not a radical scientific breakthrough like the discovery of the electron; rather, it was a practical engineering fix that made the daily work of every chemist slightly more efficient. That philosophy—incremental, practical improvement delivered at scale—became the company’s ethos. In 1925, to distinguish itself from the many generic competitors springing up, the business was officially renamed the Fisher Scientific Company.1

The Alchemist Collection: A Cultural Legacy

A unique and often overlooked aspect of the Fisher history is its intersection with the world of fine art, which served a potent branding function. Chester Fisher was fascinated by the heritage of his customers—the chemists. He saw a direct lineage between the modern industrial chemist and the alchemists of the 17th century. To honor this connection, he began collecting Dutch and Flemish paintings depicting alchemists in their laboratories.5

Fisher acquired works by masters such as David Teniers the Younger and David Ryckaert III. His most famous acquisition was a painting titled The Alchemist, purchased in London in 1928.5 Fisher used reproductions of these paintings in his catalogs and marketing materials, effectively elevating the brand. By associating the often drab, industrial work of modern chemists with the mystical, noble pursuit of knowledge depicted in the paintings, Fisher provided his customers with a sense of professional dignity and historical continuity. This collection grew to be one of the largest of its kind in the world 7 and was eventually donated to the Chemical Heritage Foundation (now the Science History Institute).5 This cultural patronage reinforced the idea that Fisher Scientific was not merely a shop, but a custodian of the scientific tradition.

Chapter II: The Thermodynamics of Innovation — The Thermo Lineage (1956–1980)

George Hatsopoulos and the MIT Spin-out

While Fisher was perfecting the logistics of the stockroom in Pennsylvania, a different kind of scientific enterprise was taking shape in Massachusetts. In the mid-1950s, a Greek immigrant and MIT doctoral student named George Hatsopoulos was rewriting the rules of energy conversion in a garage in Belmont, Massachusetts.8

George Hatsopoulos was born in Athens in 1927 to a prominent family of professors and politicians. His early life was marked by the trauma and ingenuity of war; during the Nazi occupation of Athens in World War II, a teenage Hatsopoulos built radios from scavenged parts to provide the Greek resistance with access to BBC newscasts.9 This early experience with practical engineering under duress would characterize his later career. Following the war, he studied electrical engineering at Athens Polytechnic before moving to the United States to attend MIT, where he developed a deep fascination with thermodynamics—the science of energy and heat.10

In 1956, fresh with a PhD in mechanical engineering, Hatsopoulos founded Thermo Electron Corporation. The initial funding was a $50,000 loan provided by Peter Nomikos, a Harvard Business School graduate who believed in Hatsopoulos’s vision.10 The company’s original mission was high-minded and deeply technical: to develop direct energy conversion technologies, specifically thermionic energy conversion, which could turn heat directly into electricity without moving parts.10 This was a quintessential “deep tech” startup decades before the term existed, founded on the belief that fundamental laws of physics could be monetized.

Early Struggles and the Public Markets

Thermo Electron was not an overnight commercial success. Its core technology, while scientifically brilliant, was years ahead of its time and lacked immediate commercial applications. To survive, the company had to pivot and diversify. Thermo Electron went public in 1967 12, a move that provided the capital necessary to explore new applications for its thermodynamic expertise.

The company began to apply its knowledge of heat transfer and energy conversion to industrial problems. It developed systems for papermaking, metal processing, and environmental monitoring. Unlike Fisher, which grew by aggregating existing products, Thermo grew by inventing new ones. However, as the company expanded into diverse fields—from artificial hearts to bomb detectors—it faced a management challenge: how to maintain the entrepreneurial zeal of a startup within a growing conglomerate structure.

Chapter III: The Galaxy Strategy (1980–2000)

The Architecture of the Spin-out

In the 1980s, Hatsopoulos implemented a radical organizational strategy that would define Thermo Electron for three decades and become a case study in corporate finance. This strategy was known as the “spin-out.”

Unlike a traditional “spin-off,” where a parent company divests a business unit entirely to its shareholders to separate it from the core business, a spin-out involved Thermo Electron taking a specific technology division, incorporating it as a separate subsidiary, and selling a minority stake (typically around 10% to 20%) to the public via an Initial Public Offering (IPO), while retaining majority control.13

This structure created a “Thermo Galaxy,” with Thermo Electron as the sun and various subsidiaries orbiting it as publicly traded planets. The strategy was designed to solve three critical problems:

- Capital Raising: It allowed the company to raise cash for specific high-risk R&D projects (like the artificial heart) without diluting the parent company’s stock significantly. The subsidiary raised its own capital from investors who specifically wanted exposure to that technology.13

- Incentives: It solved the “big company” problem of diluted incentives. Managers of specific units (e.g., the environmental instrument division) were given stock options in their own subsidiary. This meant that their personal wealth was directly tied to the performance of their specific business, rather than being washed out by the average performance of a massive conglomerate.15 Hatsopoulos believed this replicated the hunger of a garage startup within a Fortune 500 company.

- Valuation: It attempted to eliminate the “conglomerate discount.” By having a market price for each piece of the empire, Hatsopoulos argued that the market would be forced to value the parent company as the sum of its parts, which was theoretically higher than the value of the whole.16

The Constellation of Subsidiaries

By the 1990s, the “Thermo Galaxy” had expanded into a bewildering array of public subsidiaries, creating a complex corporate ecosystem. Some of the key “planets” in this system included:

- Thermo Instrument Systems: Focused on analytical instruments for environmental and industrial monitoring.17

- Thermo Cardiosystems: Developing Left Ventricular Assist Devices (LVADs), essentially artificial hearts.10

- Thermo Ecotek: Dedicated to clean power generation and alternative energy projects.

- Thermo Fibertek: Focused on paper recycling and processing machinery.

- Thermo Trex: A high-tech subsidiary working on advanced physics, medical imaging (mammography), and defense applications like bomb detection.10

- Thermo BioAnalysis: A spin-out focused on the emerging field of bio-instrumentation.17

At its peak, the structure became fractal; subsidiaries would sometimes spin out their own subsidiaries (2nd and 3rd generation spin-outs), creating a web of cross-ownership and inter-company financing that was nearly impossible for an outsider to fully untangle.17

The Collapse of the Strategy: “One Thermo”

By the late 1990s, the spin-out strategy had become a victim of its own complexity. While it had successfully funded innovation for years, the structure was too convoluted for the average investor to understand. Wall Street began applying a heavy “conglomerate discount” because the transparency of the organization was low, and the administrative costs of maintaining dozens of public boards and filing separate SEC reports were high.16

Furthermore, the market environment had changed. The late 1990s were the era of the Dot-com bubble. Investors were chasing pure-play internet stocks and had little patience for complex industrial conglomerates with “sum of the parts” arguments. Thermo Electron’s stock price suffered as the market ignored the intrinsic value of its holdings.18

In 1998 and 1999, the Board, led by CEO Richard Syron (who succeeded Hatsopoulos), initiated the “One Thermo” restructuring strategy.19 This was a painful and expensive reversal of the previous twenty years. The plan involved:

- Privatizing the Spin-outs: Thermo Electron had to buy back the minority interests in its subsidiaries (e.g., ThermoSpectra, Thermo TerraTech) to consolidate them back under the parent company.18 This often involved paying a premium to the minority shareholders.

- Divesting Non-Core Assets: The company ruthlessly sold off businesses that did not fit the core mission of “instruments and life sciences.” Power generation, paper recycling, and other industrial businesses were divested.

- Rebranding: In 2000, the company initiated a master brand strategy. All remaining units were renamed with the prefix “Thermo” (e.g., Nicolet became Thermo Nicolet, Finnigan became Thermo Finnigan) to create a unified corporate identity.19

This restructuring transformed Thermo Electron from a chaotic holding company into a focused, integrated operating company. It laid the groundwork for the modern era by creating a streamlined entity that was ready for a transformative partnership.

