May 2026

The portfolio is closing in on $8,000.

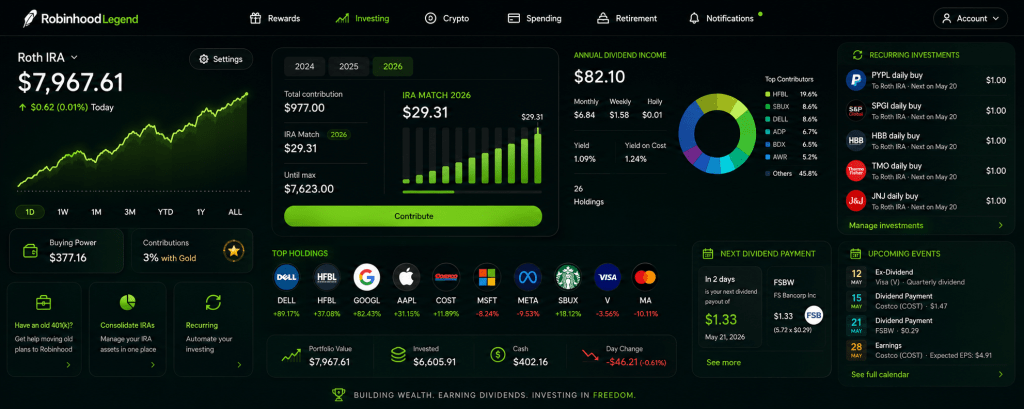

As of this update, the account sits at $7,966.12, up from $6,655.32 last month — a gain of $1,310.80 (+19.7%) month over month. That number deserves a caveat before anything else: the move was a mix of new contributions, recurring buys, market appreciation, and dividend reinvestment, not pure returns. I’d rather be honest about that than overstate what the market did.

The point of this account has never been a one-month percentage. The point is to own quality businesses, contribute consistently, and let dividends compound. May moved the needle on all three.

Portfolio Snapshot

| Metric | May 2026 |

|---|---|

| Portfolio Value | $7,966.12 |

| Total Unrealized Gain | +$958.05 (+14.5%) |

| Invested Capital (Cost Basis) | $6,605.91 |

| Holdings | 26 |

| Previous Update | $6,655.32 |

| MoM Change | +$1,310.80 (+19.7%) |

| Annual Dividend Income | $82.10 |

| Monthly Average | $6.84 |

| Yield | 1.09% |

| Yield on Cost | 1.24% |

A few things worth pulling out of that table.

Forward dividend income is now $82.10/year — about $6.84 a month. Small in absolute terms, but it’s real cash flow being thrown off by a portfolio that didn’t exist two years ago.

The gap between yield (1.09%) and yield on cost (1.24%) is the more interesting number. It means the average dollar I put in is already generating ~14% more income than the same dollar would earn buying these stocks today. That’s the dividend growth flywheel starting to show up in the math, even at this size.

A portfolio under $10K is still in the accumulation stage, but it’s no longer just a collection of starter positions. Structure is starting to matter, and that changes the questions I have to ask.

The Shift: From Accumulating to Constructing

Early on, almost every buy was a win because the portfolio was small enough that anything helped. Approaching $8K, the questions get sharper:

- Which positions are becoming core?

- Which are still experiments?

- Which winners deserve more capital — and which are getting too large?

- Where is the portfolio thin?

- Is dividend growth and total return in the right balance?

This isn’t a high-yield portfolio and it isn’t trying to be. Chasing yield is the easiest way to end up owning broken businesses with attractive payouts. I’d rather own a 1% yielder that compounds for 20 years than a 7% yielder that erodes its capital base in five.

Performance Leaders

| Holding | Shares | Unrealized Gain | Return |

|---|---|---|---|

| Dell | 3.49 | +$385.25 | +88.68% |

| Alphabet | 1.74 | +$324.40 | +87.19% |

| HFBL | 35.97 | +$191.83 | +36.94% |

| Apple | 2.22 | +$151.84 | +30.03% |

| UnitedHealth | 0.36 | +$27.35 | +24.55% |

| Starbucks | 3.57 | +$58.52 | +18.27% |

| Waters | 0.15 | +$5.55 | +12.12% |

| Costco | 0.48 | +$47.44 | +10.03% |

| Coca-Cola | 1.18 | +$5.53 | +6.13% |

| Hamilton Beach | 10.42 | +$10.59 | +6.00% |

Dell and Alphabet are both up roughly 90% and are doing a lot of the heavy lifting. Neither is what most people picture when they hear “dividend portfolio” — Alphabet’s yield is negligible and Dell isn’t a Dividend Aristocrat. But total return grows the capital base that future dividend income gets paid on, and that’s the part that compounds.

