Dividend Portfolio Review (Feb 2026): The “Growth Orchard” Strategy

Strategy: Quality Compounders & Dividend Growth

It’s not often that a beloved portfolio member simply disappears overnight, but that’s exactly what happened with First Savings Financial Group (FSFG) at the end of January. FSFG was unexpectedly acquired and delisted (its last trading day was January 30, 2026), leaving me both surprised and a little sentimental. I watched as FSFG merged into a larger bank (First Merchants Corporation, ticker FRME) without much warning on my part. As of today (February 4, 2026), the FRME stock I received in exchange is worth roughly $170, and by the time you’re reading this around February 10 it will likely be about $176. It’s a strange feeling to see a familiar small-cap holding vanish into a bigger entity, and I admit it caught me off guard.

In reflection, this turn of events carried some humbling lessons. I realize now I hadn’t fully appreciated the buyout risk that comes with holding a smaller regional bank like FSFG. In hindsight, that was a subtle violation of Peter Lynch’s old “know what you own” principle – I thought I knew FSFG well, but I didn’t consider that its fate could be decided by a larger fish in the pond. The acquisition news blindsided me, and I have to own that oversight with a bit of chagrin. On the bright side, I caught the change and adjusted quickly (thankfully before it could become a larger problem for the portfolio), so at least no lasting harm was done. Still, I’m left with a renewed appreciation for staying vigilant, even with seemingly stable dividend payers.

The upside to this shake-up is the opportunity to strengthen the portfolio’s core. With FSFG gone, I’ve decided to bring in S&P Global (SPGI) as a long-term replacement – essentially a permanent “emergency anchor” allocation that probably should have been there from day one. SPGI is a far bigger and steadier company, and it’s a stock I have high conviction in for the long haul. There’s some humility (and a touch of irony) in admitting that perhaps I should have opted for this blue-chip stalwart instead of a niche bank initially, but better late than never.

In any case, I’m confident that swapping FSFG for SPGI ultimately makes the portfolio more resilient. It’s a bittersweet farewell to FSFG, but also an excited welcome to SPGI – and with that transition complete, we can move forward into the rest of the February review with lessons learned and optimism intact.

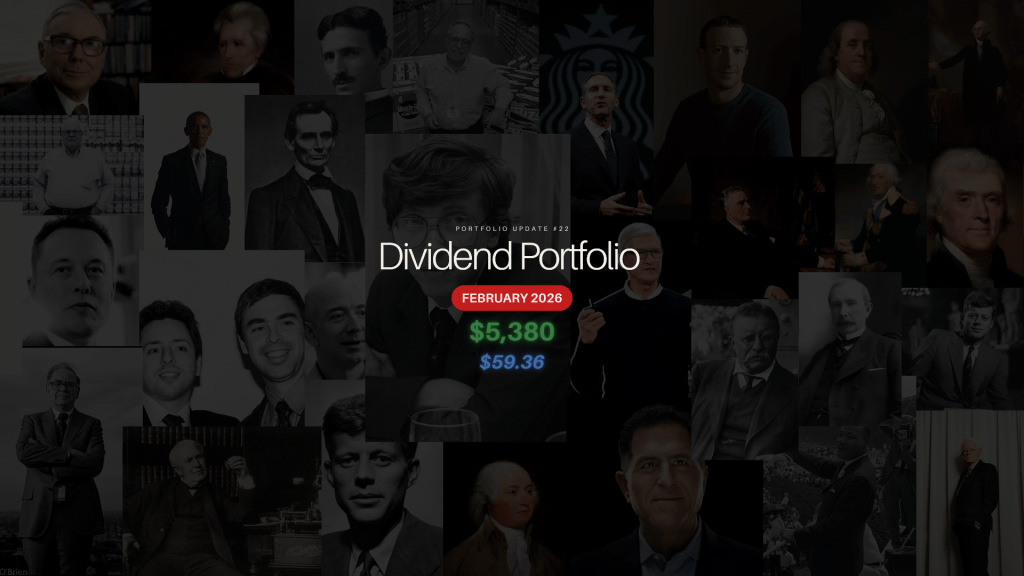

DP.22 | Dividend Portfolio Update #22 (February 2026)

To my fellow investors,

This month’s portfolio review comes with a twist we didn’t quite expect. It’s not often that a beloved holding simply vanishes overnight, but that’s exactly what happened at the end of January. First Savings Financial Group (FSFG), one of our small community bank positions, was unexpectedly acquired and delisted (its last trading day was January 30, 2026). I watched FSFG merge into a larger regional bank (First Merchants Corp, FRME) with little warning. As of today (Feb 4), the FRME stock received in the deal was worth ~$170, and by the time you’re reading this around Feb 10 it’s about $176. Seeing a familiar small-cap holding vanish into a bigger entity was surreal, and I admit it caught me off guard. It’s a humbling reminder that even “safe” dividend payers can surprise you – a nod to Peter Lynch’s adage “know what you own.” In hindsight, I hadn’t fully appreciated the buyout risk of a tiny bank like FSFG. The acquisition news blindsided me, and I have to own that oversight with some chagrin. On the bright side, I acted quickly (thankfully before any damage was done), and with FSFG gone I’ve taken the opportunity to strengthen the portfolio’s core.