Chapter IV: The Merchant of Science — Fisher’s Expansion (1950–2006)

The Henley Group Era and the 1991 IPO

While Thermo was experimenting with corporate structure, Fisher Scientific was undergoing its own transformation. For most of the 20th century, Fisher had remained a family-controlled entity. However, the corporate consolidation wave of the 1980s brought significant changes. The company was acquired and became a subsidiary of the Allied Corporation (later AlliedSignal). Subsequently, it was spun out into The Henley Group, a conglomerate run by Michael Dingman, a legendary corporate financier known as a “wheeler-dealer” operator who specialized in turning around undervalued industrial assets.3

Under Dingman’s stewardship, Fisher was groomed for the public markets. In 1991, The Henley Group sold a majority interest in Fisher Scientific through a public stock offering (IPO), listing it on the New York Stock Exchange under the ticker FSH.3 This marked the beginning of Fisher’s modern corporate era as an independent public company.

The Roll-Up Strategy

Following the IPO, Fisher embarked on an aggressive growth strategy under the leadership of CEO Paul Montrone (1991–2006) and CFO Paul Meister.21 The laboratory supply market in the 1990s was highly fragmented, consisting of hundreds of small, regional distributors. Montrone and Meister recognized that scale was the key to profitability in distribution.

They executed a “roll-up” strategy, completing over 60 acquisitions in a fifteen-year period.20 They bought regional competitors, specialized chemical suppliers, and niche equipment manufacturers. This consolidation spree transformed Fisher from a large American distributor into a global powerhouse with a massive logistical footprint. By the mid-2000s, Fisher Scientific was the dominant channel for scientific supplies, serving over 350,000 customers in 150 countries.3 They had perfected the art of the “one-stop shop,” but they lacked one critical component: high-end, proprietary technology. They were selling everyone else’s innovations, but owning very little of the intellectual property themselves.

Chapter V: The Fusion (2006)

The Strategic Rationale

In 2006, the trajectories of Thermo Electron and Fisher Scientific intersected. The logic for a combination was compelling, grounded in the concept of complementary strengths.

Thermo Electron was a powerhouse of high-end analytical instruments. They made the mass spectrometers, the chromatographs, and the elemental analyzers that were the “Ferraris” of the lab. However, these were one-time capital purchases. Once a lab bought a mass spectrometer, they might not buy another one for ten years. Thermo lacked a recurring revenue stream and a direct, high-frequency relationship with the customer.

Fisher Scientific, on the other hand, was the master of the channel. They sold the consumables—the pipette tips, the reagents, the glassware—that labs used every single day. They had the logistics network, the catalogs, and the deep customer relationships. However, they had low margins compared to high-tech instrument makers.

The proposed merger promised “synergy” in its truest form. Thermo’s high-margin instruments could be pushed through Fisher’s deep distribution channels. Conversely, Fisher’s consumables could be bundled with Thermo’s instruments, creating a sticky ecosystem. If a lab bought a Thermo instrument, the goal was to ensure they ran Fisher reagents through it for its entire lifecycle.

The Merger of Equals

On May 8, 2006, the two companies announced a “merger of equals”.22 The deal was structured as a tax-free, stock-for-stock exchange. Fisher shareholders received 2.00 shares of Thermo Electron common stock for each share of Fisher stock they owned.11 This valuation reflected the massive scale Fisher had achieved through its roll-up strategy.

The combined entity was projected to have more than $9 billion in revenues and $1 billion in cash flow in its first year.22 The deal closed on November 9, 2006, creating Thermo Fisher Scientific Inc. (NYSE: TMO). The ticker symbol TMO was retained, honoring the Thermo lineage, but the Fisher name took equal billing in the corporate identity, acknowledging the power of the Fisher brand in the marketplace.

Chapter VI: The Inorganic Engine (2006–2020)

Marc Casper and the Capital Allocation Machine

Post-merger, the leadership mantle eventually passed to Marc Casper, who became CEO in 2009. Under Casper, TMO became one of the most effective capital allocators in the S&P 500. The strategy was simple to describe but difficult to execute: use the strong, reliable cash flow from the base business (boosted by Fisher’s recurring consumables revenue) to acquire high-growth assets, plug them into the unrivaled Fisher distribution channel, and ruthlessly strip out costs through the “PPI Business System” (Practical Process Improvement).

The company embarked on a series of massive acquisitions that fundamentally altered its scope, moving it from an instrument and supply company to a dominant force in life sciences, genomics, and clinical services.

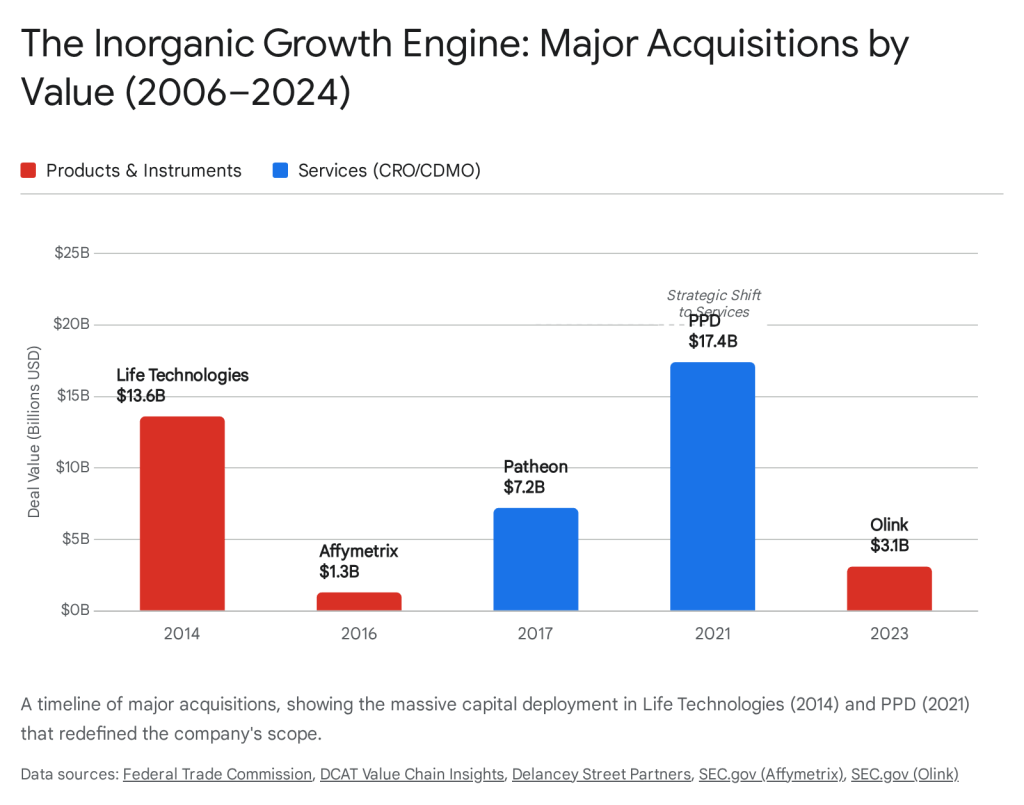

1. Life Technologies (2014) — $13.6 Billion

The acquisition of Life Technologies in 2014 was a transformative moment. Life Technologies itself was the product of a merger between Invitrogen and Applied Biosystems. By acquiring it for $13.6 billion, Thermo Fisher gained immediate dominance in the field of genomics.23

Life Technologies owned the Applied Biosystems brand, which was synonymous with DNA sequencing and PCR (Polymerase Chain Reaction) machines. It also owned Invitrogen, a leader in reagents and cellular analysis. This deal positioned TMO at the very center of the genomic revolution, providing the tools for the next generation of personalized medicine. The deal was so significant that the Federal Trade Commission (FTC) required TMO to divest its gene modulation and cell culture media businesses (selling them to GE Healthcare) to avoid creating a monopoly.23

2. FEI Company (2016) — $4.2 Billion

In 2016, TMO acquired FEI Company for approximately $4.2 billion.25 FEI was the global leader in electron microscopy. This was a strategic bet on the field of structural biology.