The flip side: when a couple of positions run this hard, concentration creeps in without a single new buy. That’s not automatically a problem, but it has to be intentional. For now I’m letting the winners work and watching position sizes more carefully than I had to a few months ago.

Dividend Growth (Without Buying a Single Share)

The most overlooked thing in any dividend portfolio update is the income that grows on its own. Nine of my holdings raised their dividends in recent months, and I didn’t have to do anything except keep owning them:

| Company | Raise | Declared |

|---|---|---|

| Dell | +20.0% | Feb 26 |

| Costco | +13.1% | Apr 15 |

| Thermo Fisher | +9.3% | Feb 21 |

| Alphabet | +4.8% | Apr 27 |

| Hamilton Beach | +4.2% | May 12 |

| Apple | +3.8% | Apr 30 |

| HFBL | +3.7% | Apr 15 |

| Johnson & Johnson | +3.1% | Apr 14 |

| S&P Global | +1.0% | Jan 14 |

Dell at +20% and Costco at +13% stand out — both are well above the rate of inflation, both come from businesses with healthy earnings power, and both come on top of share price appreciation. That’s exactly the combination this portfolio is designed to capture: companies whose payouts grow because the businesses underneath them are getting bigger.

This is also why yield on cost matters more than current yield over time. Every one of these raises permanently lifts the income my existing dollars produce. Compound that over 10 or 20 years and the math gets interesting.

Dividend Composition

The forward dividend income is more concentrated than the portfolio value:

| Position | Share of Annual Dividends |

|---|---|

| HFBL | 19.6% |

| Starbucks | 8.6% |

| Dell | 8.6% |

| ADP | 6.7% |

| BDX | 6.5% |

| AWR | 5.2% |

| HBB | 5.1% |

| WM | 5.0% |

| FSBW | 5.0% |

HFBL alone produces nearly 20% of annual dividend income. The top three positions produce roughly 37%. That’s a real number to be aware of — it doesn’t mean trim anything today, but it does mean the income stream is currently leaning on a small group of names, and the rest of the portfolio still has room to grow into more dividend-meaningful positions.

Upcoming Dividends

| Company | Payment Date | Amount |

|---|---|---|

| FS Bancorp | May 21 | $1.33 |

| Starbucks | May 29 | $2.20 |

| Visa | June 1 | $0.72 |

| Target | June 1 | $0.44 |

| American States Water | June 2 | $1.33 |

| Johnson & Johnson | June 9 | $0.48 |

| Microsoft | June 11 | $0.46 |

| S&P Global | June 11 | $0.50 |

| Cintas | June 15 | $0.31 |

| Alphabet | June 15 | $0.38 |

| Hamilton Beach | June 16 | $1.35 |

| Waste Management | June 18 | $0.93 |

The pattern matters more than any single line: income arriving from banks, consumer brands, payments, utilities, tech, healthcare, industrials, and retail. That spread is the entire point.

How the Portfolio Is Shaping Up

Three rough buckets are starting to emerge across the 26 holdings:

Core compounders — Apple, Alphabet, Costco, Visa, Mastercard, S&P Global, Microsoft, Cintas, Thermo Fisher, Intuit, Meta. Owned for durable earnings power, not yield.

Dividend stability — Coca-Cola, Johnson & Johnson, American States Water, Target, Starbucks, ADP, BDX, Waste Management, UnitedHealth. The traditional dividend-growth foundation.

Opportunistic / smaller — Dell, PayPal, Hamilton Beach, Waters, HFBL, FSBW. Some have already worked; others are still being built or watched.

The objective isn’t dividend income in isolation. It’s rising income supported by rising business value. That’s the difference between owning dividends and owning businesses.

Going Into June

Four things I’m tracking:

- Concentration — in both value and income. HFBL is 20% of dividends. Dell and Alphabet are oversized contributors to total return. Winners are welcome; dependence on a handful of names isn’t.

- Dividend quality, not quantity. A consistent raiser like Costco at +13% is worth more here than any high-yield name with a flat payout.

- Balance across sectors. The current mix is healthy, but some areas are still thin. I want balance to happen naturally as good opportunities come up, not forced for its own sake.

- Process over outcome. A green month can hide bad decisions; a red month can hide good ones. The right question isn’t “did it go up” — it’s “is it getting stronger.”

For May, I think the answer is yes.

May Takeaway

The portfolio crossed within a rounding error of $8,000, winners kept running, nine companies raised their dividends, and forward annual income climbed to $82.10. More importantly, the portfolio is becoming more intentional.

The next milestone is simple: cross $8,000, keep building, move toward $10,000.