Enter S&P Global (SPGI). I decided to redeploy FSFG’s proceeds into S&P Global – essentially adding a blue-chip “emergency anchor” that probably should have been in the mix from day one. SPGI is a far larger, steadier enterprise (a true Dividend Aristocrat with decades of raises), and it’s a stock I have high conviction in for the long haul. There’s humility (and irony) in admitting perhaps I should have opted for this blue-chip stalwart over a niche bank initially – but better late than never. Swapping FSFG for SPGI ultimately makes the portfolio more resilient. It’s a bittersweet farewell to FSFG, but also an excited welcome to SPGI. With that transition complete, let’s dive into the February review with lessons learned and optimism intact.

1. February Scoreboard – Portfolio at a Glance

Despite the shake-up, the portfolio’s growth continues to impress. We’ve crossed a couple of meaningful milestones as we head into February:

- Total Portfolio Value: ~$5,380 (up from ~$4,952 at year-end 2025)

- Invested Capital (Stocks): ~$4,975 (with ~$1,000 cash reserve on hand)

- Holdings: 22 dividend-paying companies (net +1 new position since last month)

- Forward Annual Dividend Income: $59.36 (projected)

- Portfolio Dividend Yield: ~1.1% (on current value, ~1.2% yield on cost)

- Overall Performance: +8% total gain on invested capital (unrealized)

The Takeaway: We’ve surpassed $5k invested in equities – exciting thresholds for this “toddler” portfolio. The market’s recent strength (plus new contributions) helped boost assets, and our focus on quality is paying off: the portfolio is up roughly 8% from cost basis, confirming that a “quality first” approach can deliver solid growth even as the dividend income builds slowly. The forward income of ~$59/year is still nominal (about $4.95 per month on average), so we’re not paying any bills yet – but the snowball is rolling faster each month.

2. Portfolio Changes: From FSFG to SPGI – Core Strengthening

As noted, the big change this month was the surprise removal of FSFG after its buyout. This event, while unexpected, came with valuable insights:

- Lesson Learned: Relying on a small-cap bank for income (FSFG provided ~3–4% of our dividends) carried hidden risk. One small bank was supplying a large chunk of our income, and its sudden disappearance highlighted our income concentration issue. We loved FSFG’s dividend, but having a quarter of your income from one tiny bank was a vulnerability – one we’ll be mindful to avoid going forward. It reinforced the importance of vigilance even with “stable” dividend payers, and of diversifying our income sources.

- Portfolio Response: The FSFG proceeds (after conversion to FRME stock) have been redirected into S&P Global (SPGI), a high-quality dividend growth titan. S&P Global brings to the table a modest ~1% yield but rock-solid dividend growth (45+ years of consecutive raises) and an essential business (financial data, indexes, and credit ratings) that should compound for decades. In fact, SPGI just announced a token increase to its quarterly dividend ($0.97 from $0.96) in January – marking its 50+ year streak of hikes. By adding this blue-chip anchor, we’ve effectively traded a niche high-yield name for a globally diversified dividend aristocrat. The result is a more balanced and resilient income stream.

All told, while I’ll miss FSFG (and the charm of its outsized yield), the swap into SPGI leaves the portfolio on stronger footing. Sometimes the market forces your hand in a good way: this was a chance to upgrade quality, and we took it. Now, with that behind us, let’s check in on all the portfolio holdings and see how each is contributing.

3. Stock-by-Stock Updates – February 2026 Check-Up

Below is a quick status update on each of our 22 holdings. Consider this a “roll call” of the portfolio – highlighting recent news, dividend moves, or performance noctes for each stock:

1. Apple (AAPL) – Our $4 trillion tech giant remains a cornerstone growth holding. Apple’s dividend yield is modest (~0.6%), but it continues growing payouts every year (we expect another small raise in April). In the meantime, Apple’s massive share buybacks and resilient iPhone revenue keep driving the stock upward. The next quarterly dividend of $0.26 per share is slated for Feb 12, adding a handy $0.41 to our coffers (for our ~1.6 shares). Slow and steady with this one – Apple is all about long-term compounding (both in stock price and dividend).

2. Microsoft (MSFT) – Microsoft has quietly become one of our larger dividend payers among the tech names. After a hefty 9.7% dividend hike last fall (to $0.91 quarterly), MSFT now yields about 1.0%. The company’s growth engine (Azure cloud, enterprise software) is still in high gear, evidenced by strong earnings and a ~+40% stock run in 2025. This Dividend Aristocrat (20+ years of raises) provides both offense and defense in our portfolio. The new higher dividend hits our account in March, and we’re happy to let those reinvested pennies buy more of this compounder.

3. Alphabet (GOOGL) – While Alphabet pays a small dividend, it has been a monster stock performer for us. Alphabet’s share price is up roughly 70% from our cost basis, making it one of our top capital gainers. We include Google in this dividend portfolio because of its dominant business and the possibility that one day it could initiate dividends (with their cash hoard, it’s plausible in the future). For now, Alphabet’s massive buybacks and growth (Google Cloud, Search, YouTube) are its way of returning value. It remains a key growth engine on the “offense” side of our strategy, balancing out the slower dividend payers.

4. Meta Platforms (META) – Like Alphabet, Meta currently pays a small dividend, but its stock gains have been impressive. META has reinvented itself post-2022 slump, cutting costs and refocusing on core apps while still investing in the metaverse. The market has rewarded these moves – our Meta position is up nicely (though it’s dipped a bit in recent weeks amid tech volatility). We hold Meta as a pure growth asset with the understanding that maybe years down the line, as the company matures, it could join the dividend payer club. Even if not, Meta’s free cash flow (and huge share buybacks) make it a valuable total return contributor for us.