FEI’s Cryo-electron microscopy (Cryo-EM) technology allowed scientists to visualize protein structures at near-atomic resolution without crystallization. This technology was becoming essential for drug discovery, allowing pharmaceutical companies to map the structures of viruses and drug targets with unprecedented clarity. By acquiring FEI, TMO essentially bought a monopoly on the high-end microscope market, further entrenching itself in the drug discovery workflow.26

3. Patheon (2017) — $7.2 Billion

The 2017 acquisition of Patheon for $7.2 billion marked a significant strategic pivot into services.27 Patheon was a Contract Development and Manufacturing Organization (CDMO).

Historically, TMO sold the tools to make the drugs. With Patheon, TMO could now manufacture the drugs for the client. This vertical integration meant TMO could capture value across the entire lifecycle of a pharmaceutical product. A biotech startup could discover a drug using Thermo instruments, develop it using Fisher reagents, and then hire Thermo Fisher (via Patheon) to manufacture the pills or vials for clinical trials and commercial sale. This “end-to-end” proposition was unique in the industry.

Chapter VII: The Pandemic Pivot (2020–2022)

The “Arms Dealer” of the Pandemic

The COVID-19 pandemic was a defining moment for Thermo Fisher Scientific, testing the resilience and agility of the massive conglomerate. The company effectively became the “arms dealer” for the global pandemic response, supplying the essential tools required to fight the virus on multiple fronts.

When the virus genome was sequenced, Thermo Fisher mobilized its Life Technologies division to produce the TaqPath COVID-19 Combo Kit. This PCR-based test became the gold standard for detection globally.29 The company ramped up production of PCR machines, reagents, and plastics (pipette tips became as valuable as gold) to meet insatiable demand.

Simultaneously, its Patheon manufacturing division secured contracts to manufacture vaccines for major pharmaceutical players like Moderna and Pfizer.30 Thermo Fisher was thus profiting from both the diagnosis of the disease and the manufacturing of the cure.

The Financial Windfall and the PPD Acquisition

The financial impact was staggering. In the fourth quarter of 2020 alone, the company generated $3.2 billion in COVID-19 response revenue.29 This massive influx of cash provided the company with a war chest that it immediately sought to deploy.

Rather than issuing a special dividend or purely buying back stock, TMO stuck to its long-term strategy of M&A. In 2021, it announced its largest acquisition to date: the purchase of PPD, Inc. for $17.4 billion.31

PPD was a leading Contract Research Organization (CRO), a company that manages clinical trials for pharmaceutical companies. With this acquisition, TMO closed the final gap in its service offering. The “flywheel” was now complete:

- Discover: Using Thermo instruments and Life Tech genomics.

- Develop: Using Fisher supplies and reagents.

- Test: Managing clinical trials via PPD.

- Manufacture: Producing the commercial drug via Patheon.

This acquisition cemented Thermo Fisher’s position as the indispensable partner to the biopharma industry.

Chapter VIII: The New Frontier (2023–Present)

Navigating the “Covid Cliff”

As the pandemic subsided in 2022 and 2023, TMO faced what investors called the “Covid Cliff”—the sharp decline in testing revenue. However, the company successfully navigated this transition by focusing on its “base business” (non-COVID revenue). While testing revenue evaporated, the core business grew at double-digit rates, proving that the relationships formed during the pandemic were sticky and that the capital deployed into PPD was generating new growth engines.33

Olink and the Proteomics Push

In late 2023, Thermo Fisher announced the acquisition of Olink Holding AB for approximately $3.1 billion, a deal that closed in July 2024.35 Olink specializes in proteomics—the study of proteins. While genomics (DNA) tells you what could happen, proteomics tells you what is happening in the body. It is widely considered the next frontier in precision medicine.

Olink’s technology, specifically its Proximity Extension Assay (PEA), allows for the high-throughput analysis of protein biomarkers. This acquisition complements the massive installed base of Thermo mass spectrometers and PCR machines, positioning the company to lead the next wave of biological discovery.

Financial Performance: A Legacy of Compounding

The financial history of Thermo Fisher Scientific is a testament to the power of compounding. The company’s stock has been a perennial outperformer.

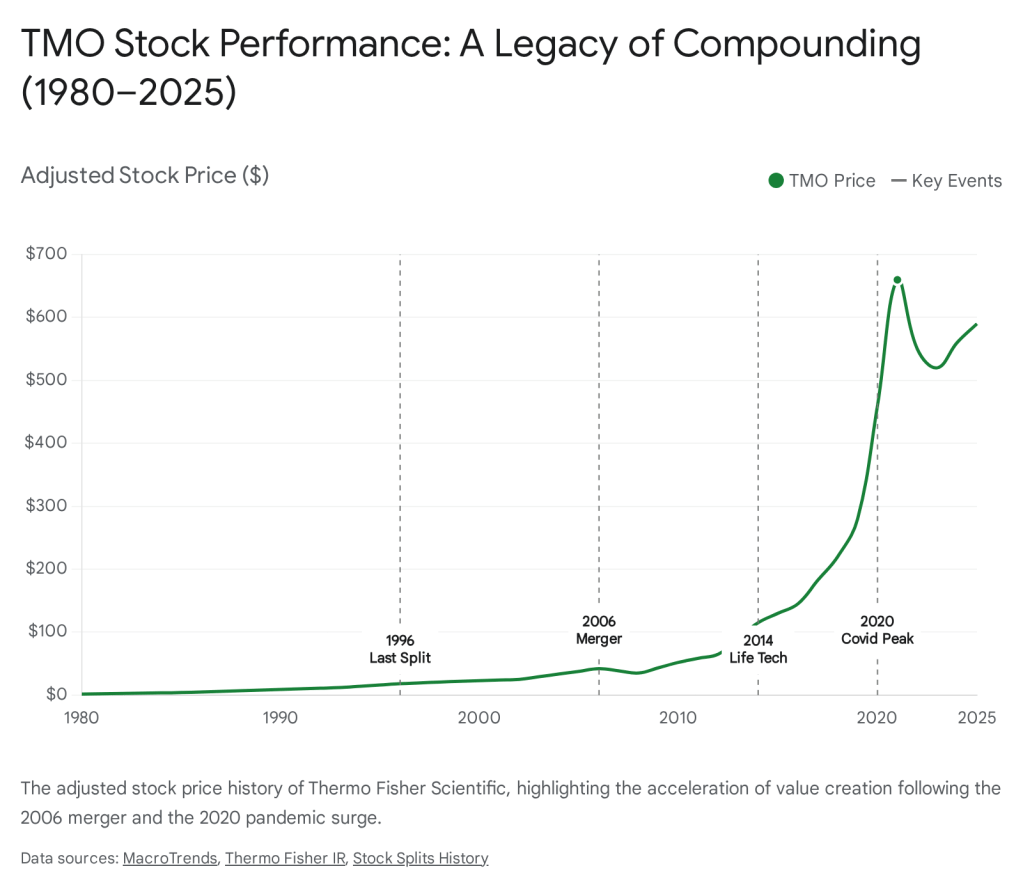

Stock Splits: Before the 2006 merger, the legacy Thermo Electron company frequently split its stock to maintain liquidity, with 3-for-2 splits occurring in 1983, 1985, 1986, 1993, 1995, and 1996.37 Notably, there have been no stock splits since 1996. The modern management team appears to view a high share price (trading often above $500 in recent years) as a badge of quality and institutional stability, eschewing the retail-friendly tactics of frequent splits.

Dividends: The company initiated a dividend program which has grown consistently. As of the 2024/2025 period, the company has increased its dividend for 9 consecutive years.39 However, the yield remains low (typically less than 0.5%), as the company continues to prioritize capital appreciation and aggressive M&A over income generation. The retained earnings are viewed as fuel for the next acquisition, a strategy that shareholders have largely endorsed given the company’s track record of successful integration.

Recent Financials: For the full year 2025, Thermo Fisher reported revenue of $44.56 billion, a 4% increase from the previous year, with adjusted earnings per share (EPS) of $22.87.41 These figures underscore the massive scale the company has achieved—from a $50,000 loan in a garage to a $45 billion annual revenue engine.