5. Visa (V) – Visa remains a low-yield (<0.8%) but high-growth dividend stock in our financials sleeve. In late 2025 Visa delivered a 13.6% dividend increase (to $0.67 quarterly), underlining why we love these payment processors – they reliably crank out double-digit dividend growth. Visa’s business – facilitating global payments – is firing on all cylinders as travel and consumer spending stay robust. The stock has been steady to up; nothing dramatic, just consistent performance. We have ~0.7 shares generating ~$1.85 in annual income here. Visa’s 17-year streak of dividend increases (and plenty of room to keep growing it) makes it a “sleep-well” holding.

6. Mastercard (MA) – Our Mastercard position is small (just ~0.4 of a share), but it’s equally mighty in dividend growth. MA delighted shareholders in December with a 14% dividend hike, raising its quarterly payout from $0.76 to $0.87 per share. The new annual rate ($3.48) added a bit to our forward income. Mastercard also announced a huge $14 billion buyback alongside the increase, signaling confidence in its future. The stock, like Visa, isn’t cheap (P/E ~35), but for a capital-light cash machine growing ~12%+ a year, we’re willing to hold and even add on dips. We view MA as a long-term compounder that will keep our dividend growth engine humming.

7. S&P Global (SPGI) – New entrant! S&P Global joins the portfolio as a best-in-class dividend stalwart. SPGI has raised its dividend for 50+ consecutive years, though the latest boost (Jan 2026) was a token ~1% uptick (quarterly $0.97). Don’t let that small hike fool you – SPGI has grown its dividend at ~10% CAGR over the past decade. The company’s franchises (S&P ratings, indices like the S&P 500, and data/analytics from the IHS Markit merger) enjoy wide moats and steady demand. Our position is currently modest (~0.3 shares), contributing ~$1.18 in annual income, but we intend for this to be a core holding. SPGI’s yield (~1%) won’t knock your socks off, but its quality and growth profile are impeccable. We’re very happy to “swap” into this name and expect it to be a long-term anchor for both dividend growth and stability.

8. Home Federal Bancorp of Louisiana (HFBL) – HFBL continues to be the quiet workhorse of our dividend income. This small Louisiana community bank now pays a quarterly dividend of $0.135 per share, after notching its 12th straight annual increase last year. With ~28 shares, HFBL remains our single largest income contributor – about 23% of our total forward dividends. That concentration is something we’re mindful of (one reason we want to grow other positions’ income faster), but we still like HFBL’s fundamentals. The stock is actually up about +33% from our cost, reflecting solid performance. Recent earnings have been stable, and the bank navigated the 2023–25 rate volatility without drama. We’ll continue to collect HFBL’s dividend “paycheck” and possibly trim or re-balance if an even better opportunity arises, but for now this high-yield micro-cap is doing its job nicely.

9. FS Bancorp (FSBW) – Our other community bank, FSBW (based in Washington state), is still chugging along steadily. FSBW just gave investors a pleasant surprise: a dividend raise in January, bumping the quarterly payout from $0.28 to $0.29 per share. That 3.6% increase marks FSBW’s 5th consecutive year of raises (and 52nd consecutive quarterly dividend payment). We hold ~4 shares, so the raise adds roughly $0.16 to our annual income – every bit counts! FSBW’s stock price has been relatively stable (community bank shares were under pressure in 2025, but FSBW held up). With a yield around 3% now and a low payout ratio, this holding provides a nice income kick. It remains a “boring is good” part of our defense, and we’re encouraged to see management’s confidence via that dividend boost.

10. Becton Dickinson (BDX) – BDX is one of our healthcare cornerstones and a newly crowned Dividend King (50+ years of increases). In December, Becton Dickinson’s board approved the 54th consecutive annual dividend hike, albeit a token +1% raise (quarterly from $1.04 to $1.05). That incremental bump keeps the streak alive and our forward income creeping upward. We own a small fraction of a share (~0.85 of a share), producing ~$3.84 annually for us. BDX’s yield is about 1.4%, and while the stock was flat in recent months (healthcare was out of favor), we’re not concerned. This is a “Steady Eddie” medtech company (think surgical tools, diagnostics, medical devices) with a wide moat and reliable growth. The tiny raise this year is actually typical – BDX often does mid-single-digit increases, but last year’s was modest due to big investments and some debt from past acquisitions. We expect BDX to remain a foundation holding that quietly compounds and throws off a slightly bigger dividend each year.

11. Automatic Data Processing (ADP) – ADP is our Dividend King in the tech/industrials space and it just delivered royally for us. In November, ADP announced its 51st consecutive yearly increase, a hefty 10% boost to the quarterly dividend (now $1.70 per share). This raise (effective Jan 1) lifted ADP’s annual payout to $6.80 per share. While our share count is small (~0.44 shares), that added roughly +$0.28 to our forward income. ADP’s stock had been a slight laggard (down a few percent from our buy price as of last month), but we view dips in this name as opportunities. The company’s fundamentals are strong – it’s a leader in payroll and HR services, with robust recurring revenue. A 10% dividend hike amid a softer stock price means we’re reinvesting dividends at a bargain and positioning for future gains. ADP remains a core holding bridging our tech and income sides, and we’re in it for the long run.

12. American States Water (AWR) – AWR is our ultra-reliable utility Dividend King. As the longest-running dividend growth streak in America, AWR has increased its dividend **for 68+ years (nearly 7 decades straight)*. In September 2025, it gave us an 8.3% raise (quarterly to $0.504 per share), and we’re now collecting ~$2.77 annually from our share. That’s a 2.1% yield on current price – not high, but remember this company literally never misses a yearly hike. AWR’s business (regulated water utility in California) is as defensive as it gets. Rising interest rates last year pressured utility stocks (including AWR), but that’s short-term noise. We’re content holding this as a stability anchor. The next raise likely comes mid-2026, and management targets ~7% dividend CAGR long-term, which is excellent for a utility. In sum, AWR adds ballast to our ship and a bit of income growth too.