Epilogue: The Silent Infrastructure

The history of Thermo Fisher Scientific is a study in the evolution of scientific capital. It began with two distinct threads: Chester Fisher’s recognition that science needs a supply chain, and George Hatsopoulos’s belief that science can be a business.

For the first century, these threads ran parallel. Fisher built the catalog; Thermo built the instruments. Their convergence in 2006 created a unique entity that defies the traditional boundaries of the sector. It is neither just a manufacturer nor just a distributor. It is the infrastructure of science itself.

Today, with a market capitalization often exceeding $200 billion and a presence in almost every laboratory on Earth, TMO stands as a testament to the power of the “pick-and-shovel” strategy. While pharmaceutical companies bet billions on the binary outcome of a single drug trial, Thermo Fisher bets on the process of discovery itself. It is a wager that, for 120 years, has rarely failed to pay off.

Appendix A: Key Biographical Figures

| Figure | Role | Key Contribution |

| Chester Garfield Fisher | Founder, Fisher Scientific | Established the “stockroom” model; created the 1904 catalog; pioneered the standardizing of lab equipment; art collector who defined the brand’s cultural legacy. |

| George Hatsopoulos | Founder, Thermo Electron | MIT PhD and Greek resistance fighter; pioneered the “spin-out” strategy; focused company on thermodynamics and instrumentation; defined the engineering culture. |

| Paul Montrone | CEO, Fisher Scientific | Led Fisher’s aggressive consolidation (60+ acquisitions) in the 1990s and architected the 2006 merger of equals. |

| Marc Casper | CEO, Thermo Fisher (2009–) | Architect of the modern “M&A Machine” (Life Tech, FEI, PPD) and the Covid-19 pivot; defined the current “Customer Channel” strategy. |

Appendix B: The Alchemist in Art

The Fisher collection of alchemical art serves as a fascinating window into the company’s corporate soul. While modern science prides itself on rationality, Chester Fisher understood that the impulse to discover—the drive to turn base matter into gold, or sickness into health—remains unchanged. By surrounding his employees and customers with images of Teniers’ alchemists, he reminded them that they were part of a lineage that stretched back centuries. The specific painting The Alchemist by David Teniers the Younger, acquired in 1928, depicts an alchemist working bellows at a furnace—a direct visual parallel to the Meker-Fisher burners that Fisher was manufacturing in Pittsburgh. This visual continuity helped elevate the brand from a commodity supplier to a partner in the great human endeavor of discovery.

The Evolution of Scientific Capital: A Definitive History of Thermo Fisher Scientific (NYSE: TMO)

Prologue: The Convergence of Matter and Energy

The history of Thermo Fisher Scientific is not merely a chronicle of corporate mergers and stock tickers; it is a proxy for the evolution of the American scientific industrial complex over the last century. From the soot-stained steel mills of Pittsburgh in 1902 to the genomic frontiers of the 21st century, the entity now known as Thermo Fisher Scientific has served as the silent infrastructure of discovery. It represents the successful fusion of two distinct, and at times contradictory, corporate philosophies: the “Fisher” lineage—a pragmatic, catalog-driven merchandising empire built on the tangible needs of the industrial chemist—and the “Thermo” lineage—an MIT-born, intellectual property-driven incubator founded on the abstract principles of thermodynamics.

The merger of these two entities in 2006 created a colossus that defied the typical “conglomerate discount,” building instead a “flywheel of serving science” that capitalizes on every stage of the research lifecycle. To understand the $170 billion titan that exists today, one must first deconstruct the parallel histories of its progenitors, exploring how a stockroom in Pittsburgh and a garage in Belmont, Massachusetts, evolved to control the supply chain of global science.

Chapter I: The Crucible of Industry — The Fisher Lineage (1902–1950)

The Pittsburgh Context and the Birth of the “Stockroom”

The genesis of the Fisher side of the ledger dates to the dawn of the 20th century in Pittsburgh, Pennsylvania, a city then serving as the crucible of American industrial power. In 1902, the steel industry was voracious, not just for iron ore and coal, but for the chemical verification of its products. As America transitioned from an agrarian society to an industrial superpower, quality control was moving from the artisan’s eye to the chemist’s bench. The burgeoning steel factories, coal mines, and manufacturing plants of western Pennsylvania required rigorous testing to ensure the structural integrity of the materials building the nation’s skyscrapers and railroads.

However, the infrastructure to support this scientific booming was nonexistent. Chester Garfield Fisher, a twenty-year-old engineering graduate from the Western University of Pennsylvania (now the University of Pittsburgh), recognized a critical bottleneck in this industrial boom. The laboratories testing the steel and coal lacked a reliable, centralized commercial source for equipment and reagents. Laboratories were forced to source beakers from glassblowers, chemicals from apothecaries, and precision instruments from Europe, often with months of lead time.

On May 6, 1902, C.G. Fisher purchased the stockroom of the Pittsburgh Testing Laboratory and established the “Scientific Materials Company”. This acquisition was the embryo of what would become Fisher Scientific. Fisher’s business model was not initially one of invention, but of aggregation and distribution—a “one-stop shop” mission that remains the core DNA of the Fisher channel today. By centralizing the supply chain, Fisher allowed industrial chemists to focus on analysis rather than procurement, effectively professionalizing the logistical side of American science.

The 1904 Catalog: The Bible of the Laboratory

In 1904, two years after founding the company, Fisher published the Scientific Materials Co. Catalog of Laboratory Apparatus & Supplies. This 400-page tome was more than a simple sales list; it was a radical act of standardization. In an era before standardized parts, where a “clamp” or a “stand” could vary wildly between manufacturers, Fisher’s catalog defined what a “standard” pipette, buret, or balance looked like for the American scientist.

The catalog became the primary interface between the scientific world and the marketplace. Later renamed simply The Fisher Catalog, it set the industry standard and became a recognized scientific reference tool worldwide, eventually being published in eight different languages. The strategic brilliance of the catalog lay in its ability to lock customers into the Fisher ecosystem. By assigning unique catalog numbers to specific apparatus configurations, Fisher ensured that when a laboratory manager ordered a replacement part, they ordered it from Fisher. This effectively created a “platform” business model decades before the term was coined in Silicon Valley.

Wartime Innovation and Supply Chain Sovereignty

The outbreak of World War I presented the young company with its first existential crisis and its greatest opportunity. Prior to the war, the global scientific community was heavily reliant on Europe—specifically Germany—as the primary source of high-quality optical glass, reagents, and precision instruments. As the war severed these supply lines, American laboratories faced a critical shortage of essential tools.

Forced to innovate to survive, Fisher established its own Research & Development (R&D) and manufacturing facilities in 1915. The company’s role shifted from a pure distributor to a manufacturer-distributor hybrid. This vertical integration allowed Fisher to control the quality and availability of its products, a strategic advantage that would prove crucial in the decades to come.

In 1917, the company’s logistical capabilities were tested on a national stage. Fisher supported the U.S. Chemical Warfare Service in its efforts to counteract the mustard gas attacks used by the German army. Chester Fisher coordinated a massive logistical operation to round up “seven railroad carloads” of supplies to produce a complete field research laboratory for the American Expeditionary Force in France. This feat demonstrated that Fisher was not just a vendor, but a strategic partner capable of mobilizing resources for national security.

The Meker-Fisher Burner: Incremental Innovation

In 1921, the company introduced a product that exemplified its approach to innovation: the Meker-Fisher burner.Developed by Edwin Fisher, Chester’s brother, this device was a significant improvement over the standard Bunsen burner, which had been the laboratory standard since 1888. The traditional Bunsen burner often produced a flickering, uneven flame that was insufficient for the precise metallurgical analysis required by the steel industry.