13. Waste Management (WM) – Waste Management is another steady defensive holding, and it just gave us some big news. WM’s board approved a 14.5% dividend increase for 2026 – planning to raise the quarterly payout from $0.825 to $0.945 starting this spring. This marks WM’s 23rd consecutive year of hikes, and it’s an unusually large jump, reflecting the company’s confidence and strong cash generation. For us, once that raise is in effect, our ~0.8 shares will see annual income climb from ~$2.57 to about $2.95 – a nice boost of ~$0.38 a year. WM’s yield will move to ~1.7% at the new rate. Beyond dividends, the company is also repurchasing shares (a new $3 billion buyback was announced alongside the dividend hike). Operationally, trash collection is an all-weather business with high barriers to entry, and WM dominates the North American market. The stock has been relatively flat recently, but with this generous dividend bump and consistent performance, WM remains a cornerstone defensive stock for us. We’ll gladly reinvest its fatter dividends in 2026.

14. Hamilton Beach Brands (HBB) – HBB is one of our smallest positions but one with a decent yield. This appliance-maker (think kitchen gadgets) pays a quarterly dividend of $0.12 per share, which comes out to a 2.5% yield at the current price. We hold a few shares (roughly 3.2 shares), providing about $2.58 annually to our income. HBB’s dividend has been stable in recent years (no big growth, but holding steady). The stock itself quietly appreciated ~+29% from our entry, as the company recovered from supply chain issues and benefited from solid consumer demand. While HBB is a small-cap and a bit cyclical, we like it as a “niche” dividend payer that diversifies our income (consumer appliances aren’t correlated with tech or banks). We’re not expecting major dividend hikes here, but the current payout appears sustainable (payout ratio under 50%). We will continue to monitor HBB’s earnings, but so far it’s a nice little contributor that pays us to wait.

15. Costco Wholesale (COST) – Our Costco holding may be tiny (≈0.2 of a share), but we have big respect for this retail powerhouse. Costco’s dividend yield is under 0.8%, yet it’s a sneaky-good dividend growth stock. In May 2025, Costco gave a 13% raise (to $1.30 quarterly), and historically it has declared hefty special dividends every few years (though none in 2025). Our fractional share yields about $1.72/year to us, and more importantly, it keeps us psychologically invested in Costco’s story. The stock is pricey (as it often is), but its business model – membership-based, high volumes, ultra-loyal customers – churns out reliable cash flow. We see Costco as a long-term accumulator position: add a bit on dips, reinvest dividends, and one day perhaps enjoy a surprise special dividend. Until then, we’re content with the ~10% annual dividend growth and the knowledge that this is one of the highest-quality retailers on the planet.

16. Apple (AAPL) – (See #1 above – Apple already covered.)

16. UnitedHealth Group (UNH) – UNH is our representative from the healthcare insurance sector and a dividend growth machine. Its yield is about 1.4% currently, but UnitedHealth has been raising its dividend at a double-digit rate every year (typically announced each June). For example, in 2025 UNH hiked the quarterly payout by 14% to $1.88 per share – marking over a decade of consecutive increases. We own a small stake (~0.2 shares), giving us ~$0.92 in annual income for now. UNH’s stock had a roller-coaster 2025 (managed care stocks faced political noise), but the company’s earnings are rock-solid and it’s trading better lately. UnitedHealth’s diversification (insurance, Optum health services, pharmacy benefits) makes it a cash cow. We view UNH as a growth-and-income play: it offers defensive characteristics in downturns and robust growth in good times. We’ll look to add more on any weakness, as this is one of those compounders that could realistically double its dividend in ~5 years if trends continue.

18. Intuit (INTU) – Intuit is a fintech powerhouse we initiated in late 2025, albeit currently as a fractional position. Even a small slice of Intuit added noticeable income: the company raised its dividend 15% in October (to $1.20 quarterly), which set its annual payout at $4.80 per share. We only own about 0.1 of a share at the moment, yielding ~$0.52/year for us, but the rationale for Intuit isn’t the current income – it’s the growth trajectory. Intuit (maker of TurboTax, QuickBooks, Credit Karma, Mailchimp, etc.) generates gobs of free cash flow and returns a lot to shareholders (over $4B via buybacks+dividends in FY2025). The stock carries a low yield (~0.7%) but management is committed to double-digit dividend growth and we’ve already benefited from that. Our plan is to build up INTU over time on dips. The recent earnings were strong, and the company’s push into AI-driven features could further boost its value proposition. Intuit fits our strategy of holding “growth-oriented dividend payers” – it’s the kind of name that could quietly 10x its dividend over a decade if all goes well.

19. Cintas (CTAS) – Cintas might be the smallest position by share count (~0.1 shares), but it’s one of the most exemplary dividend stocks in our roster. Cintas is a bona fide Dividend King with 42 years of consecutive increases. It yields only ~1% for us, yet its dividend growth has been 20%+ CAGR over the past 10 years – phenomenal. The company last split its stock 4-for-1 in 2024 and subsequently raised the quarterly dividend to $1.56 (post-split) in late 2025. We’re collecting about $0.47 a year from our sliver of CTAS, and we see this as a “set it and forget it” position to expand over time. Cintas’s business (uniform rentals, workplace services) is very steady and profitable, and management is top-notch in capital allocation. They target ~30% of earnings for dividends and use the rest for buybacks and M&A – a great balance. In short, Cintas exemplifies the ideal dividend compounder, and we’re thrilled to have even a small stake in this elite company. We’ll continue to drip reinvestments here and look for opportunistic adds.

20. The Coca-Cola Company (KO) – KO is as classic as it gets – a true Dividend King with 61 consecutive years of raises. We started a small position in Coca-Cola as a way to anchor some reliable income in the portfolio’s defensive side. Our fraction of a share (≈0.25 shares) produces about $0.47 in annual income for now, based on KO’s current quarterly dividend of $0.46. That’s essentially a 3% yield – among the highest of our holdings. While KO’s dividend growth is slow (typically ~4% per year, in line with its steady EPS growth), the consistency is unparalleled. In fact, we expect KO to announce its 62nd annual increase this month (Feb 2026), likely raising the quarterly payout a penny or two as usual. The stock itself is a bit sluggish (it was flat-to-down in 2025 amid consumer staples weakness), but that doesn’t bother us – we primarily own KO for stability and income. This is a name we may add to over time, especially if its yield stays attractive. Coca-Cola’s global brand strength and pricing power make it a sleepy but solid part of our long-term dividend strategy.

21. Thermo Fisher Scientific (TMO) – Thermo Fisher is another new addition to the portfolio, reflecting our strategy of selectively adding elite growth companies even if their yields are very low. TMO currently yields only ~0.3%, but it’s a leader in life sciences and lab equipment – a picks-and-shovels play on the healthcare and biotech industries. Importantly for us, Thermo Fisher has been growing its dividend at a rapid clip. In early 2025, it boosted the quarterly dividend by 10% (to $0.43), and it has a history of double-digit raises (including an 18% hike in 2024). We initiated a tiny fractional position (on the order of hundredths of a share), so our current income from TMO is essentially $0 (just a few cents). However, we view TMO similarly to Intuit or Cintas – as a long-term growth play that also happens to be committed to shareholder returns. Thermo’s business is firing on all cylinders (over $40B revenue, serving a broad array of scientific markets), and it throws off strong cash flow for buybacks and dividends. We’ll be looking to increase our stake in TMO gradually. Consider this one “a sapling in our dividend orchard” – small now, but with the potential to become a mighty income tree in the future.

4. Dividend Income Growth – Month-over-Month Progress

The primary goal of this portfolio is to grow the passive dividend income, and February brought another step forward. Our forward annual dividend income now stands at $59.36, up from about $54.43 last month. That’s a 9% jump in one month, which is fantastic progress at this early stage. Several factors drove the increase:

- New Capital & Positioning: The addition of SPGI contributed roughly +$1.18 to our annual income (since we had no SPGI before). We also added small positions in KO and TMO, which together add a few more cents now but lay the groundwork for future income. The portfolio now has more “dividend weight” in blue-chips, which should help income growth over time.

- Dividend Raises: This past month saw a flurry of hikes from our holdings. We benefited from ADP’s ~10% raise (+$0.16/qtr), Mastercard’s 14% raise (+$0.11/qtr), BDX’s 1% raise (+$0.01/qtr), FSBW’s 3.6% raise (+$0.01/qtr) and HFBL’s earlier 2025 raise now fully reflected (+$0.015/qtr). In aggregate, these boosts added a few dollars to our forward annual income. For example, ADP’s increase alone gave us about +$0.28/year (on 0.44 shares), and Mastercard’s about +$0.17/year (on 0.38 shares). It’s these incremental gains that fuel our snowball. Notably, Waste Management’s 14.5% hike will add another ~$0.38/year once effective – pushing our forward income over $59.7 going forward.

- Reinvestments: We continue to reinvest every dividend back into the portfolio. January’s received dividends (from the likes of HFBL, AWR, etc.) were small in dollar terms, but they purchased fractional shares that will themselves generate dividends. This compounding, while minuscule now, will accelerate as our income grows. Every $1 reinvested adds roughly $0.01–$0.03 to our annual income depending on the yield of the stock it buys. It’s truly “building the snowball” from the ground up.

To put the $59.36 figure in perspective: a year ago, our forward income was around $34, so we’ve nearly doubled it in 12 months. The combination of new contributions, strategic stock additions, and healthy dividend increases has created a strong upward trajectory. Our yield on cost has risen to 1.19% (from ~1.1% a month ago and ~0.9% mid-last-year), indicating that the portfolio’s cash yield on our invested dollars is climbing. This is exactly what we want to see. We’re not chasing high current yield; we’re steadily growing yield organically via dividend hikes and smart buys. The portfolio’s overall yield is ~1.1% on market value – still lower than a bank account – but the dividend growth rate of our holdings is high (weighted average in the high single digits percent). That means patience will be rewarded. If we sustain, say, ~10% dividend growth annually, our yield on cost will double in about 7 years (all else equal). That’s the long game we’re playing.

One more point of pride: the portfolio’s income stream is becoming more balanced. Last month, HFBL alone was ~24% of our total income. After February’s changes, HFBL is about 23% and falling, as others (like ADP, Visa, SPGI, etc.) grow their share. We still have work to do to reduce single-stock income reliance (HFBL and our top 4 payers still make up ~50%+ of income), but we’re moving in the right direction – primarily by growing the blue-chip dividends around them. The goal for 2026 remains to have the Apples, ADPs, and Intuits of the world contribute more meaningfully, so that no single small cap dominates the income flow.