Edwin Fisher’s design featured a deep nickel grid at the top of the burner tube and a larger air inlet. These modifications created a “short, intensely hot, homogeneous flame” that was far superior for high-temperature work. The Meker-Fisher burner was not a radical scientific breakthrough like the discovery of the electron; rather, it was a practical engineering fix that made the daily work of every chemist slightly more efficient. That philosophy—incremental, practical improvement delivered at scale—became the company’s ethos. In 1925, to distinguish itself from the many generic competitors springing up, the business was officially renamed the Fisher Scientific Company.

The Alchemist Collection: A Cultural Legacy

A unique and often overlooked aspect of the Fisher history is its intersection with the world of fine art, which served a potent branding function. Chester Fisher was fascinated by the heritage of his customers—the chemists. He saw a direct lineage between the modern industrial chemist and the alchemists of the 17th century. To honor this connection, he began collecting Dutch and Flemish paintings depicting alchemists in their laboratories.

Fisher acquired works by masters such as David Teniers the Younger and David Ryckaert III. His most famous acquisition was a painting titled The Alchemist, purchased in London in 1928. Fisher used reproductions of these paintings in his catalogs and marketing materials, effectively elevating the brand. By associating the often drab, industrial work of modern chemists with the mystical, noble pursuit of knowledge depicted in the paintings, Fisher provided his customers with a sense of professional dignity and historical continuity. This collection grew to be one of the largest of its kind in the world and was eventually donated to the Chemical Heritage Foundation (now the Science History Institute). This cultural patronage reinforced the idea that Fisher Scientific was not merely a shop, but a custodian of the scientific tradition.

Chapter II: The Thermodynamics of Innovation — The Thermo Lineage (1956–1980)

George Hatsopoulos and the MIT Spin-out

While Fisher was perfecting the logistics of the stockroom in Pennsylvania, a different kind of scientific enterprise was taking shape in Massachusetts. In the mid-1950s, a Greek immigrant and MIT doctoral student named George Hatsopoulos was rewriting the rules of energy conversion in a garage in Belmont, Massachusetts.

George Hatsopoulos was born in Athens in 1927 to a prominent family of professors and politicians. His early life was marked by the trauma and ingenuity of war; during the Nazi occupation of Athens in World War II, a teenage Hatsopoulos built radios from scavenged parts to provide the Greek resistance with access to BBC newscasts. This early experience with practical engineering under duress would characterize his later career. Following the war, he studied electrical engineering at Athens Polytechnic before moving to the United States to attend MIT, where he developed a deep fascination with thermodynamics—the science of energy and heat.

In 1956, fresh with a PhD in mechanical engineering, Hatsopoulos founded Thermo Electron Corporation. The initial funding was a $50,000 loan provided by Peter Nomikos, a Harvard Business School graduate who believed in Hatsopoulos’s vision. The company’s original mission was high-minded and deeply technical: to develop direct energy conversion technologies, specifically thermionic energy conversion, which could turn heat directly into electricity without moving parts. This was a quintessential “deep tech” startup decades before the term existed, founded on the belief that fundamental laws of physics could be monetized.

Early Struggles and the Public Markets

Thermo Electron was not an overnight commercial success. Its core technology, while scientifically brilliant, was years ahead of its time and lacked immediate commercial applications. To survive, the company had to pivot and diversify. Thermo Electron went public in 1967 , a move that provided the capital necessary to explore new applications for its thermodynamic expertise.

The company began to apply its knowledge of heat transfer and energy conversion to industrial problems. It developed systems for papermaking, metal processing, and environmental monitoring. Unlike Fisher, which grew by aggregating existing products, Thermo grew by inventing new ones. However, as the company expanded into diverse fields—from artificial hearts to bomb detectors—it faced a management challenge: how to maintain the entrepreneurial zeal of a startup within a growing conglomerate structure.

Chapter III: The Galaxy Strategy (1980–2000)

The Architecture of the Spin-out

In the 1980s, Hatsopoulos implemented a radical organizational strategy that would define Thermo Electron for three decades and become a case study in corporate finance. This strategy was known as the “spin-out.”

Unlike a traditional “spin-off,” where a parent company divests a business unit entirely to its shareholders to separate it from the core business, a spin-out involved Thermo Electron taking a specific technology division, incorporating it as a separate subsidiary, and selling a minority stake (typically around 10% to 20%) to the public via an Initial Public Offering (IPO), while retaining majority control.

This structure created a “Thermo Galaxy,” with Thermo Electron as the sun and various subsidiaries orbiting it as publicly traded planets. The strategy was designed to solve three critical problems:

- Capital Raising: It allowed the company to raise cash for specific high-risk R&D projects (like the artificial heart) without diluting the parent company’s stock significantly. The subsidiary raised its own capital from investors who specifically wanted exposure to that technology.

- Incentives: It solved the “big company” problem of diluted incentives. Managers of specific units (e.g., the environmental instrument division) were given stock options in their own subsidiary. This meant that their personal wealth was directly tied to the performance of their specific business, rather than being washed out by the average performance of a massive conglomerate. Hatsopoulos believed this replicated the hunger of a garage startup within a Fortune 500 company.

- Valuation: It attempted to eliminate the “conglomerate discount.” By having a market price for each piece of the empire, Hatsopoulos argued that the market would be forced to value the parent company as the sum of its parts, which was theoretically higher than the value of the whole.

The Constellation of Subsidiaries

By the 1990s, the “Thermo Galaxy” had expanded into a bewildering array of public subsidiaries, creating a complex corporate ecosystem. Some of the key “planets” in this system included:

- Thermo Instrument Systems: Focused on analytical instruments for environmental and industrial monitoring.

- Thermo Cardiosystems: Developing Left Ventricular Assist Devices (LVADs), essentially artificial hearts.

- Thermo Ecotek: Dedicated to clean power generation and alternative energy projects.

- Thermo Fibertek: Focused on paper recycling and processing machinery.

- Thermo Trex: A high-tech subsidiary working on advanced physics, medical imaging (mammography), and defense applications like bomb detection.

- Thermo BioAnalysis: A spin-out focused on the emerging field of bio-instrumentation.

At its peak, the structure became fractal; subsidiaries would sometimes spin out their own subsidiaries (2nd and 3rd generation spin-outs), creating a web of cross-ownership and inter-company financing that was nearly impossible for an outsider to fully untangle.

The Collapse of the Strategy: “One Thermo”

By the late 1990s, the spin-out strategy had become a victim of its own complexity. While it had successfully funded innovation for years, the structure was too convoluted for the average investor to understand. Wall Street began applying a heavy “conglomerate discount” because the transparency of the organization was low, and the administrative costs of maintaining dozens of public boards and filing separate SEC reports were high.

Furthermore, the market environment had changed. The late 1990s were the era of the Dot-com bubble. Investors were chasing pure-play internet stocks and had little patience for complex industrial conglomerates with “sum of the parts” arguments. Thermo Electron’s stock price suffered as the market ignored the intrinsic value of its holdings.

In 1998 and 1999, the Board, led by CEO Richard Syron (who succeeded Hatsopoulos), initiated the “One Thermo” restructuring strategy. This was a painful and expensive reversal of the previous twenty years. The plan involved:

- Privatizing the Spin-outs: Thermo Electron had to buy back the minority interests in its subsidiaries (e.g., ThermoSpectra, Thermo TerraTech) to consolidate them back under the parent company. This often involved paying a premium to the minority shareholders.

- Divesting Non-Core Assets: The company ruthlessly sold off businesses that did not fit the core mission of “instruments and life sciences.” Power generation, paper recycling, and other industrial businesses were divested.

- Rebranding: In 2000, the company initiated a master brand strategy. All remaining units were renamed with the prefix “Thermo” (e.g., Nicolet became Thermo Nicolet, Finnigan became Thermo Finnigan) to create a unified corporate identity.

This restructuring transformed Thermo Electron from a chaotic holding company into a focused, integrated operating company. It laid the groundwork for the modern era by creating a streamlined entity that was ready for a transformative partnership.