5. Outlook – Staying the Course (and Staying Vigilant)

After an eventful month, the strategy going forward remains fundamentally unchanged: buy wonderful businesses, reinvest the dividends, and hold for the long term. The surprise FSFG episode reinforced the importance of quality and diversification. While we don’t plan for buyouts, it’s good to know our portfolio can weather such an event and even come out stronger by reallocating wisely.

Looking ahead to the next few weeks, a few things are on our radar:

- Deploying Cash: We have about $1,000 in cash sitting (roughly 16% of the portfolio) as dry powder. This is intentionally a bit higher than usual – partly due to recent contributions and the FSFG transaction. I’m in no rush to deploy it all at once; with the market near highs, patience is key. However, I am eyeing a couple of our underweight names for potential topping up. Adding to defensive stocks like AWR or KO on dips, or boosting high-growers like INTU or TMO if opportunities arise, could be smart moves. The cash provides flexibility to respond to any volatility (for example, if we get a February/March pullback, we’ll be ready to buy quality on sale).

- Dividend Announcements: We’re expecting a few dividend declarations in the coming weeks. Notably, Coca-Cola (KO) should announce its annual increase this month – likely a ~4% uptick, which we’ll happily take. Also, some of our tech names will go ex-dividend soon (Microsoft in mid-Feb, Apple in Feb, etc.), meaning more small reinvestments on the way. We’ll watch for UnitedHealth’s next raise in June and Intuit’s later this year. Part of the fun is anticipating these “pay raises” for our passive income and planning how to reinvest them.

- Monitoring Earnings & News: Earnings season is underway. Thus far, results have been favorable for our holdings (Microsoft beat expectations, Visa/Mastercard reported strong holiday-quarter numbers, etc.). We’ll keep an eye on any developments that might affect our companies’ long-term outlooks – whether it’s regulatory news for Visa/MA, AI updates from big tech, or interest rate trends impacting our banks and utilities. The macro backdrop (a possible Fed rate pause or cut later in 2026, inflation trends, etc.) also factors into our game plan, especially regarding when to deploy that cash reserve. Overall, we remain cautiously optimistic: the economy is holding up, and dividend growth companies are continuing to thrive.

Conclusion: The February update encapsulates why a balanced dividend growth strategy can be so rewarding. We navigated an unforeseen hurdle (losing a holding to acquisition) and used it to our advantage by upgrading the portfolio’s quality. Meanwhile, our dividend income kept climbing, fueled by both our actions and the companies’ generosity. The portfolio is still young and small, but it’s growing sturdier by the month – much like a young tree sprouting new branches. We’ll continue to tend this dividend “orchard” with care: planting new seeds (new positions like SPGI, TMO), watering them regularly (reinvesting dividends), and pruning/rebalancing when necessary (trimming risk, as we did with the barbell concentration). As always, the keys are patience, consistency, and vigilance.

Thank you for reading and following along on this journey. Here’s to another month of steady compounding – see you in the next update!

Our portfolio’s projected annual dividends have climbed to about $59.36 (≈$4.95/mo), up from ~$54.43 last month. This ~9% jump is largely due to fresh cash contributions and several dividend hikes in late 2025/early 2026. We review each holding below, noting any recent dividend changes and their impact on our monthly income.

- Apple (AAPL): Apple declared a $0.26 quarterly payout (payable Feb 12, 2026), up from $0.25 a year ago. This matches Apple’s pattern of modest raises – in Sept 2025 the board increased the dividend from $0.22 to $0.25, and now to $0.26 per share. The new $0.26/share (≈$1.04 annual on 1 share) was confirmed with Q1 results. Apple’s dividend yield remains low (~0.5%) but the hike adds a few cents to our forward income.

- Starbucks (SBUX): Starbucks boosted its quarterly dividend slightly to $0.62 in late 2025. That 1.6% raise (from $0.61) was announced Oct 1, 2025 and paid Nov 28, 2025. No further change was declared this winter, so SBUX remains at $0.62/Q ($2.48 annually) for now. Starbucks has a long history of raises, but typically only a small bump each year.

- Dell Technologies (DELL): Dell’s board declared a $0.525 quarterly dividend in its Nov 2025 results, meaning $2.10 annual. This continued the earlier 18% increase approved in Feb 2025. Dell has held the $0.525 per share level through late 2025 (no further raise announced), so our Dell income is stable at ~$2.10 per share per year.

- FS Bancorp (FSBW): FS Bancorp raised its quarterly payout from $0.28 to $0.29 (3.6% increase), with the new $0.29 declared Jan 21, 2026 and payable Feb 19. At our ~2.7 share position, this adds roughly $0.01 per quarter per share, or about +$0.02 monthly to our income. The annualized rate is now ~$1.16 per share.

- Becton Dickinson (BDX): BDX announced a $1.05 quarterly dividend (annual $4.20) in Nov 2025, up just 1% from $1.04. As a Dividend Aristocrat, BDX has raised each year for decades. The latest tiny hike (to $4.20/yr) provides a modest bump. At ~0.84 share, our annual BD dividend is now ~$3.52.

- Automatic Data Processing (ADP): ADP’s board raised the quarterly dividend to $1.70 in Nov 2025 (a 10% jump from $1.54). This was paid Jan 1, 2026. With ~0.439 share, our ADP dividend run-rate is now about $3.66/yr (from ~$3.38 prior). ADP’s generous increase (its 51st straight year of raises) adds noticeably to our portfolio income.