Chapter IV: The Merchant of Science — Fisher’s Expansion (1950–2006)

The Henley Group Era and the 1991 IPO

While Thermo was experimenting with corporate structure, Fisher Scientific was undergoing its own transformation. For most of the 20th century, Fisher had remained a family-controlled entity. However, the corporate consolidation wave of the 1980s brought significant changes. The company was acquired and became a subsidiary of the Allied Corporation (later AlliedSignal). Subsequently, it was spun out into The Henley Group, a conglomerate run by Michael Dingman, a legendary corporate financier known as a “wheeler-dealer” operator who specialized in turning around undervalued industrial assets.

Under Dingman’s stewardship, Fisher was groomed for the public markets. In 1991, The Henley Group sold a majority interest in Fisher Scientific through a public stock offering (IPO), listing it on the New York Stock Exchange under the ticker FSH. This marked the beginning of Fisher’s modern corporate era as an independent public company.

The Roll-Up Strategy

Following the IPO, Fisher embarked on an aggressive growth strategy under the leadership of CEO Paul Montrone (1991–2006) and CFO Paul Meister. The laboratory supply market in the 1990s was highly fragmented, consisting of hundreds of small, regional distributors. Montrone and Meister recognized that scale was the key to profitability in distribution.

They executed a “roll-up” strategy, completing over 60 acquisitions in a fifteen-year period. They bought regional competitors, specialized chemical suppliers, and niche equipment manufacturers. This consolidation spree transformed Fisher from a large American distributor into a global powerhouse with a massive logistical footprint. By the mid-2000s, Fisher Scientific was the dominant channel for scientific supplies, serving over 350,000 customers in 150 countries. They had perfected the art of the “one-stop shop,” but they lacked one critical component: high-end, proprietary technology. They were selling everyone else’s innovations, but owning very little of the intellectual property themselves.

Chapter V: The Fusion (2006)

The Strategic Rationale

In 2006, the trajectories of Thermo Electron and Fisher Scientific intersected. The logic for a combination was compelling, grounded in the concept of complementary strengths.

Thermo Electron was a powerhouse of high-end analytical instruments. They made the mass spectrometers, the chromatographs, and the elemental analyzers that were the “Ferraris” of the lab. However, these were one-time capital purchases. Once a lab bought a mass spectrometer, they might not buy another one for ten years. Thermo lacked a recurring revenue stream and a direct, high-frequency relationship with the customer.

Fisher Scientific, on the other hand, was the master of the channel. They sold the consumables—the pipette tips, the reagents, the glassware—that labs used every single day. They had the logistics network, the catalogs, and the deep customer relationships. However, they had low margins compared to high-tech instrument makers.

The proposed merger promised “synergy” in its truest form. Thermo’s high-margin instruments could be pushed through Fisher’s deep distribution channels. Conversely, Fisher’s consumables could be bundled with Thermo’s instruments, creating a sticky ecosystem. If a lab bought a Thermo instrument, the goal was to ensure they ran Fisher reagents through it for its entire lifecycle.

The Merger of Equals

On May 8, 2006, the two companies announced a “merger of equals”. The deal was structured as a tax-free, stock-for-stock exchange. Fisher shareholders received 2.00 shares of Thermo Electron common stock for each share of Fisher stock they owned. This valuation reflected the massive scale Fisher had achieved through its roll-up strategy.

The combined entity was projected to have more than $9 billion in revenues and $1 billion in cash flow in its first year.The deal closed on November 9, 2006, creating Thermo Fisher Scientific Inc. (NYSE: TMO). The ticker symbol TMO was retained, honoring the Thermo lineage, but the Fisher name took equal billing in the corporate identity, acknowledging the power of the Fisher brand in the marketplace.

Chapter VI: The Inorganic Engine (2006–2020)

Marc Casper and the Capital Allocation Machine

Post-merger, the leadership mantle eventually passed to Marc Casper, who became CEO in 2009. Under Casper, TMO became one of the most effective capital allocators in the S&P 500. The strategy was simple to describe but difficult to execute: use the strong, reliable cash flow from the base business (boosted by Fisher’s recurring consumables revenue) to acquire high-growth assets, plug them into the unrivaled Fisher distribution channel, and ruthlessly strip out costs through the “PPI Business System” (Practical Process Improvement).

The company embarked on a series of massive acquisitions that fundamentally altered its scope, moving it from an instrument and supply company to a dominant force in life sciences, genomics, and clinical services.

1. Life Technologies (2014) — $13.6 Billion

The acquisition of Life Technologies in 2014 was a transformative moment. Life Technologies itself was the product of a merger between Invitrogen and Applied Biosystems. By acquiring it for $13.6 billion, Thermo Fisher gained immediate dominance in the field of genomics.

Life Technologies owned the Applied Biosystems brand, which was synonymous with DNA sequencing and PCR (Polymerase Chain Reaction) machines. It also owned Invitrogen, a leader in reagents and cellular analysis. This deal positioned TMO at the very center of the genomic revolution, providing the tools for the next generation of personalized medicine. The deal was so significant that the Federal Trade Commission (FTC) required TMO to divest its gene modulation and cell culture media businesses (selling them to GE Healthcare) to avoid creating a monopoly.

2. FEI Company (2016) — $4.2 Billion

In 2016, TMO acquired FEI Company for approximately $4.2 billion. FEI was the global leader in electron microscopy. This was a strategic bet on the field of structural biology.

FEI’s Cryo-electron microscopy (Cryo-EM) technology allowed scientists to visualize protein structures at near-atomic resolution without crystallization. This technology was becoming essential for drug discovery, allowing pharmaceutical companies to map the structures of viruses and drug targets with unprecedented clarity. By acquiring FEI, TMO essentially bought a monopoly on the high-end microscope market, further entrenching itself in the drug discovery workflow.

3. Patheon (2017) — $7.2 Billion

The 2017 acquisition of Patheon for $7.2 billion marked a significant strategic pivot into services. Patheon was a Contract Development and Manufacturing Organization (CDMO).

Historically, TMO sold the tools to make the drugs. With Patheon, TMO could now manufacture the drugs for the client. This vertical integration meant TMO could capture value across the entire lifecycle of a pharmaceutical product. A biotech startup could discover a drug using Thermo instruments, develop it using Fisher reagents, and then hire Thermo Fisher (via Patheon) to manufacture the pills or vials for clinical trials and commercial sale. This “end-to-end” proposition was unique in the industry.

Chapter VII: The Pandemic Pivot (2020–2022)

The “Arms Dealer” of the Pandemic

The COVID-19 pandemic was a defining moment for Thermo Fisher Scientific, testing the resilience and agility of the massive conglomerate. The company effectively became the “arms dealer” for the global pandemic response, supplying the essential tools required to fight the virus on multiple fronts.

When the virus genome was sequenced, Thermo Fisher mobilized its Life Technologies division to produce the TaqPath COVID-19 Combo Kit. This PCR-based test became the gold standard for detection globally. The company ramped up production of PCR machines, reagents, and plastics (pipette tips became as valuable as gold) to meet insatiable demand.

Simultaneously, its Patheon manufacturing division secured contracts to manufacture vaccines for major pharmaceutical players like Moderna and Pfizer. Thermo Fisher was thus profiting from both the diagnosis of the disease and the manufacturing of the cure.

The Financial Windfall and the PPD Acquisition

The financial impact was staggering. In the fourth quarter of 2020 alone, the company generated $3.2 billion in COVID-19 response revenue. This massive influx of cash provided the company with a war chest that it immediately sought to deploy.

Rather than issuing a special dividend or purely buying back stock, TMO stuck to its long-term strategy of M&A. In 2021, it announced its largest acquisition to date: the purchase of PPD, Inc. for $17.4 billion.

PPD was a leading Contract Research Organization (CRO), a company that manages clinical trials for pharmaceutical companies. With this acquisition, TMO closed the final gap in its service offering. The “flywheel” was now complete:

- Discover: Using Thermo instruments and Life Tech genomics.

- Develop: Using Fisher supplies and reagents.

- Test: Managing clinical trials via PPD.

- Manufacture: Producing the commercial drug via Patheon.

This acquisition cemented Thermo Fisher’s position as the indispensable partner to the biopharma industry.

Chapter VIII: The New Frontier (2023–Present)

Navigating the “Covid Cliff”

As the pandemic subsided in 2022 and 2023, TMO faced what investors called the “Covid Cliff”—the sharp decline in testing revenue. However, the company successfully navigated this transition by focusing on its “base business” (non-COVID revenue). While testing revenue evaporated, the core business grew at double-digit rates, proving that the relationships formed during the pandemic were sticky and that the capital deployed into PPD was generating new growth engines.

Olink and the Proteomics Push

In late 2023, Thermo Fisher announced the acquisition of Olink Holding AB for approximately $3.1 billion, a deal that closed in July 2024. Olink specializes in proteomics—the study of proteins. While genomics (DNA) tells you what could happen, proteomics tells you what is happening in the body. It is widely considered the next frontier in precision medicine.

Olink’s technology, specifically its Proximity Extension Assay (PEA), allows for the high-throughput analysis of protein biomarkers. This acquisition complements the massive installed base of Thermo mass spectrometers and PCR machines, positioning the company to lead the next wave of biological discovery.

Financial Performance: A Legacy of Compounding

The financial history of Thermo Fisher Scientific is a testament to the power of compounding. The company’s stock has been a perennial outperformer.

Stock Splits: Before the 2006 merger, the legacy Thermo Electron company frequently split its stock to maintain liquidity, with 3-for-2 splits occurring in 1983, 1985, 1986, 1993, 1995, and 1996. Notably, there have been no stock splits since 1996. The modern management team appears to view a high share price (trading often above $500 in recent years) as a badge of quality and institutional stability, eschewing the retail-friendly tactics of frequent splits.

Dividends: The company initiated a dividend program which has grown consistently. As of the 2024/2025 period, the company has increased its dividend for 9 consecutive years. However, the yield remains low (typically less than 0.5%), as the company continues to prioritize capital appreciation and aggressive M&A over income generation. The retained earnings are viewed as fuel for the next acquisition, a strategy that shareholders have largely endorsed given the company’s track record of successful integration.

Recent Financials: For the full year 2025, Thermo Fisher reported revenue of $44.56 billion, a 4% increase from the previous year, with adjusted earnings per share (EPS) of $22.87. These figures underscore the massive scale the company has achieved—from a $50,000 loan in a garage to a $45 billion annual revenue engine.

Epilogue: The Silent Infrastructure

The history of Thermo Fisher Scientific is a study in the evolution of scientific capital. It began with two distinct threads: Chester Fisher’s recognition that science needs a supply chain, and George Hatsopoulos’s belief that science can be a business.

For the first century, these threads ran parallel. Fisher built the catalog; Thermo built the instruments. Their convergence in 2006 created a unique entity that defies the traditional boundaries of the sector. It is neither just a manufacturer nor just a distributor. It is the infrastructure of science itself.

Today, with a market capitalization often exceeding $200 billion and a presence in almost every laboratory on Earth, TMO stands as a testament to the power of the “pick-and-shovel” strategy. While pharmaceutical companies bet billions on the binary outcome of a single drug trial, Thermo Fisher bets on the process of discovery itself. It is a wager that, for 120 years, has rarely failed to pay off.

1. Company Origin and Evolution — How Thermo Fisher Became a Global Life Sciences Giant

Thermo Fisher Scientific’s roots stretch back over a century. The company in its current form was created in 2006 by the merger of two storied firms: Thermo Electron Corporation and Fisher Scientific International . Understanding Thermo Fisher’s origin means examining the legacies of both of these predecessors and the strategic milestones that transformed the combined entity into the life sciences giant we know today:

- 1902 – Fisher Scientific founded: Inventor and entrepreneur Chester G. Fisher established Fisher Scientific in Pittsburgh to supply laboratory equipment and chemicals . Over the ensuing decades, Fisher grew into a premier distributor of scientific supplies, serving academic and industrial labs. By the early 2000s, Fisher Scientific had become a global provider of lab consumables, reagents, and equipment – a “one-stop shop” for researchers – with a proud legacy spanning over a century. The Fisher Scientific brand celebrated its 120th anniversary in 2006 at the time of the Thermo merger .

- 1956 – Thermo Electron founded: George Hatsopoulos, an MIT-trained engineer, and his colleague Aris Melissaratos founded Thermo Electron Corporation in 1956 . Thermo Electron started as a scientific instruments company, initially focusing on advanced thermodynamics equipment and later expanding into analytical instruments (hence the “Thermo” name). Over the latter half of the 20th century, Thermo Electron incubated and acquired numerous high-tech instrument businesses – from mass spectrometers to environmental analyzers – becoming known for innovation in analytical and measurement technologies .

- 2006 – Thermo Electron and Fisher Scientific merge: In May 2006, the two companies combined to form Thermo Fisher Scientific, in a deal valued at ~$10.6 billion. The logic was compelling: Thermo’s strength in instruments and technology coupled with Fisher’s strength in consumables, distribution, and customer relationships created a comprehensive life sciences supply company . This merger instantly gave the new Thermo Fisher unmatched breadth, from cutting-edge lab equipment to everyday lab supplies, under brands like Thermo Scientificand Fisher Scientific . The merged firm could offer an “unrivaled combination of innovative technologies, purchasing convenience and pharmaceutical services” to the scientific community . Thermo Fisher’s headquarters was set in Waltham, Massachusetts, and Marc N. Casper (who joined Thermo in 2001) would eventually become CEO in 2009, ushering in an era of aggressive growth.

- Aggressive Expansion through Acquisitions (2010s): Post-merger, Thermo Fisher embarked on a decade-plus of strategic acquisitions to broaden its portfolio and global scale. Some transformative deals include: Dionex (2011), adding a leading chromatography instrumentation line ; Life Technologies (2013), a blockbuster $13.6 billion acquisition that brought DNA sequencing (Ion Torrent) and genetic research tools under Thermo Fisher’s roof ; FEI Company (2016), a ~$4 billion purchase adding industry-leading electron microscopy capabilities (cryo-EM); Affymetrix (2016) for $1.3 billion, adding microarray and genetic analysis tools ; and Patheon (2017) for $7.2 billion, which vaulted Thermo Fisher into the business of contract drug manufacturing (CDMO) for pharma and biotech clients . Each of these deals extended Thermo Fisher’s reach into new markets – from genomics to clinical production – building an ever more diversified and resilient company. Thermo Fisher’s scale advantagesgrew with each acquisition, cementing its status as the industry’s 800-pound gorilla. Notably, Thermo Fisher now accounts for an estimated 57% of the laboratory supply wholesaling industry’s revenues – an astonishing level of dominance for a once-fragmented sector.

- Recent Milestones – PPD and the Pandemic: In the late 2010s and early 2020s, Thermo Fisher continued to expand its capabilities. In 2019, it acquired Brammer Bio (for ~$1.7 billion) to gain expertise in gene therapy production . In 2021, Thermo Fisher made one of its largest moves ever by acquiring PPD, Inc. for $17.4 billion . PPD is a leading clinical research organization (CRO), and this deal firmly planted Thermo Fisher in the clinical trial management and drug development services arena – complementing the manufacturing services from Patheon and completing an end-to-end offering for pharma companies. The integration of PPD has gone well, delivering strong growth and synergies of $175 million within 3 years of closing . Around the same time, the COVID-19 pandemic (2020–2021) proved to be both a challenge and an opportunity for Thermo Fisher. The company played a crucial role in the pandemic response, supplying COVID testing kits (leveraging its PCR technology), personal protective equipment, vaccine development materials, and more . Pandemic-related demand caused a surge in Thermo Fisher’s revenue – from ~$25 billion in 2019 to ~$32 billion in 2020 and nearly ~$40 billion in 2021 – demonstrating the company’s ability to rapidly scale and deliver in a crisis. Thermo Fisher emerged from the pandemic larger and financially stronger, with enhanced credibility as a reliable partner to governments and healthcare clients in critical times.