- American States Water (AWR): AWR approved a quarterly dividend of $0.5040 in Oct 2025. This represents roughly an 8% raise over the previous ~$0.47 payout. The new $0.5040 (annual ~$2.016) continues AWR’s string of 71 consecutive annual hikes. At our ~0.26 share, we earn about $0.52/yr from AWR.

- Waste Management (WM): Waste Management’s board approved a 10% boost in the 2025 dividend (to $0.825 per quarter, $3.30/yr). More notably, WM announced a planned 14.5% hike to $0.945 per quarter for 2026. In short, WM will pay about $0.945/Q ($3.78/yr) next year. For now our incoming WM dividend stays at the current $0.825/Q, but next year’s jump will further lift our income stream.

- Microsoft (MSFT): Microsoft declared a $0.91 quarterly dividend on Sept 15, 2025 (10% higher than $0.83). That payout was paid Dec 11, 2025. MSFT typically raises ~10% yearly. With ~0.329 share, our MSFT annualized dividends are ~$2.66 (0.329×3.64), and the recent hike ensured it remains on track.

- Hamilton Beach Brands (HBB): In May 2025 Hamilton Beach announced a 4.3% dividend increase to $0.12/Q. This was paid June 13, 2025. With ~2.58 shares, we now get about $1.24 per year from HBB. It’s a small, steady consumer name and the raise added a few cents/month to our income.

- Visa (V): Visa’s board raised the quarterly payout to $0.67 in Oct 2025 (up from $0.62/Q). The $0.67 was paid Dec 1, 2025 (record date Nov 12). With ~2.7 shares, this yields ~$1.80/yr now (2.7×4×0.67). Visa usually increases roughly 5–10% annually; this raise adds a modest amount to our monthly dividends.

- Costco (COST): Costco surprised investors in Apr 2025 by lifting its quarterly dividend to $1.30 (from $1.16). This $1.30/Q ($5.20/yr) was paid May 16, 2025. No new changes have been announced since. At ~0.13 share, we earn about $0.65/yr from Costco. Its large base payout means it contributes steadily, though its hikes are infrequent.

- Apple (AAPL): (See above #1.)

- Mastercard (MA): Mastercard’s directors approved a quarterly dividend of $0.87 on Dec 9, 2025 (a 14% jump over $0.76). This will be paid Feb 9, 2026. We hold ~0.382 share, so our annualized MA dividends rose to ~$1.36 (0.382×4×0.87). The new raise adds a few cents more to our monthly income compared to last year’s run-rate.

- S&P Global (SPGI): The board approved a small 1% raise to $0.97/Q on Jan 14, 2026 (from $0.96). The payout on Mar 11, 2026 will be $0.97. SPGI now pays $3.88/yr. We just established this position (replacing FSFG), owning ~0.342 share. Its increased dividend adds ~$0.04/yr to our income. (SPGI’s payout is very safe: it’s paid dividends since 1937 with 55+ years of raises.)

- Alphabet (GOOGL): Alphabet only began paying a regular dividend in 2024. It currently pays $0.21 per quarter (announced Oct 28, 2025). We hold ~0.175 share, so GOOGL yields roughly $0.14/yr to us. No increase was announced; the payout remains $0.21/Q. In sum, GOOGL contributes very little to our dividend stream (only 1–2% of it).

- UnitedHealth Group (UNH): UNH’s board declared a $2.21 quarterly dividend on Nov 7, 2025 (up from $2.14 last quarter, ≈3.3% increase). This was paid Dec 16, 2025. Our ~0.318 share now earns ~$0.92/yr (0.318×4×2.21). The latest raise added only a few cents to that, so UNH is a steady 2–3% contributor to monthly income.

- Meta Platforms (META): Meta pays no dividend (0% yield), so it adds nothing to our income. We hold ~0.115 share as a growth/tech position only. There are no dividend developments for META to report.

- Intuit (INTU): Intuit announced a large raise to $1.20/Q (15% higher) in Nov 2025. This $1.20 was paid Jan 16, 2026. Our ~0.433 share now yields ~$2.52/yr (0.433×4×1.20). The 15% bump (from $1.04) adds about $0.08/yr to our Intuit income, a nice boost driven by Intuit’s strong performance.

- Cintas (CTAS): Cintas declared a $0.45 quarterly dividend on Oct 28, 2025. (This was a 15.4% raise from the prior $0.39.) Our ~0.244 share now yields ~$0.44/yr (0.244×4×0.45). The higher payout (paid Dec 15, 2025) modestly increased our Cintas income; CTAS remains a reliable industrial payer.

- Coca-Cola (KO): Coca-Cola’s dividend is about $0.51 per quarter (last paid Dec 15, 2025). This was up from $0.50, a ~2% raise announced in early 2025 (Feb 2025 board increase). Our 0.92 share yields ~$1.88/yr (0.92×4×0.51). KO’s most recent 5.2% annual raise (announced Feb 2025) was modest, so KO adds a steady but small ~3% of our income.

- Thermo Fisher (TMO): We currently hold no shares of TMO, so it contributes nothing. (TMO normally pays a significant dividend, but it’s not part of our portfolio now.)

Overall Impact: Thanks to these updates, our forward dividend income is up about 9% month-over-month. In particular, the large raises from Mastercard (+14%) and Intuit (+15%) and modest hikes at Visa, ADP, etc. pushed up the total. We also turned FSFG’s cash into a position in SPGI, a blue-chip with stable payouts. Going into Feb, the portfolio should collect roughly $61–62 in dividends for the month (including declared and estimated), vs. about $56 in Jan – a clear increase.