- Today – A Global Life Sciences Titan: Fast forward to 2025, and Thermo Fisher Scientific stands as a behemoth with 125,000+ employees , serving over 400,000 customers worldwide (pharmaceutical & biotech companies, academic and government labs, hospitals and clinics, industrial and environmental sectors ). Its annual revenues now hover in the mid-$40 billion range – roughly quadruple the level at the time of the 2006 merger. For context, Thermo Fisher’s sales are about 50% larger than those of its next-largest competitor in the life science tools industry. The company’s broad portfolio and global infrastructure give it a presence in virtually every laboratory and research center on the planet. Thermo Fisher’s evolution over 120+ years (combining Fisher’s and Thermo’s histories) exemplifies how strategic M&A, innovation, and execution can create a dominant enterprise in a growth industry. Few companies can match Thermo Fisher’s combination of scientific heritage, scale, and adaptive growth. This foundation underpins its potential as a long-term dividend compounder.

2. Business Model Deep Dive — Segments, Revenue Streams, and Competitive Advantages

Thermo Fisher Scientific operates a highly diversified business model built around helping its customers achieve scientific breakthroughs and produce novel therapies. The company generates revenue through a wide array of products and services that support research, diagnostics, and biopharmaceutical production. Internally, Thermo Fisher organizes its offerings into four main segments :

- Life Sciences Solutions (≈35% of revenue) : This segment provides reagents, consumables, and instrumentsused in biological research, drug discovery, and the production of new therapies and vaccines . It encompasses many of Thermo Fisher’s “crown jewel” brands in biotechnology. Key offerings include PCR machines and reagents (for DNA amplification and diagnostics), gene sequencing platforms (e.g. the Ion Torrent NGS sequencers), cell culture media and reagents for growing cells, lab chemicals and antibodies, and specialized tools for genomics and proteomics research . Much of this segment was built via the 2013 Life Technologies acquisition, which brought in Applied Biosystems (known for PCR and DNA sequencers) and Invitrogen (a leader in research reagents). Life Sciences Solutions benefits from a high volume of consumable sales – e.g. enzymes, assay kits, and cell culture nutrients that labs must purchase repeatedly. This gives the segment a growth profile tied to global R&D spending. In recent years, Life Sciences Solutions saw surging demand for molecular diagnostic kits (like COVID-19 test kits) and for bioproduction supplies for vaccines . While some COVID-related sales have tapered, underlying trends in genetic research and biotherapeutics continue to drive this segment’s growth (Thermo Fisher noted the segment’s revenue is on an “increasing” trend) .

- Analytical Instruments (≈25% of revenue) : This segment covers Thermo Fisher’s broad portfolio of laboratory and field instruments used to analyze the composition of materials and substances. Think of precision machines that identify, quantify, and characterize chemical or biological samples. Notable product lines include mass spectrometers (for detecting molecules by mass; Thermo’s Orbitrap mass specs are industry-leading), chromatography systems (liquid and gas chromatographs for separating chemical mixtures, boosted by the Dionex acquisition ), spectrometers (infrared, UV-Vis, and atomic spectroscopy tools for analyzing materials), electron microscopes (Thermo is a top player in electron microscopy after acquiring FEI, enabling imaging down to the nanoscale), and laboratory automation systems. Customers for Analytical Instruments range from pharma companies analyzing drug purity, to environmental labs testing water quality, to industrial labs doing materials science . While instrument sales can be cyclical (often tied to capital spending budgets at labs), Thermo Fisher’s vast installed base yields a steady stream of aftermarket revenue – including software, accessories, service contracts, and consumables tailored to its instruments. This segment tends to have high profit margins, reflecting Thermo’s strong technological differentiation and brand reputation in instruments (scientists often prefer trusted brands for critical measurements). Thermo Fisher’s instrument business faces competition from specialized firms like Agilent, Waters, Bruker, and others, but Thermo’s breadth and continuous innovation (e.g. new launches like the Orbitrap Ascend mass spectrometer and Talos cryo-electron microscope in 2022–2025) have helped maintain its leadership. Overall demand for analytical instruments is stable to growing, with Thermo Fisher citing a stable outlook for this segment – new applications in biotech, environmental testing, and industrial quality control provide ongoing growth opportunities.

- Specialty Diagnostics (≈20% of revenue) : This segment focuses on diagnostic test kits, reagents, and clinical products used in healthcare and disease detection. It includes products for immunodiagnostics (e.g. Thermo’s Phadia line of allergy and autoimmune test systems ), molecular diagnostics (tests for infectious diseases, including PCR-based assays), microbiology supplies (culture media and rapid identification tests for bacteria/viruses – Thermo Fisher acquired microbiology specialists like Oxoid and Remel in 2007), and diagnostic reagents sold to hospitals and clinical labs. One notable part of this segment is Thermo’s One Lambda unit (acquired in 2012), which makes tests for tissue typing in transplant patients. Specialty Diagnostics also encompasses some clinical instruments such as blood chemistry analyzers and patient point-of-care test kits. During the COVID-19 pandemic, this segment’s molecular diagnostics business saw a major uptick from COVID testing demand, which then receded post-2021. For example, COVID-19 testing contributed over $3 billion to Thermo’s revenue in 2022 , much of it flowing through Life Sciences and Diagnostics segments. As pandemic testing wanes, the underlying growth in Specialty Diagnostics is now driven by factors like aging populations (more testing for diseases), the rise of personalized medicine (companion diagnostic tests for targeted therapies), and Thermo’s entry into specialized niches (e.g. the 2023 acquisition of The Binding Site for $2.7 billion expanded Thermo’s menu of diagnostic tests for multiple myeloma and other conditions ). Thermo Fisher indicates this segment is back to growth mode (“increasing”) after the pandemic-related volatility . While smaller than other segments, Specialty Diagnostics provides steady, high-margin revenue and deepens Thermo Fisher’s reach into hospitals and clinics – reinforcing customer relationships and cross-selling opportunities.

- Laboratory Products & Biopharma Services (≈20% of revenue) : This segment is Thermo Fisher’s largest by revenue (especially after recent acquisitions) and perhaps its most diverse. It combines two major components: Laboratory Products – essentially the consumables, equipment, and supply-chain services needed to run labs – and Biopharma Services – contract services for drug development and manufacturing. On the laboratory products side, Thermo Fisher, through the legacy Fisher Scientific channels, supplies everything from laboratory plastics (test tubes, pipette tips, petri dishes) to lab equipment (centrifuges, refrigerators, incubators) to safety supplies and chemicals. Thermo’s Unity Lab Services provides lab instrument maintenance and supply management services as well. In essence, Thermo can outfit an entire laboratory with both durable equipment and daily consumables – a reliable, recurring revenue stream. The “laboratory products” business is often lower-margin but high-volume and highly recurring (labs constantly need to reorder supplies). On the biopharma services side, Thermo Fisher has built a compelling end-to-end offering for pharmaceutical and biotech companies: it offers contract development and manufacturing (CDMO) through the Patheon unit (helping produce drug substances and drug products) , and clinical trial services (CRO) through PPD (managing clinical studies, logistics, and trial data) . With these capabilities, Thermo Fisher can support a new therapy from early research (providing reagents and lab tools), through clinical trials (running the trials and providing test kits), to manufacturing and commercial production (producing the drug and supplying quality control instruments). This makes Thermo Fisher an indispensable partner to biotech and pharma clients – essentially outsourcing key parts of the R&D and production value chain to Thermo. This segment’s revenue mix tilts toward service contracts and consumables, giving it a high degree of recurring revenue. Indeed, across Thermo Fisher’s entire business, a substantial portion of sales (roughly 80% in 2024) comes from consumables and services rather than one-time instrument sales . The Lab Products & Biopharma Services segment was significantly bolstered by the PPD acquisition in 2021; as a result, by Q4 2022 this segment contributed over half of Thermo Fisher’s total revenues . Thermo Fisher reports the segment’s growth trend as “stable” overall – laboratory products have steady demand, and biopharma services grow with pharma R&D pipelines (though can be influenced by the timing of biotech funding cycles, as discussed later).