In summary, each holding continues to pay its dividend, and the recent increases have slightly boosted our run-rate. We’ll keep reinvesting these growing payouts. Per our strategy, this steady rise in income – even if modest in absolute terms – is the main takeaway. All dividend sources remain secure and, over time, will compound further into the portfolio’s income stream.

Sources: Recent dividend declarations and raises from company press releases and filings. These underline the dividend amounts and changes noted above.

Citations

DP.21 | Dividend Portfolio Update #21 (January 2026) – Gedal Notes

https://gedal.org/2026/01/10/dp-21-dividend-portfolio-update-21-january-2026/Apple quietly raises 2026 dividend after record quarter | AAPL – TheStreethttps://www.thestreet.com/investing/stocks/beloved-50-year-old-tech-giant-apple-stock-quietly-raised-dividends-in-2026Starbucks Coffee Company – Starbucks Announces Increase in Quarterly Cash Dividendhttps://investor.starbucks.com/news/financial-releases/news-details/2025/Starbucks-Announces-Increase-in-Quarterly-Cash-Dividend/default.aspxDell Technologies Declares Quarterly Cash Dividendhttps://www.businesswire.com/news/home/20251204988757/en/Dell-Technologies-Declares-Quarterly-Cash-DividendFS Bancorp, Inc. (NASDAQ:FSBW) to Issue Dividend Increase – $0.29 Per Sharehttps://www.marketbeat.com/instant-alerts/fs-bancorp-inc-nasdaqfsbw-to-issue-dividend-increase-029-per-share-2026-01-22/BD Board Increases Dividend for 54th Consecutive Year :: Becton, Dickinson and Company (BDX)https://investors.bd.com/news-events/press-releases/detail/914/bd-board-increases-dividend-for-54th-consecutive-yearADP Increases Cash Dividend; Marks 51st Consecutive Year of Dividend Increaseshttps://www.prnewswire.com/news-releases/adp-increases-cash-dividend-marks-51st-consecutive-year-of-dividend-increases-302612176.htmlAmerican States Water Company Announces Regular Common Dividendshttps://www.businesswire.com/news/home/20251030922063/en/American-States-Water-Company-Announces-Regular-Common-DividendsWM Announces 10% Dividend Rate Increase for 2025https://www.businesswire.com/news/home/20241216487906/en/WM-Announces-10-Dividend-Rate-Increase-for-2025WM Announces 10% Dividend Rate Increase for 2025https://www.businesswire.com/news/home/20241216487906/en/WM-Announces-10-Dividend-Rate-Increase-for-2025Microsoft announces quarterly dividend increasehttps://news.microsoft.com/source/2025/09/15/microsoft-announces-quarterly-dividend-increase-6/HAMILTON BEACH BRANDS HOLDING COMPANY ANNOUNCES QUARTERLY DIVIDEND INCREASEhttps://www.prnewswire.com/news-releases/hamilton-beach-brands-holding-company-announces-quarterly-dividend-increase-302451450.htmlQ4 2025 Earnings Releasehttps://s1.q4cdn.com/050606653/files/doc_financials/2025/q4/Q4-2025-Earnings-Release_vF.pdfCostco Wholesale Corporation Announces Increase in Quarterly Cash Dividend to $1.30 per Share | Nasdaqhttps://www.nasdaq.com/articles/costco-wholesale-corporation-announces-increase-quarterly-cash-dividend-130-shareMastercard Incorporated – Mastercard Board of Directors Announces Quarterly Dividend and $14 Billion Share Repurchase Programhttps://investor.mastercard.com/investor-news/investor-news-details/2025/Mastercard-Board-of-Directors-Announces-Quarterly-Dividend-and-14-Billion-Share-Repurchase-Program/default.aspxS&P Global Increases Dividend 1.0% to $0.97https://www.prnewswire.com/news-releases/sp-global-increases-dividend-1-0-to-0-97–302661618.htmlS&P Global Increases Dividend 1.0% to $0.97https://www.prnewswire.com/news-releases/sp-global-increases-dividend-1-0-to-0-97–302661618.htmlS&P Global Increases Dividend 1.0% to $0.97https://www.prnewswire.com/news-releases/sp-global-increases-dividend-1-0-to-0-97–302661618.htmlAlphabet Inc – Class A Shares (GOOGL) Dividendshttps://www.dividendmax.com/united-states/nasdaq/software-and-computer-services/alphabet-inc-class-a-shares/dividendsUnitedHealth Group Board Authorizes Payment of Quarterly Dividend – UnitedHealth Grouphttps://www.unitedhealthgroup.com/newsroom/2025/2025-11-uhg-authorizes-payment-quarterly-dividend.htmlIntuit Reports Strong First-Quarter Results and Reiterates Full-Year Guidancehttps://investors.intuit.com/_assets/_8945f5df3b38ce273cf7bfa182d29587/intuit/news/2025-11-20_Intuit_Reports_Strong_First_Quarter_Results_and_1286.pdfCintas Corporation Announces Quarterly Cash Dividend and New $1.0 Billion Stock Buyback Authorizationhttps://www.cintas.com/newsroom/details/news/2025/10/28/cintas-corporation-announces-quarterly-cash-dividend-and-new-1-billion-stock-buyback-authorization/The Coca-Cola Company (KO) Dividend Date & History | Koyfinhttps://www.koyfin.com/company/ko/dividends/Home Federal Bancorp, Inc. of Louisiana Declares Quarterly Cash Dividend | Nasdaqhttps://www.nasdaq.com/press-release/home-federal-bancorp-inc-louisiana-declares-quarterly-cash-dividend-2026-01-21